NPS Nomination: A Family Checklist Every Subscriber Should Review

NPS nomination is easy to postpone because it does not affect today's contribution. But for a family, it can become one of the most important records in the account.

Nomination Is Not Just A Formality

NPS is built as a long-term retirement account. Over many years, family structure, addresses, bank details and personal priorities can change. A nominee record that was correct at account opening may become outdated after marriage, birth of a child, death in the family, divorce, remarriage or a major family settlement.

The practical question is simple: if something happens to the subscriber, will the family know who is nominated, what share is recorded, and which documents will be required?

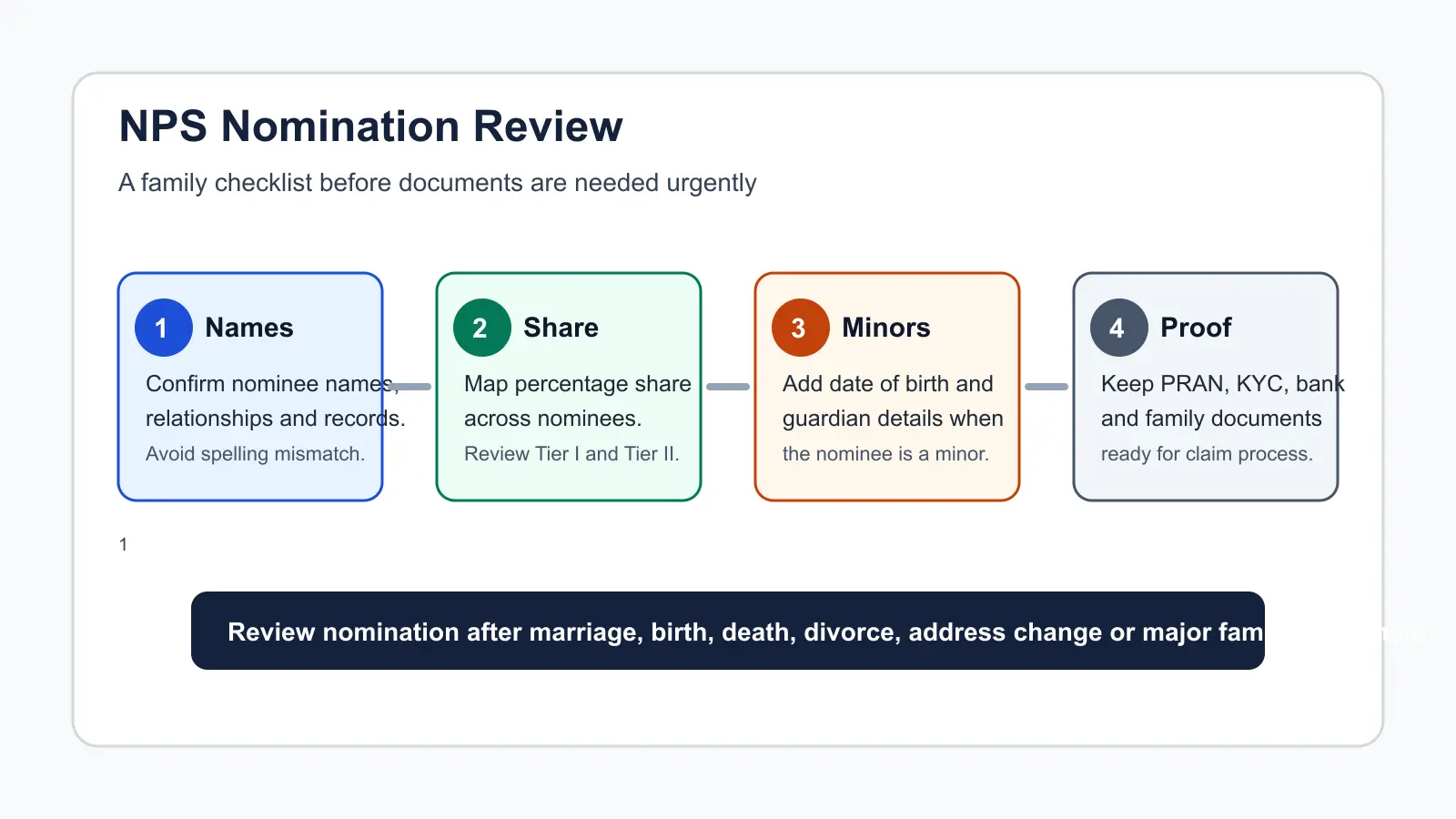

What To Check In The Nomination Record

| Area | What subscribers should review | Why it matters |

|---|---|---|

| Nominee names | The CRA change form provides for up to three nominees. Names, relationship and communication details should be reviewed carefully. | Clear nominee details reduce avoidable confusion for the family during a claim. |

| Percentage share | The additional nomination format captures percentage share for each nominee. | A documented share helps the family understand how the NPS corpus is intended to be distributed. |

| Minor nominee | Where a nominee is a minor, date of birth and guardian details are part of the nomination record. | Minor nominee records need guardian clarity so that future processing is not delayed. |

| Tier I and Tier II | Nomination details can be reviewed for Tier I and Tier II accounts. | A subscriber may want the same nomination for both accounts or a different structure, depending on family planning. |

| Death-exit readiness | Current NPS exit information lists 100% lump sum as permitted on death, with other approved options also mentioned. | The family should know the account, nominee record and document trail before an emergency arises. |

A Simple Family Review Map

Start with names and relationships. Then confirm percentage share. If a nominee is a minor, record guardian details properly. Finally, keep PRAN, KYC, bank and family documents accessible to the people who may need them.

This review should not wait for retirement. It is useful whenever there is a major family event, change in dependent status, change in address, or update in estate-planning documents.

Documents And Conversations To Keep Ready

Subscribers should maintain a simple NPS family file with:

- PRAN and account details.

- Updated mobile number and email linked to the account.

- Nominee names and relationship details.

- KYC and bank-account information.

- Minor nominee guardian details, if applicable.

- Basic instructions on whom the family should contact for process guidance.

The family discussion should be practical, not emotional. The subscriber can tell the nominee where the NPS record is maintained, which email and mobile number are registered, and which adviser or Point of Presence should be contacted for process support.

Common Mistakes To Avoid

- Keeping an old nominee after marriage or remarriage.

- Not updating guardian details when a minor nominee is involved.

- Assuming Tier I and Tier II nomination records are automatically identical.

- Leaving spelling mismatches between account records and identity documents.

- Keeping PRAN, email and mobile details unknown to the family.

How Abhipra Can Help

Abhipra has acted as a Point of Presence for 17 years and can guide subscribers on NPS account servicing, nomination review, PRAN-related process support, contribution setup and withdrawal-process readiness.

- Learn about Abhipra's NPS & Pension services.

- Start online through Abhipra's NPS account opening link.

- Set up recurring contributions through Abhipra's NPS SIP link.

- For NPS process queries, write to nps@abhipra.com.

Source Links / Disclaimer

Sources checked on July 15, 2026:

- PFRDA: NPS All Citizen Model

- Protean CRA: S2 Subscriber Details Change Form

- Abhipra: NPS & Pension services

This article is for investor education. NPS rules, nomination processing, claim documentation and operational procedures may change. Subscribers should verify current requirements and consult a qualified adviser before making NPS, estate-planning or tax-related decisions.