NPS Tier I vs Tier II: Which Account Should You Use First?

NPS has two account types, but they do not serve the same purpose. Tier I is the retirement account. Tier II is an optional flexible investment account that becomes available only after an active Tier I account exists.

That one distinction can prevent a lot of confusion. If the goal is retirement discipline, start by understanding Tier I. If the goal is flexible access after that, then Tier II can be evaluated separately.

The Core Difference

PFRDA describes Tier I as the default individual pension account under NPS and as a retirement savings account. Withdrawals from Tier I are governed by PFRDA exit and withdrawal rules, and the account is eligible for tax benefits under the Income Tax Act, 1961.

Tier II is different. PFRDA describes it as an optional investment account, available only to subscribers with an active Tier I account. It has no withdrawal restriction and can be withdrawn from at any time, but it is not eligible for tax benefits.

| Feature | Tier I account | Tier II account | Practical reading |

|---|---|---|---|

| Purpose | Default pension account and retirement savings account. | Optional investment account. | Use Tier I for retirement discipline first. |

| Availability | Opened as the primary NPS account. | Available only with active Tier I account. | Tier II is an add-on, not the starting point. |

| Withdrawals | Subject to PFRDA exit and withdrawal rules. | No withdrawal restriction; subscriber can withdraw any time. | Tier I protects retirement purpose; Tier II gives flexibility. |

| Tax benefits | Eligible for tax benefits under the Income Tax Act, 1961. | Not eligible for tax benefits. | Tax should not be the only reason, but the distinction matters. |

| Investment choices | Subscriber-selected pension fund and asset allocation apply. | Different pension funds and investment options may be chosen for Tier I and Tier II. | Do not assume both accounts must carry identical choices. |

Why Tier I Should Usually Come First

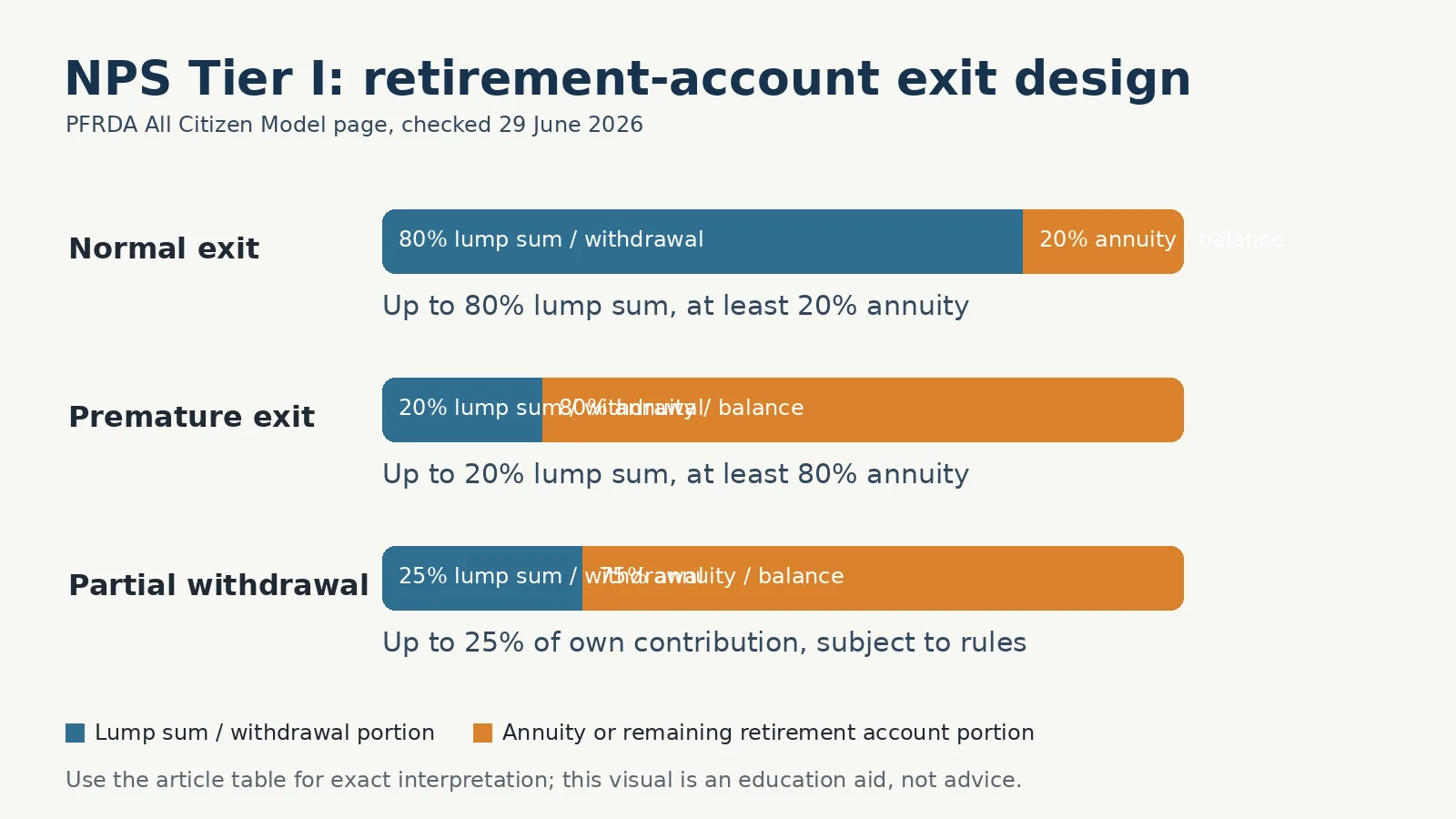

Tier I is built around retirement purpose. That is why exit design matters. PFRDA's All Citizen Model page says normal exit after 60 years or 15 years can allow up to 80% lump sum and at least 20% annuity. Premature exit can allow up to 20% lump sum and at least 80% annuity, subject to corpus-specific and approved payout options.

| Rule area | PFRDA data point | Investor takeaway |

|---|---|---|

| Normal exit after 60 years or 15 years | Up to 80% lump sum; at least 20% annuity. | The account is designed for retirement income, not just accumulation. |

| Premature exit before 60 years or 15 years | Up to 20% lump sum; at least 80% annuity. | Early exit has stronger annuity orientation. |

| Partial withdrawal before 60 | 4 times; 4-year interval between partial withdrawals. | Liquidity exists, but it is not meant to replace emergency savings. |

| Partial withdrawal post 60 | Unlimited frequency; 3-year interval; max 25% of contribution. | Withdrawal choices still need planning. |

When Tier II May Be Considered

Tier II may be useful when an investor already has Tier I and wants a flexible NPS-linked investment account. But flexibility is not the same as suitability.

PFRDA also states that NRIs and OCIs with Tier I accounts are not permitted to activate Tier II account. Investors should check their eligibility, tax situation, liquidity needs and current PFRDA/CRA process before activating or using Tier II.

The decision sequence is simple: open and understand Tier I first, because it carries the pension purpose. Use Tier II only if the flexibility, eligibility and investment choices serve a separate need.

Practical Decision Points

Choose Tier I as the foundation when:

- The money is meant for retirement.

- The investor wants tax-linked retirement planning, subject to applicable rules.

- The investor accepts that withdrawals and exit are rule-bound.

- The investor wants long-term discipline rather than easy access.

Evaluate Tier II separately when:

- Tier I is already active.

- The investor needs flexible withdrawals.

- Tax benefits are not the reason for the contribution.

- The investor understands that Tier II is still market-linked.

FAQs

Can I open Tier II without Tier I?

No. PFRDA describes Tier II as available only to subscribers with an active Tier I account.

Is Tier II a retirement account like Tier I?

No. Tier I is the default pension account and retirement savings account. Tier II is an optional investment account with withdrawal flexibility.

Does Tier II get the same tax benefits as Tier I?

PFRDA states that Tier II is not eligible for tax benefits. Investors should still check their current tax position with a qualified tax adviser.

Can Tier I and Tier II use different investment choices?

PFRDA states that subscribers may choose different pension funds and investment options for Tier I and Tier II accounts.

Conclusion

Tier I and Tier II should not be treated as two versions of the same account. Tier I is the retirement foundation. Tier II is optional flexibility after the foundation exists.

For most investors, the practical order is clear: understand Tier I first, then consider whether Tier II solves a separate need. For service information, read Abhipra NPS & Pension. To start online, use the NPS account opening link. To set recurring contributions, use the NPS SIP setup link.

Reviewed by Abhipra Research / Compliance Team.

Source Links

Disclaimer

This article is for educational and informational purposes only. It is not investment, tax, legal or retirement planning advice. NPS is market-linked and subject to PFRDA rules, investment risk, tax provisions, exit conditions and regulatory changes. Investors should evaluate suitability, liquidity needs, tax position, risk appetite and investment horizon before making any decision.