NPS vs EPF: Which Retirement Account Gives More Flexibility?

For many salaried professionals, EPF is the default retirement base. NPS can become the additional retirement bucket. The useful question is not which one sounds better, but which flexibility the investor actually needs.

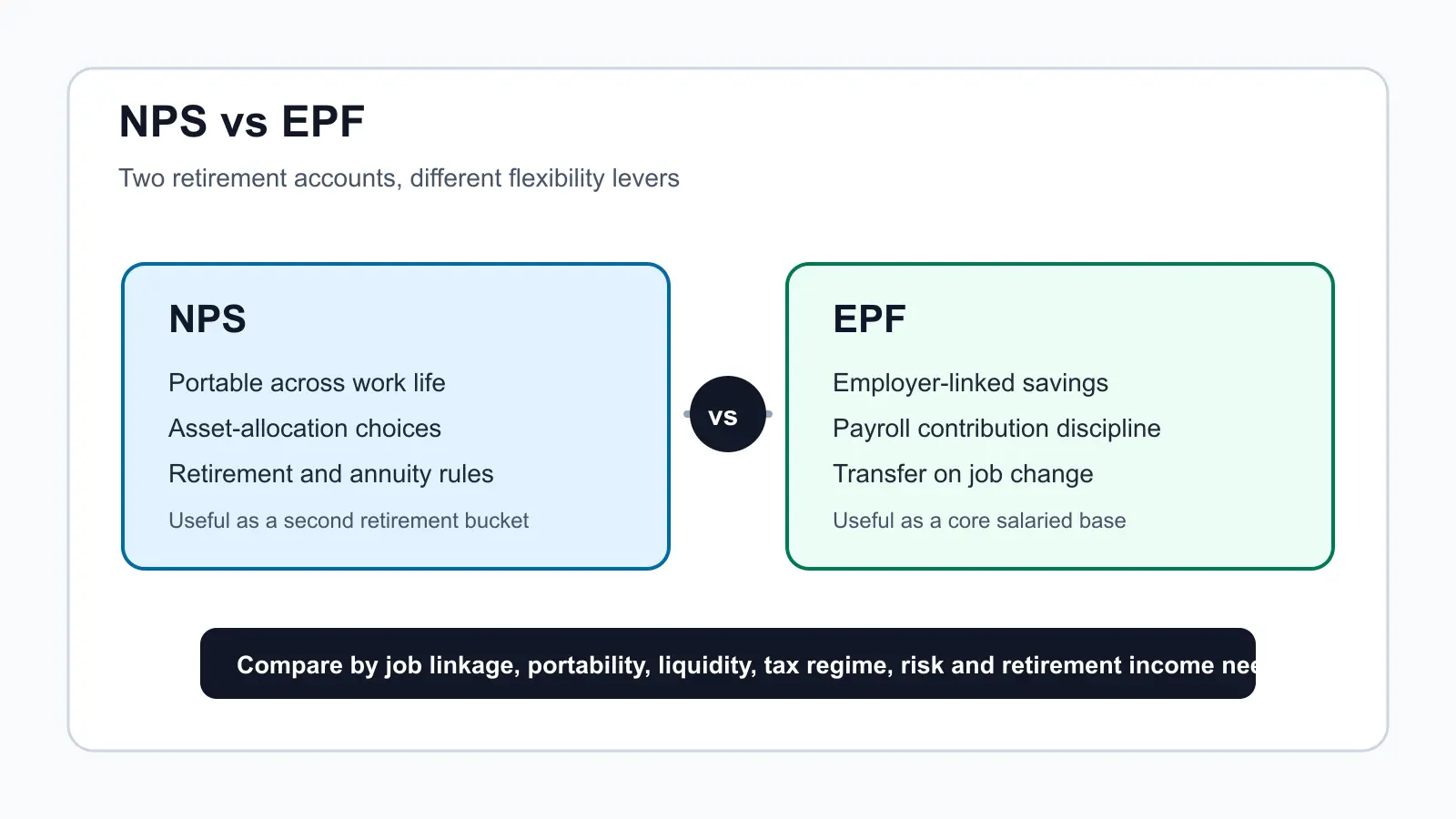

EPF And NPS Solve Different Problems

EPF is closely linked to salaried employment and payroll contribution discipline. NPS is a retirement account that can continue across jobs, locations and self-employment situations, subject to applicable rules.

A person changing jobs, starting consulting work, moving from private employment to business, or planning a second retirement corpus should not compare only deductions. The comparison should include portability, contribution control, liquidity, market risk and exit design.

Flexibility Comparison

| Point | EPF | NPS |

|---|---|---|

| Where it fits | Employer-linked retirement savings for eligible employees, generally handled through payroll. | Portable retirement account that can be used by eligible individuals and continued across employment changes. |

| Contribution discipline | Works through employee and employer contributions, creating automatic saving discipline for salaried employees. | Allows voluntary contribution planning, including recurring NPS contribution setup where suitable. |

| Portability | EPF transfer processes are available when a member changes employment. | NPS is portable across jobs and locations, which can help when the investor changes work structure. |

| Investment choice | EPF is not chosen like a market portfolio by the employee. It is a statutory retirement saving framework. | NPS provides asset-allocation choices across permitted options such as equity, corporate debt and government securities. |

| Liquidity and exit | Withdrawal and transfer depend on EPFO rules, employment status and claim conditions. | Withdrawal and exit follow NPS rules, including retirement-stage lump-sum and annuity design. |

| Tax review | EPF-related tax treatment should be reviewed under the relevant salary, provident fund and deduction provisions. | NPS contributions may involve Section 80CCD provisions, including the additional Section 80CCD(1B) deduction of up to Rs 50,000 where applicable. |

A Practical Decision Map

EPF can be treated as the salaried employee's core retirement base. NPS can be evaluated as an additional retirement bucket when the investor wants portability, asset-allocation control, structured pension planning and a disciplined long-term account.

The comparison changes when someone leaves employment, becomes self-employed, changes jobs often, already has a strong EPF base, or wants to build retirement income beyond employer-linked savings.

Mistakes To Avoid

- Assuming EPF alone will be enough for retirement income.

- Choosing NPS without understanding market risk and exit rules.

- Ignoring EPF transfer when changing jobs.

- Comparing only tax deduction and ignoring liquidity.

- Not checking the current tax regime before assuming deductions.

- Treating retirement planning as a one-account decision.

How Abhipra Can Help

Abhipra has acted as a Point of Presence for 17 years and can guide subscribers on NPS account opening, NPS SIP setup, PRAN servicing, contribution planning, nomination review and retirement-readiness documentation.

- Learn about Abhipra's NPS & Pension services.

- Start online through Abhipra's NPS account opening link.

- Set up recurring contributions through Abhipra's NPS SIP link.

- For NPS process queries, write to nps@abhipra.com.

Source Links / Disclaimer

Sources checked on July 18, 2026:

- PFRDA: NPS All Citizen Model

- EPFO: FAQs

- Income Tax Department: Deductions

- Abhipra: NPS & Pension services

This article is for investor education. EPF rules, NPS rules, tax treatment, withdrawal rules and employer benefit practices may change and may depend on individual facts. Investors should consult a qualified adviser before making tax, investment or retirement-planning decisions.