NPS vs Fixed Deposits: Safety Is Not the Same as Retirement Readiness

Rohit’s father had one simple rule: “Keep retirement money safe.” So Rohit opened fixed deposits every year and felt responsible.

Then one question changed the conversation: safe for what?

Money needed in the next few months should be easy to access. Money meant for retirement has a different job. It must survive decades of spending, medical surprises, inflation and changing family needs. That is where comparing fixed deposits with NPS becomes useful.

Fixed Deposits Solve One Problem Well

A fixed deposit can be useful when the goal is stability, known interest terms and relatively simple documentation. It may suit emergency backup, near-term goals, or conservative money that cannot tolerate market movement.

But a fixed deposit is not automatically a complete retirement plan. Interest rates change across banks and tenures. Premature withdrawal conditions can differ. Tax treatment depends on the investor’s situation. And over a long retirement, the question is not only whether the principal feels safe today, but whether the income can support tomorrow’s expenses.

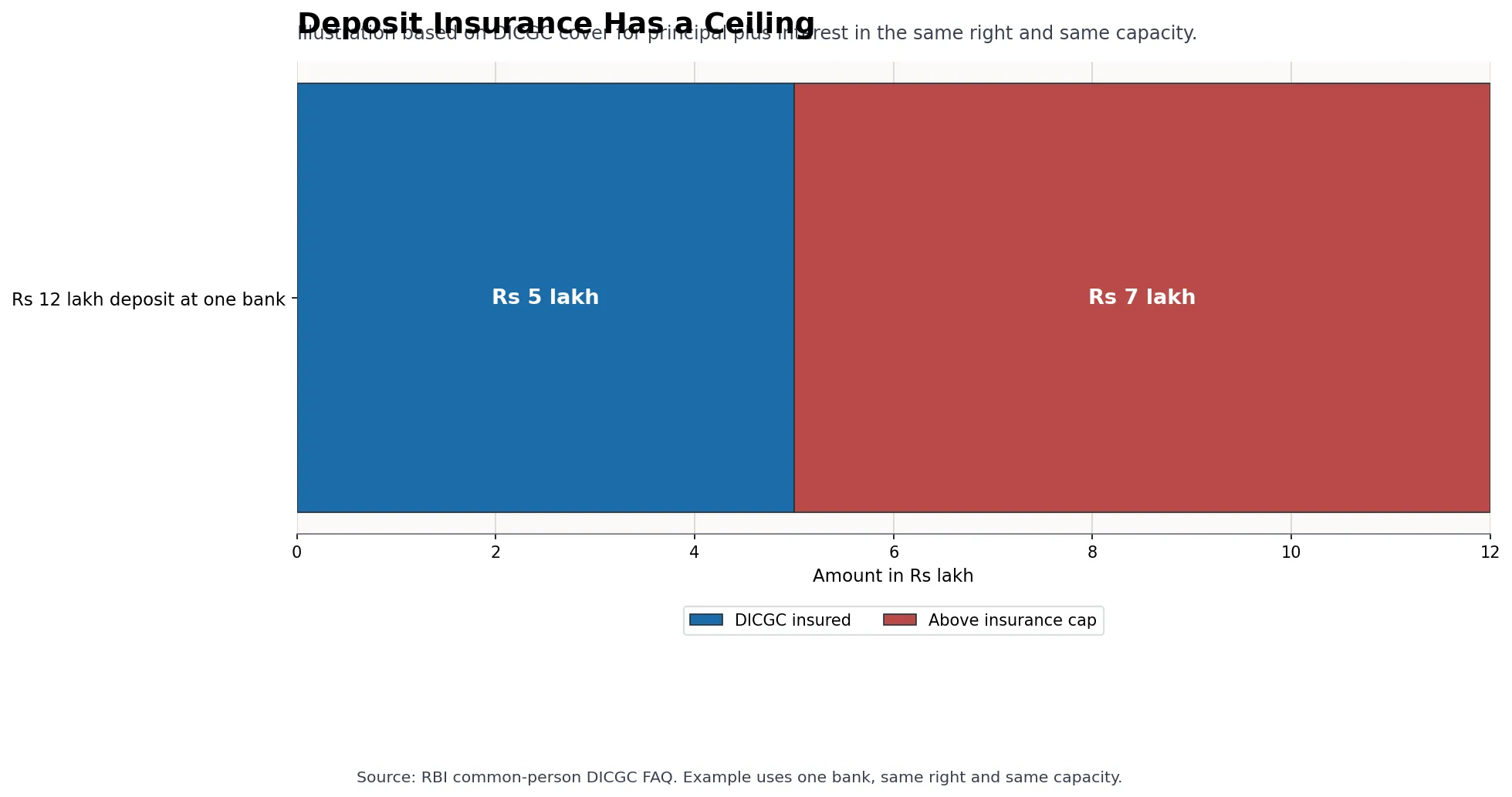

Deposit Insurance Is Important, But It Has a Limit

RBI’s common-person FAQ on DICGC explains that deposits such as savings, fixed, current and recurring deposits are insured, except specified exclusions. It also states that each depositor in a bank is insured up to Rs 5,00,000 for principal and interest held in the same right and same capacity.

| Illustration | Amount | What it means |

|---|---|---|

| DICGC insured portion | Rs 5 lakh | Maximum cover for principal plus interest in the same right and same capacity at one bank. |

| Amount above the insurance cap in this illustration | Rs 7 lakh | A larger deposit can still be held, but the DICGC insurance ceiling should be understood. |

This does not mean fixed deposits are bad. It means safety has layers: bank selection, deposit size, insurance rules, tax, liquidity and the time period for which money is needed.

NPS Solves a Different Problem

PFRDA describes NPS under the All Citizen Model as a regulated, low-cost, flexible, portable and market-linked pension system. It also says NPS can be voluntarily subscribed to by eligible Indian citizens, resident or non-resident, and OCI subscribers, subject to rules.

The key phrase is “pension system”. Tier I is the default pension account and is treated as a retirement savings account. Withdrawals follow PFRDA exit regulations. This makes NPS less flexible than a bank deposit, but that reduced flexibility is also part of its retirement discipline.

PFRDA also explains that contributions are invested according to the subscriber’s selected pension fund and asset allocation. Active Choice can include equity, corporate bonds and government securities within specified limits, while Auto Choice uses age-based lifecycle allocation.

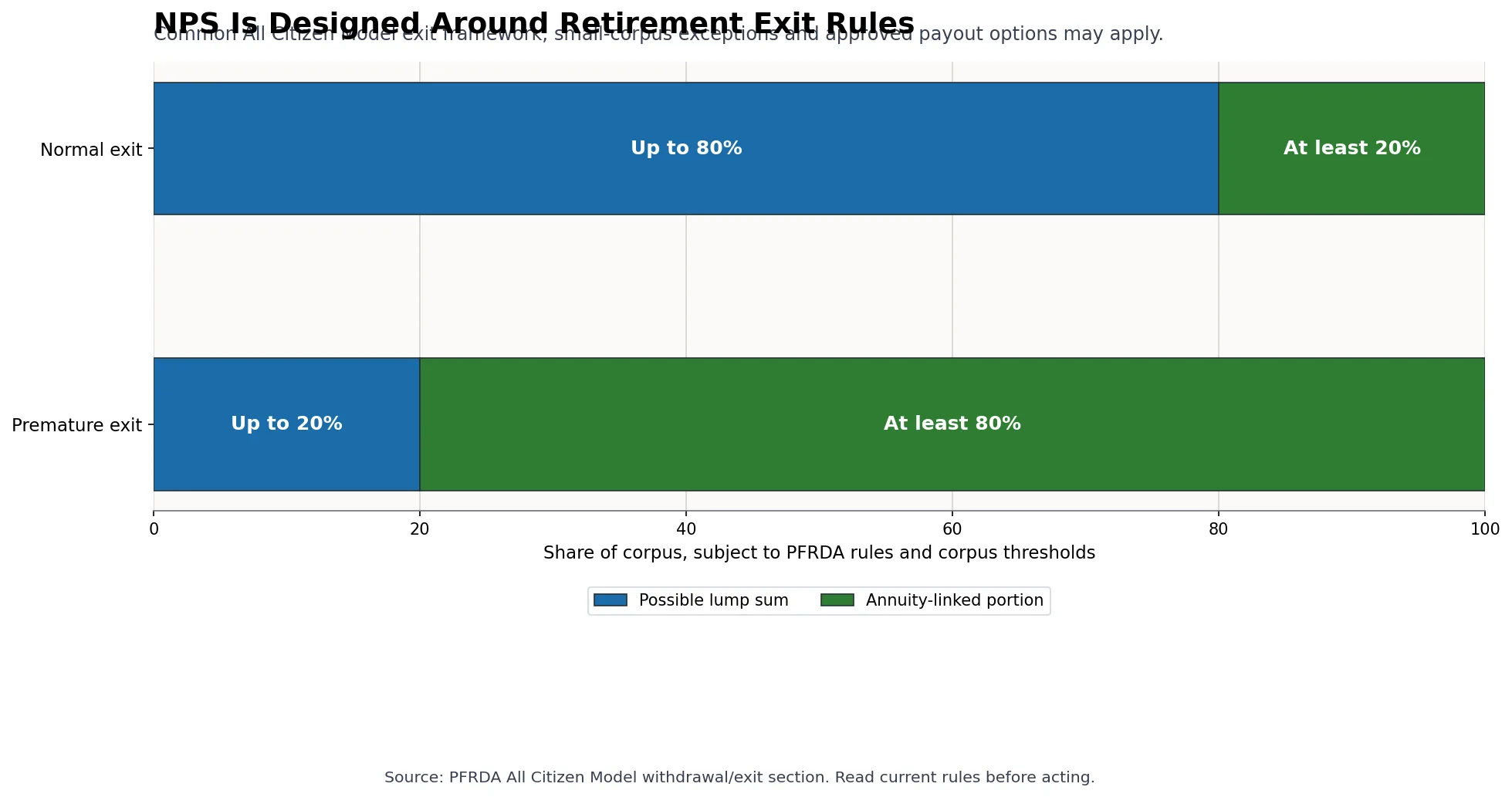

The Exit Rules Show the Real Purpose

NPS is not designed like a short-term deposit. PFRDA’s All Citizen Model page describes the common exit framework: normal exit after 60 years or 15 years can allow up to 80% lump sum and at least 20% annuity, while premature exit can allow up to 20% lump sum and at least 80% annuity, subject to corpus thresholds and approved payout options.

| Exit situation | Possible lump sum | Annuity-linked portion | Practical takeaway |

|---|---|---|---|

| Normal exit after 60 years or 15 years | Up to 80% | At least 20% | Designed to combine lump-sum access with pension-income planning. |

| Premature exit before 60 years or 15 years | Up to 20% | At least 80% | Early exit is deliberately more restrictive, subject to exceptions and current rules. |

This structure is exactly why NPS should not be treated like an FD replacement for money that may be needed soon.

The Better Question Is: Which Money Has Which Job?

The useful comparison is not “NPS or FD?” It is “which rupee belongs where?”

- Money needed for emergencies or near-term payments may need bank liquidity and capital stability.

- Money meant strictly for retirement may need discipline, long-term asset allocation and market-linked participation.

- A household can use both, as long as the purpose of each bucket is written clearly.

The image above shows this as a sorting exercise. One side is near-term safety. The other is retirement readiness. Confusing the two creates most of the mistakes.

Where Fixed Deposits May Fit

Fixed deposits may fit when the investor needs:

- known tenure and interest terms;

- short-to-medium-term goal parking;

- low market volatility;

- simple nomination and documentation;

- emergency reserve layering, subject to premature-withdrawal rules; or

- conservative allocation outside market-linked products.

Even then, investors should check tax, deposit concentration, DICGC cover, premature withdrawal terms and whether the deposit is with an insured bank.

Where NPS May Fit

NPS may fit when the investor wants:

- a dedicated retirement account rather than casual saving;

- long-term contribution discipline;

- exposure to regulated pension-fund investment choices;

- portability across jobs and locations;

- possible tax benefits subject to the Income Tax Act and the chosen tax regime; and

- retirement-income planning through the exit and annuity framework.

For service information, read Abhipra NPS & Pension. To start the process online, visit the NPS account opening link. To set up recurring contributions, use the NPS SIP setup link.

FAQs

Is NPS safer than a fixed deposit?

No. They carry different risks. FDs may offer stable bank-deposit terms and deposit-insurance protection up to the applicable DICGC limit. NPS is market-linked and meant for retirement planning, so its value can move with investments and rules.

Should all retirement money be in NPS?

Not necessarily. Retirement planning can include NPS, EPF, PPF, mutual funds, deposits, insurance and other assets. Suitability depends on age, income stability, risk appetite, liquidity needs and tax position.

Can fixed deposits still be useful after starting NPS?

Yes. Fixed deposits can still support emergency money, near-term needs and conservative allocation. NPS and FDs can complement each other when each has a clear role.

Conclusion

A fixed deposit can protect stability. NPS can create retirement discipline. Neither removes the need for planning.

The strongest retirement plan is not the one that chooses one product for every job. It is the one that knows which money must stay liquid, which money can accept market-linked risk, and which money should be protected from short-term spending habits.

Reviewed by Abhipra Research / Compliance Team.

Source Links

- PFRDA All Citizen Model

- RBI common-person FAQ on DICGC deposit insurance

- NPS Trust

- Abhipra NPS & Pension

Disclaimer

This article is for educational and informational purposes only. It should not be treated as investment, tax, legal, banking, or retirement planning advice. NPS is a market-linked retirement product and is subject to applicable PFRDA rules, investment risks, tax provisions, annuity conditions and withdrawal rules. Fixed deposits are subject to bank terms, interest-rate conditions, taxation, premature-withdrawal rules and applicable deposit-insurance limits. Investors should carefully evaluate their goals, liquidity needs, risk appetite, investment horizon and tax situation before making any decision.