Before 35 Is Not Early: Why Retirement Planning Needs a Head Start

Amit is 32. His salary is better than it was five years ago, but his money still has many claims on it: rent, family support, insurance, a possible home loan, travel, and short-term goals.

Retirement feels far away, so it keeps moving to "next year".

That is exactly why before 35 matters. It is not about panic. It is about giving your future self enough working years, enough discipline, and enough room to make mistakes without turning retirement into a last-minute scramble.

The Real Advantage Is Time, Not Guesswork

Starting before 35 does not guarantee a bigger corpus. NPS is market-linked, and outcomes depend on contribution discipline, asset allocation, costs, market movement, and rules applicable at the time.

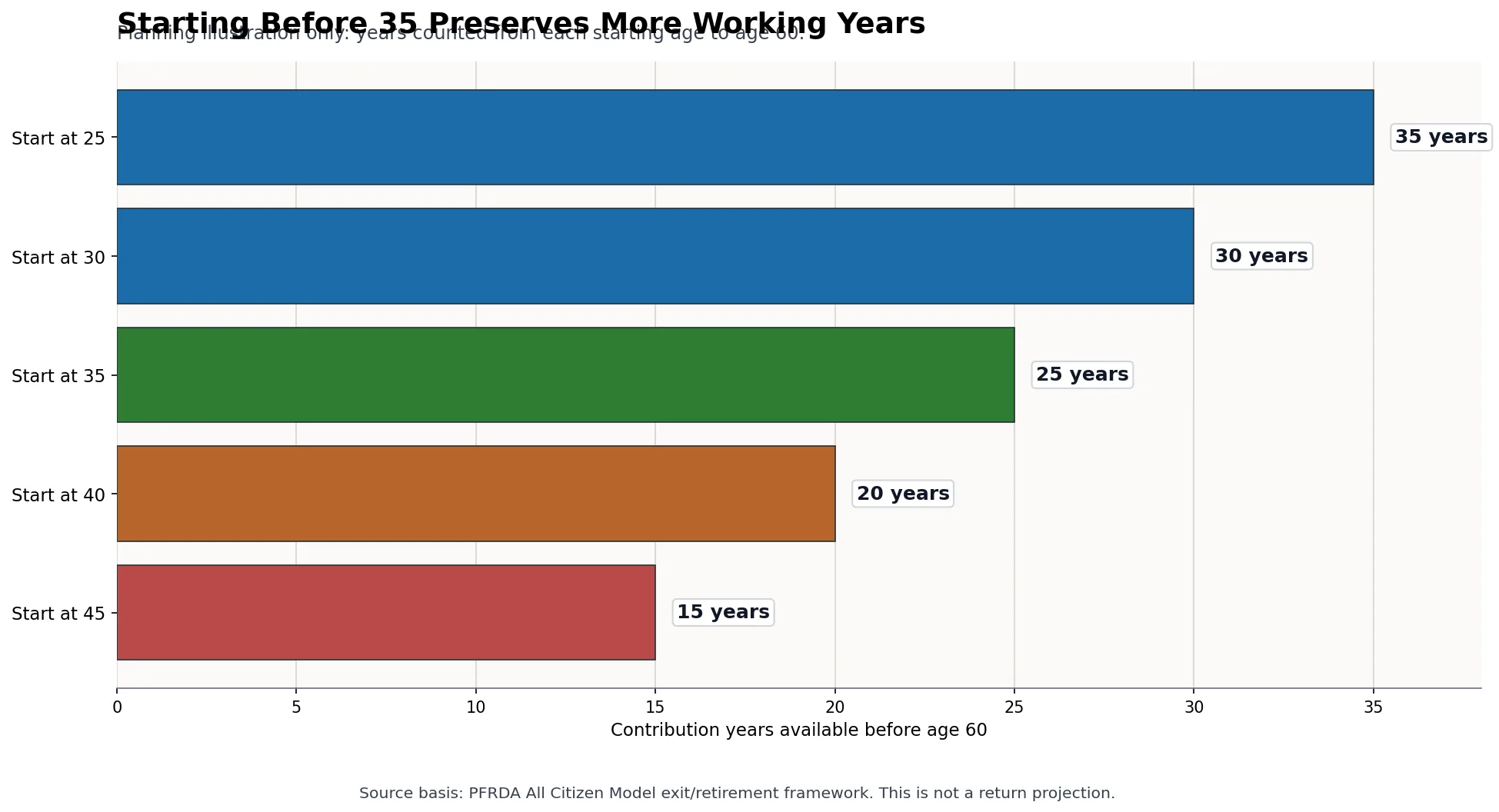

But an early start gives something very practical: more contribution years before retirement decisions become urgent.

| Starting age | Years available till 60 | How to read it |

|---|---|---|

| 25 | 35 years | More time to build the habit gradually. |

| 30 | 30 years | Still a long runway if contributions become regular. |

| 35 | 25 years | The point where delay starts becoming more visible. |

| 40 | 20 years | The monthly saving pressure may rise. |

| 45 | 15 years | Less room to recover from gaps or wrong assumptions. |

This chart uses age 60 only as a planning reference. PFRDA's All Citizen Model page explains the current NPS exit framework, including normal exit after 60 years or 15 years, subject to applicable rules.

Why 35 Is a Useful Checkpoint in NPS

PFRDA's All Citizen Model page says NPS subscribers can choose their pension fund and asset allocation. It also explains Active Choice and Auto Choice.

The age-35 point is important because PFRDA describes Auto Choice as an age-based allocation where allocation remains constant until age 35 and equity allocation reduces gradually with age. In simple words: if a young investor uses an age-based lifecycle option, the system itself treats the years up to 35 as a distinct planning stage.

That does not mean every investor below 35 should take the same risk. It means the risk conversation should start early, while there is time to understand equity, corporate bonds, government securities, liquidity, tax rules and exit conditions.

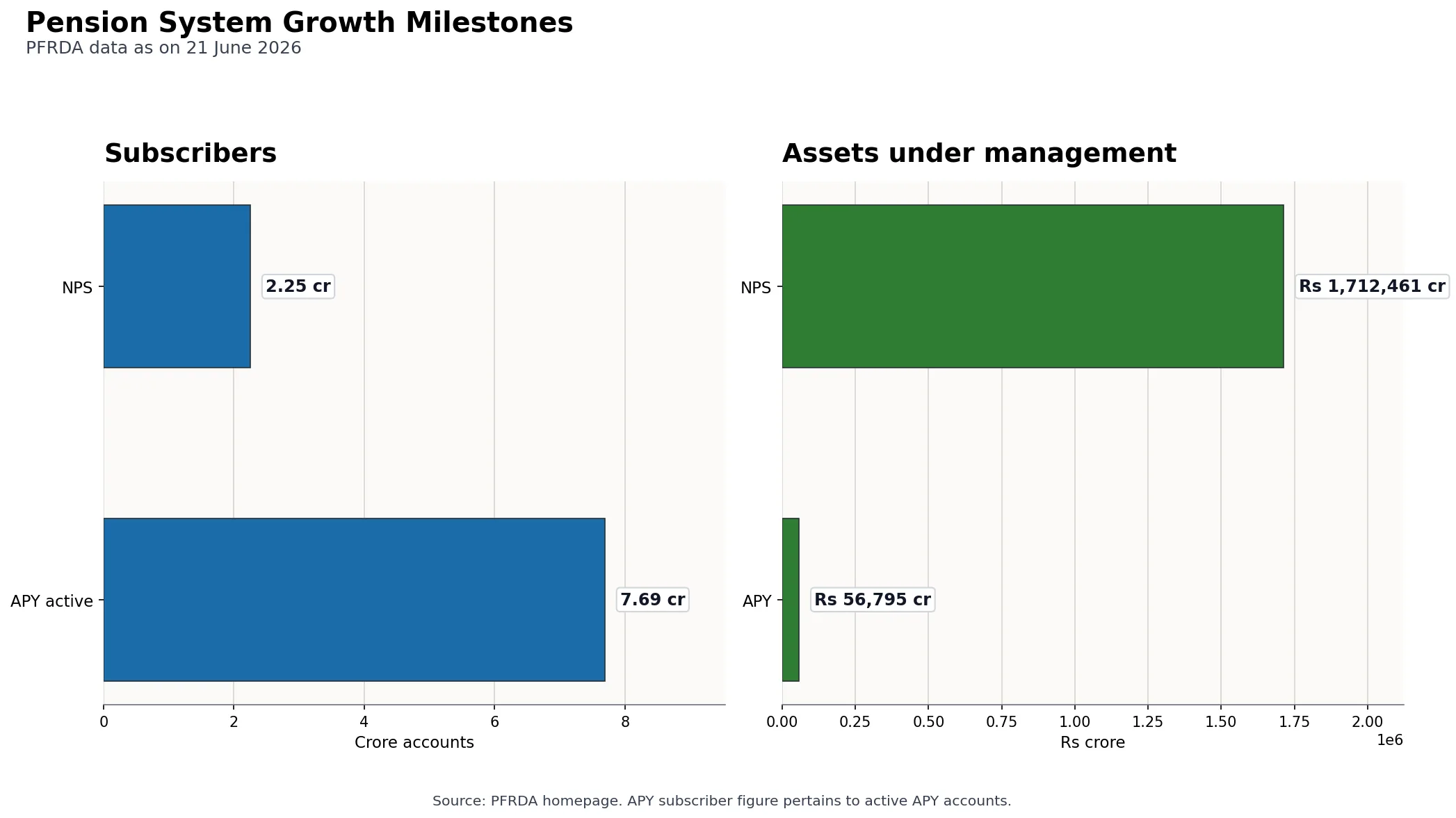

NPS Is Big, But Your Contribution Habit Is Personal

PFRDA's pension-system growth milestones show that NPS has become a large retirement platform. As on 21 June 2026, PFRDA displayed NPS total subscribers at 2.25 crore and NPS assets under management at Rs 17,12,461 crore. It also displayed APY active accounts at 7.69 crore and APY AUM at Rs 56,795 crore.

| Scheme | Subscribers | AUM | Reader takeaway |

|---|---|---|---|

| NPS | 2.25 crore | Rs 17,12,461 crore | A large regulated system can support retirement planning, but suitability is still individual. |

| APY | 7.69 crore active accounts | Rs 56,795 crore | Pension awareness is broadening across income segments. |

The scale is useful context. It should not be read as a recommendation to join without checking liquidity needs, risk appetite, tax position and retirement goals.

The Habit Has to Fit Real Life

Before 35, the problem is usually not that people do not earn. The problem is that every rupee is already emotionally assigned.

A practical retirement plan can start with three small decisions:

- decide a monthly amount that can continue even in a busy month;

- keep emergency money separate, so retirement contributions are not disturbed for routine surprises; and

- review the NPS asset choice once a year instead of reacting to every market headline.

The image above shows the same idea as a home planning routine: retirement saving works better when it becomes a repeatable process, not an annual tax-season panic.

What Young Earners Should Check Before Starting

PFRDA states that NPS under the All Citizen Model can be voluntarily subscribed to by eligible Indian citizens, resident or non-resident, and OCI subscribers, subject to conditions. It also says NPS is regulated by PFRDA, portable, flexible, low cost, transparent and market-linked.

Before opening or increasing contributions, check:

- whether Tier I lock-in and exit rules fit your retirement goal;

- whether you understand the difference between Tier I and Tier II;

- whether Active Choice or Auto Choice suits your risk capacity;

- how much equity exposure you can emotionally tolerate;

- whether you have emergency money and health/life protection in place;

- how NPS fits with EPF, PPF, mutual funds, insurance and other assets; and

- whether tax benefits are relevant under your chosen tax regime.

For service information, read Abhipra NPS & Pension. To start the process online, visit the NPS account opening link. To set up recurring contributions, use the NPS SIP setup link.

FAQs

Is 35 too late to start retirement planning?

No. The point is not that planning after 35 is useless. The point is that before 35 gives more time to build discipline, understand risk and recover from contribution gaps.

Should I start NPS only for tax saving?

NPS may provide tax benefits subject to the Income Tax Act and the tax regime applicable to you, but it should first be evaluated as a retirement product. Tax saving alone is a weak reason to ignore liquidity, risk and exit conditions.

Can I change my NPS choices later?

PFRDA's All Citizen Model page states that subscribers can choose pension funds and investment options, and that asset allocation or investment choice can be changed within allowed limits. Investors should verify the current rules before acting.

Conclusion

Before 35 is not "too early" for retirement planning. It is the stage where the monthly habit can be small, the learning curve can be calmer, and the plan can adjust as income and family responsibilities grow.

The aim is not to guess the future perfectly. The aim is to stop postponing a goal that will eventually become non-negotiable.

Reviewed by Abhipra Research / Compliance Team.

Source Links

- PFRDA All Citizen Model

- PFRDA homepage pension-system growth milestones

- PFRDA Pension Bulletin March 2026

- NPS Trust

- Abhipra NPS & Pension

Disclaimer

This article is for educational and informational purposes only. It should not be treated as investment, tax, legal, or retirement planning advice. NPS is a market-linked retirement product and is subject to applicable PFRDA rules, investment risks, tax provisions, and withdrawal conditions. Investors should carefully evaluate their financial goals, risk appetite, investment horizon, liquidity needs and tax situation before making any decision.