NPS Exit Mistakes Investors Should Avoid Before Retirement

NPS exit is not just a form submission. It is a retirement-income decision involving lump sum, annuity, tax review, documentation and family cash-flow planning.

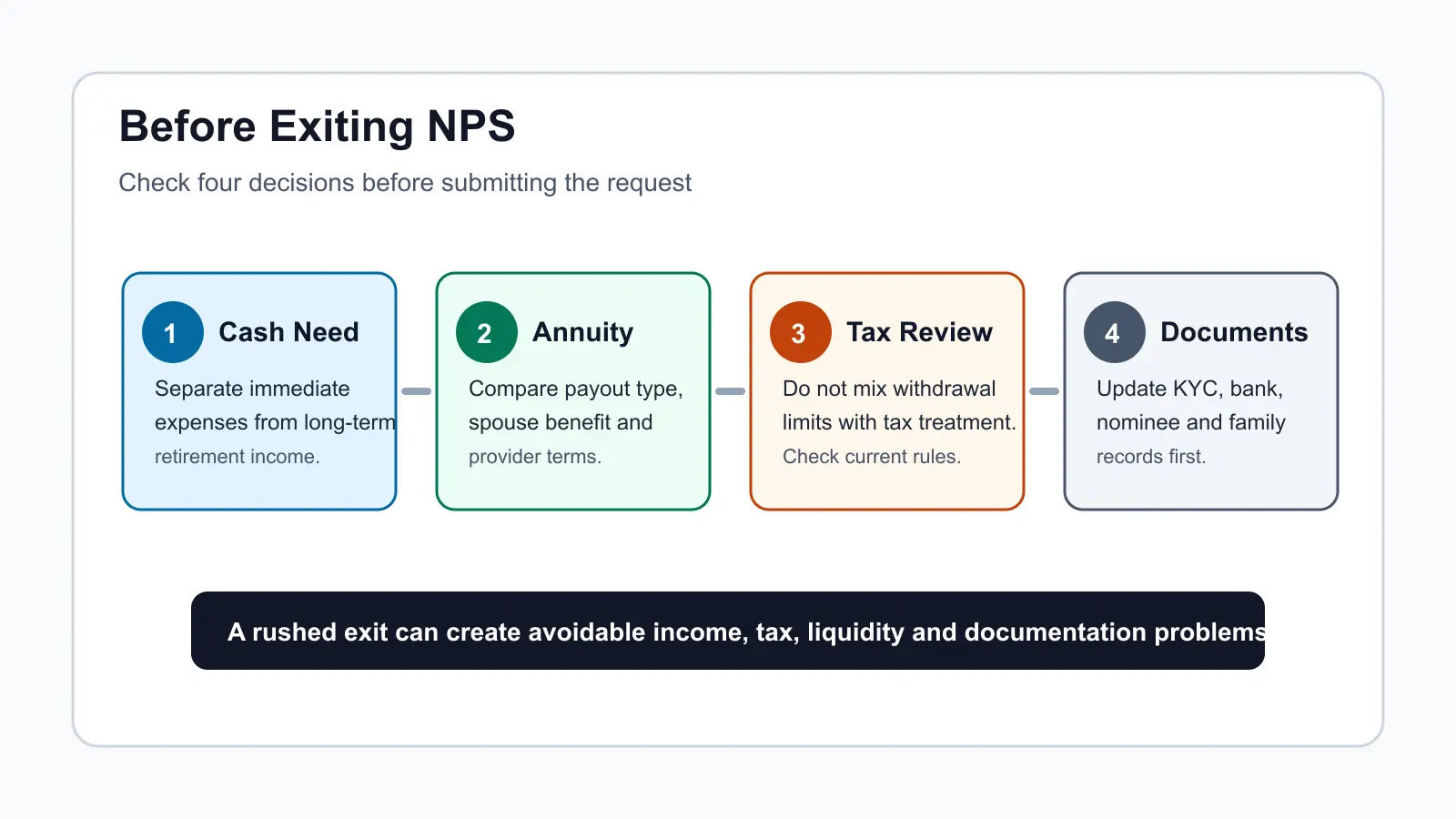

The Costly Mistake Is Rushing The Exit

Many subscribers focus only on how much money can be withdrawn. That is incomplete. The real decision is how the NPS corpus should support the next phase of life: immediate expenses, regular income, medical reserve, family responsibilities and spouse security.

Before submitting an exit request, the subscriber should know whether the case is normal exit on attaining 60, exit after joining NPS after 60, premature exit, death exit or a small-corpus case. The payout design can change materially across these situations.

Current Exit Snapshot

| Exit situation | Current treatment | Mistake to avoid |

|---|---|---|

| Normal exit on attaining age 60 | For subscribers who joined NPS before 60, normal exit is linked to attaining age 60. Up to 80% can be taken as lump sum and at least 20% must normally be used for annuity. If the corpus is up to Rs 8 lakh, 100% withdrawal can be permitted under the small-corpus exit treatment. | Do not assume the full corpus should be withdrawn immediately just because a lump-sum option is available. |

| Premature exit before age 60 | Up to 20% can be taken as lump sum and at least 80% must normally be used for annuity. Corpus up to Rs 5 lakh has approved full-payout options. | Do not plan a premature exit without checking the higher annuity requirement and liquidity impact. |

| Exit after joining NPS after age 60 | Subscribers who opened NPS after 60 should check the currently applicable post-60 entry rule before exit. Current PFRDA scheme information shows no lock-in period and permits up to 80% lump sum and at least 20% annuity. If the corpus is up to Rs 8 lakh, 100% withdrawal can be permitted under the small-corpus exit treatment. | Do not contribute after 60 without knowing the exit route and expected use of the corpus. |

| Death exit | Current NPS exit information lists 100% lump sum as permitted on death, with other approved options also mentioned. | Do not leave nominee, bank, KYC and family communication details outdated. |

Four Checks Before You Exit

Start with cash need. Keep immediate expenses separate from long-term retirement income. Then compare annuity choices because payout type, spouse benefit, return-of-purchase-price terms and provider rates may vary. After that, review tax treatment because withdrawal limits and tax treatment are separate questions. Finally, complete KYC, bank, nominee and family documentation before the request is submitted.

Common Exit Mistakes

- Treating the lump sum as free spending money instead of retirement capital.

- Selecting an annuity without comparing spouse benefit, payout frequency and return-of-purchase-price options.

- Confusing regulatory withdrawal limits with tax treatment.

- Ignoring small-corpus options and systematic withdrawal or approved payout alternatives.

- Leaving nominee, bank, mobile, email or PAN details unresolved until the last moment.

- Not telling the family where PRAN, statements and service records are maintained.

Annuity Choice Should Not Be A Last-Minute Decision

Annuity service providers make annuity payments to NPS subscribers at exit and provide periodic pension payments under the annuity contract. Since annuity variants and rates can differ, the subscriber should compare choices before finalising the exit request.

The lowest-effort option is not always the most suitable one. A retiree should consider monthly cash-flow needs, spouse protection, health situation, other pension income, tax position and family expectations.

How Abhipra Can Help

Abhipra has acted as a Point of Presence for 17 years and can guide subscribers on NPS exit process readiness, annuity documentation, PRAN servicing, nomination review and NPS SIP setup before retirement.

- Learn about Abhipra's NPS & Pension services.

- Start online through Abhipra's NPS account opening link.

- Set up recurring contributions through Abhipra's NPS SIP link.

- For NPS process queries, write to nps@abhipra.com.

Source Links / Disclaimer

Sources checked on July 16, 2026, and exit-age wording corrected after regulatory re-check:

This article is for investor education. NPS rules, tax treatment, annuity terms, small-corpus treatment and operational procedures may change. Subscribers should verify current requirements and consult a qualified adviser before making continuation, exit, withdrawal, annuity or tax decisions.