One Hour Can Start Retirement Readiness: An NPS Awareness Playbook for MSMEs

In many MSME teams, retirement planning is not ignored because employees are careless. It is ignored because the conversation never starts.

A supervisor may discuss attendance, wages, overtime and production targets every week. But the question, “What will your monthly income look like after work stops?” rarely gets a quiet 30 minutes.

That is exactly where an NPS awareness session can help. It does not need to sound like a financial seminar. It should feel like a practical workplace conversation about old-age security, contribution discipline and the choices employees should understand before opening or using a National Pension System account.

Start With The Real Problem, Not The Product

The first 10 minutes should not begin with forms or tax sections. Start with the retirement gap.

The PIB release on PFRDA’s MSME outreach in January 2026 stated that MSMEs employ over 32 crore people nationwide and are the second-largest employer after agriculture. The same release highlighted that only 29% of India’s elderly population currently receives any pension.

That contrast makes the session relevant. A workplace may be small, but the retirement question is large.

Ask employees three simple questions:

- If regular salary stops at 60, where will monthly income come from?

- Is there a separate retirement account, or is all saving mixed with household money?

- Does the family know who is nominated and where account details are kept?

These questions make the session human before it becomes technical.

Keep The Session Short And Structured

A good MSME awareness session can be completed in 45 to 60 minutes.

Use this flow:

- Retirement reality: explain longer post-work life, rising family costs and why pension planning should not wait until the final decade of employment.

- NPS basics: explain that NPS is a regulated, market-linked retirement system. It is not a fixed-return deposit and does not guarantee market returns.

- Corporate NPS model: explain that the PFRDA NPS for Corporates page describes Corporate NPS as a platform for employers to extend old-age social-security benefits with flexible employer and employee contributions.

- Choices and risks: discuss pension fund choice, investment pattern, market risk, liquidity limits, exit rules and the need for emergency savings outside NPS.

- Action support: explain how interested employees can complete KYC, nomination, contribution setup and account access through an authorised channel.

Avoid turning the meeting into a sales pitch. Employees should leave with clarity, not pressure.

Use Data To Show Momentum

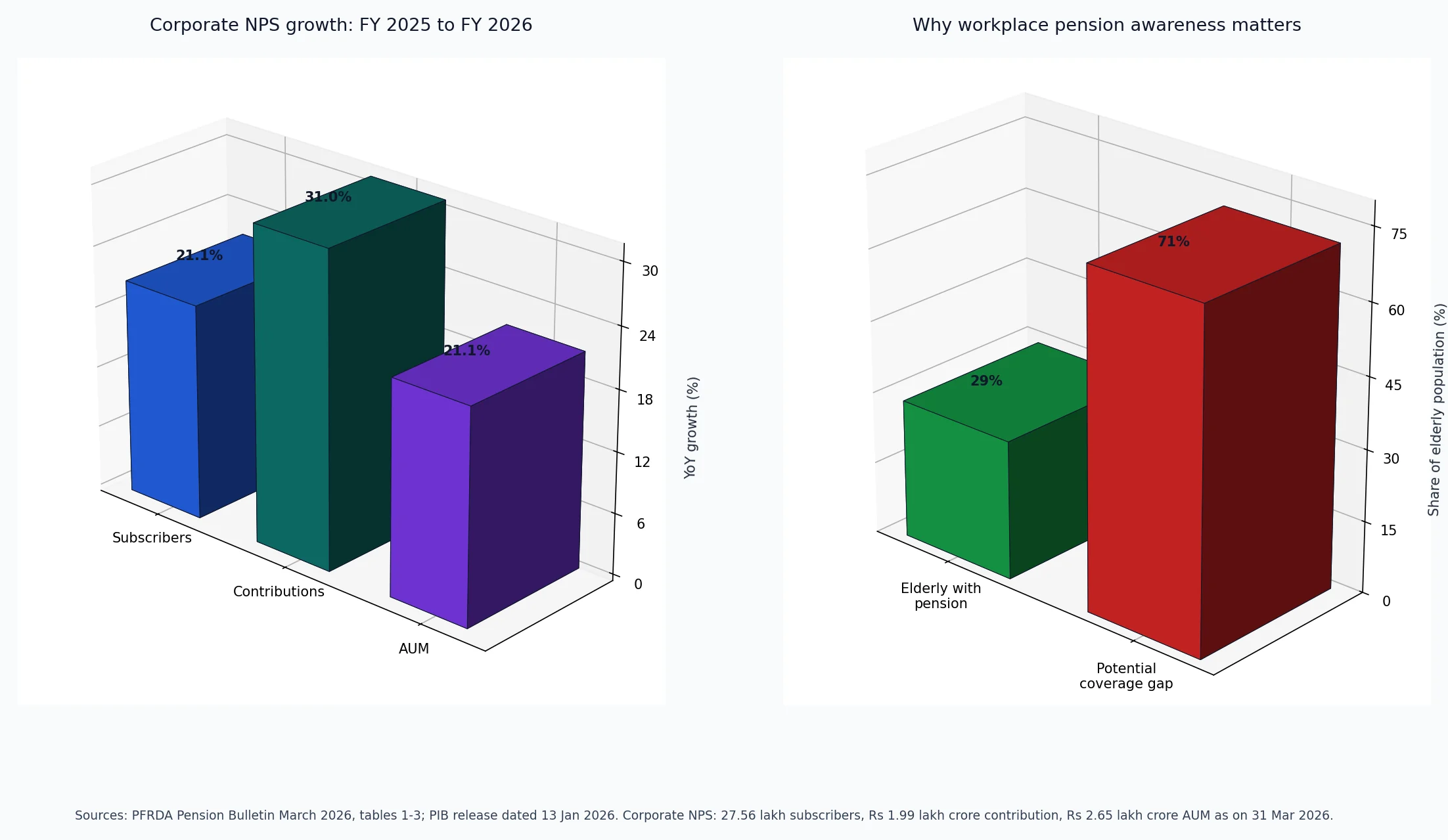

The chart uses official PFRDA and PIB data to show two ideas:

- Corporate NPS is growing: PFRDA’s March 2026 Pension Bulletin reports that Corporate NPS subscribers rose from 22.75 lakh on 31 March 2025 to 27.56 lakh on 31 March 2026, a 21.1% year-on-year increase. Corporate NPS contribution rose 31.0% year-on-year to about Rs 1.99 lakh crore, and Corporate NPS AUM rose 21.1% year-on-year to about Rs 2.65 lakh crore.

- The awareness gap remains large: PIB’s January 2026 release states that only 29% of India’s elderly population currently receives any pension, leaving a large protection gap that workplace education can help address.

These numbers should be used responsibly. Growth in NPS adoption does not mean NPS is automatically suitable for every employee. Suitability depends on age, income stability, emergency liquidity, risk appetite, tax position and retirement objective.

What Employees Should Understand Before Joining

Employees should hear the plain version of NPS, not only the benefits.

NPS can help create disciplined retirement saving because contributions are earmarked for a long-term purpose. Under the Corporate NPS model, PFRDA states that accounts are portable across jobs and geographies, which matters in MSME sectors where employees may change employer, city or role over time.

At the same time, employees should understand:

- NPS is market-linked, so account value can move up or down.

- Tier I is meant for retirement and has regulated access and exit conditions.

- Emergency money should be kept separately; retirement money should not be the first source for short-term needs.

- Nomination, mobile number, email and bank details should remain updated.

- Tax benefits, where applicable, depend on the employee’s regime, salary structure and current law.

This balanced explanation builds trust. It also reduces future complaints caused by misunderstanding.

What The Employer Should Prepare

The employer or HR team should prepare a simple checklist before the session:

- Decide whether the session is only educational or also includes assisted onboarding.

- Keep employee questions anonymous where possible, especially around salary, age and family responsibilities.

- Explain whether employer contribution is planned, optional or not part of the current policy.

- Coordinate with a registered Point of Presence for account-opening and servicing support.

- Provide employees with a written list of documents, KYC requirements, contribution options and contact points.

- Keep attendance and communication records for auditability.

For a small team, one room and one hour may be enough. For a factory or branch network, it may be better to conduct short batch-wise sessions so employees can ask questions comfortably.

What A Point Of Presence Can Help With

The PFRDA list of registered Points of Presence, published on 15 April 2026, includes Abhipra Capital Ltd as a registered PoP. As a Point of Presence, Abhipra provides NPS awareness support through employee sessions, online and offline conferences, and one-to-one discussions. Abhipra also helps investors with NPS onboarding and account operations.

MSME owners and HR teams can review Abhipra NPS & Pension services for awareness-session and account-service support. Eligible employees may use the NPS account-opening journey through Abhipra or the NPS SIP setup journey through Abhipra. For assistance, contact the Abhipra NPS Desk.

Questions Employees Usually Ask

Is NPS only for tax saving?

No. Tax treatment may be relevant, but NPS is primarily a retirement-planning account. Employees should not join only because a deduction is mentioned.

Can I stop contributing if money is tight?

Contribution flexibility depends on the account type, rules and service channel. Employees should not overcommit. Emergency liquidity and household cash flow should come first.

Will I get a guaranteed return?

No. NPS is market-linked. Returns depend on contributions, investment choice, pension fund performance, charges and time horizon.

What happens if I change my job?

PFRDA describes NPS as portable across jobs and geographies. Employees should keep account details, PRAN information, contact details and nomination updated when they move.

Should every employee join immediately?

No. Awareness should lead to informed choice. Employees should evaluate age, income stability, family responsibilities, risk appetite, existing retirement savings and applicable rules.

A Practical Closing For The Session

End the meeting with three actions:

- Employees who are interested should verify eligibility, KYC and contribution process through an authorised channel.

- Employees who are unsure should first list emergency savings, current debt and existing retirement benefits.

- Employers should decide whether NPS will remain an optional awareness initiative or become part of a documented employee-benefit policy.

An NPS awareness session is not about convincing every employee in one sitting. It is about giving workers the language, facts and service pathway to think about retirement before it becomes urgent.

Reviewed by Abhipra Research / Compliance Team.

Source Links

- PIB: PFRDA undertakes NPS outreach for MSMEs at Vibrant Gujarat Regional Conference 2026

- PFRDA: NPS for Corporates

- PFRDA: Pension Bulletin March 2026

- NPS Trust: Functions of Point of Presence

- PFRDA: List of registered Points of Presence

- Abhipra: NPS & Pension services

Disclaimer

This article is for educational and informational purposes only. It is not investment, tax, legal or retirement-planning advice. NPS is market-linked and subject to applicable PFRDA rules, investment risks, charges, contribution conditions, tax provisions, exit rules and operational procedures. Employers and employees should verify current rules, suitability and service availability through authorised channels before taking action.