NPS vs ELSS: Same Tax Season, Very Different Jobs

NPS and ELSS often appear in the same tax-saving conversation. That does not mean they do the same job. One is built around retirement and pension income. The other is an equity mutual fund route used for Section 80C tax planning.

Do Not Start With The Tax Deduction

Tax saving is only the entry point. The better question is: what job should this money perform?

If the money must stay disciplined for retirement, NPS may be worth evaluating. If the investor wants equity exposure through a tax-saving mutual fund and can accept market risk, ELSS may fit a different part of the portfolio. Many investors may use both, but with separate expectations.

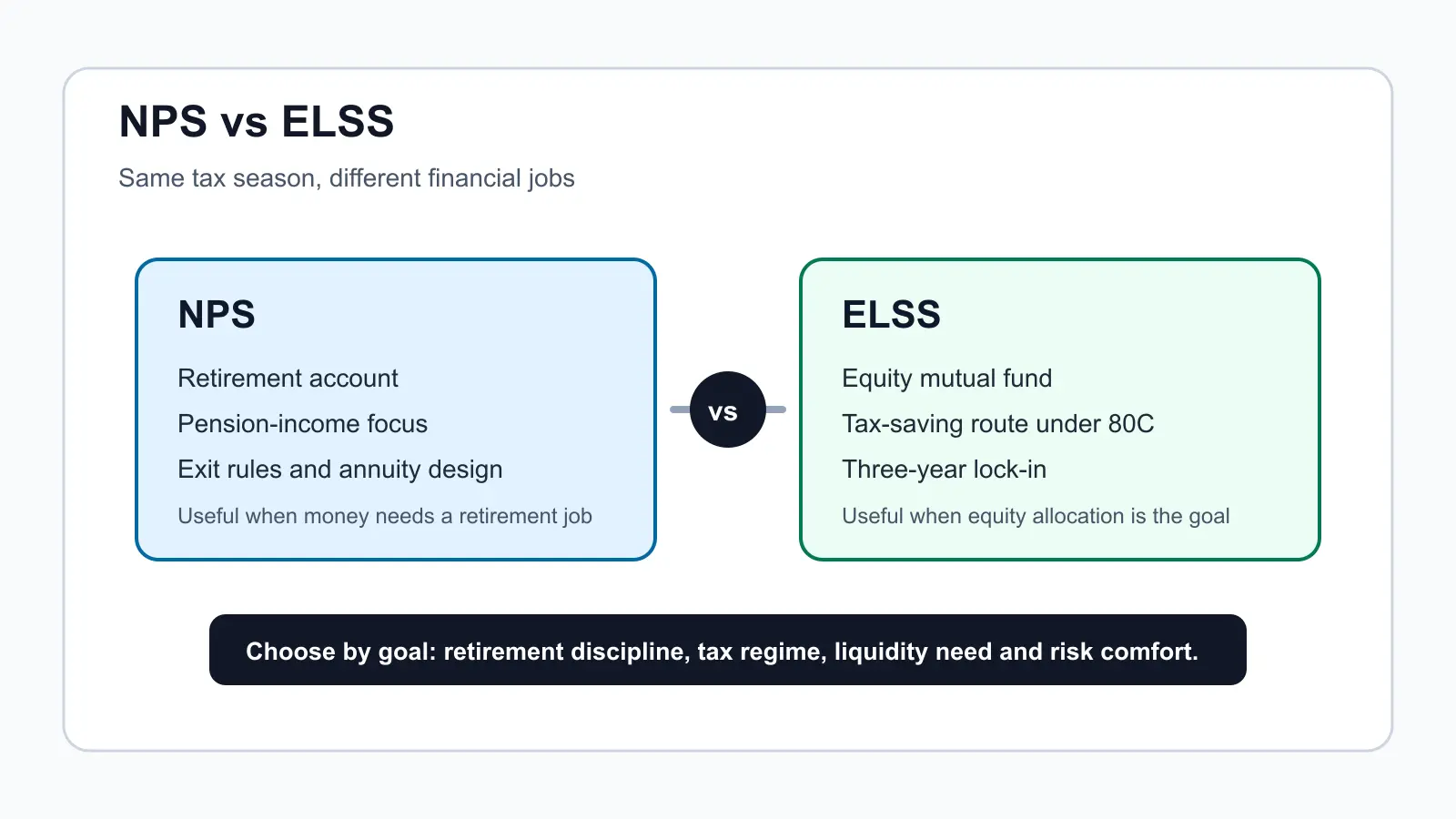

Key Differences At A Glance

| Point | NPS | ELSS |

|---|---|---|

| Primary purpose | Retirement-focused pension account with exit and annuity rules. | Equity-linked tax-saving mutual fund route under Section 80C. |

| Tax section | Own contribution can fall under Section 80CCD(1), and additional NPS contribution under Section 80CCD(1B) can be up to Rs 50,000. Employer contribution may be covered separately under Section 80CCD(2), subject to conditions. | ELSS investment qualifies under Section 80C, where the maximum deduction bucket is Rs 1,50,000 across eligible items. |

| Liquidity | Designed for long-term retirement. Withdrawal and exit are subject to NPS rules. | Has a three-year lock-in. After that, redemption or continued holding depends on the investor's plan. |

| Market risk | Market-linked, with asset allocation across permitted NPS options such as equity, corporate debt and government securities. | Equity-oriented and market-linked. SEBI Investor material describes ELSS as investing at least 80% in equity and equity-related instruments. |

| Best-fit question | Do I need a retirement account with pension-income discipline? | Do I need a tax-saving equity mutual fund allocation? |

A Goal-Based Decision Map

NPS should be evaluated when the investor wants retirement discipline, pension-income planning and a structured long-term account. ELSS should be evaluated when the investor wants equity exposure inside the Section 80C tax-saving bucket and accepts market volatility.

This is not an either-or decision for every investor. A salaried professional may use employer NPS contribution, personal NPS contribution and ELSS differently. A self-employed investor may compare NPS contribution discipline with equity mutual fund liquidity. The answer depends on tax regime, investment horizon, existing 80C usage, risk appetite and retirement gap.

Mistakes To Avoid

- Choosing ELSS only because the lock-in is shorter.

- Choosing NPS only because an extra deduction may be available.

- Ignoring the tax regime before assuming deductions will apply.

- Treating NPS as a short-term tax-saving product.

- Treating ELSS as a risk-free product.

- Using both products without checking total equity exposure and retirement income needs.

How Abhipra Can Help

Abhipra has acted as a Point of Presence for 17 years and can guide subscribers on NPS account opening, contribution setup, PRAN servicing, NPS SIP, nomination review and retirement-process readiness.

- Learn about Abhipra's NPS & Pension services.

- Start online through Abhipra's NPS account opening link.

- Set up recurring contributions through Abhipra's NPS SIP link.

- For NPS process queries, write to nps@abhipra.com.

Source Links / Disclaimer

Sources checked on July 17, 2026:

- PFRDA: NPS All Citizen Model

- Income Tax Department: Deductions

- SEBI Investor: A Guide to ELSS

- Abhipra: NPS & Pension services

This article is for investor education. NPS rules, ELSS scheme terms, tax treatment and deduction availability may change and may differ by tax regime and taxpayer facts. Investors should consult a qualified adviser before making tax, investment or retirement-planning decisions.