How Rs 5,000 a Month in NPS Can Build Retirement Discipline

A monthly contribution looks small only when it is seen in isolation. Rs 5,000 can disappear into routine spending very easily. But when the same amount is moved into a retirement account every month, it starts doing something more important than chasing a number: it creates a habit.

That is the real value of this idea. NPS is market-linked, so no one should treat a monthly contribution as a guaranteed future corpus. But a fixed monthly NPS routine can help investors separate retirement money from short-term spending and review the plan calmly instead of rushing during tax season.

The Discipline Starts Before Returns

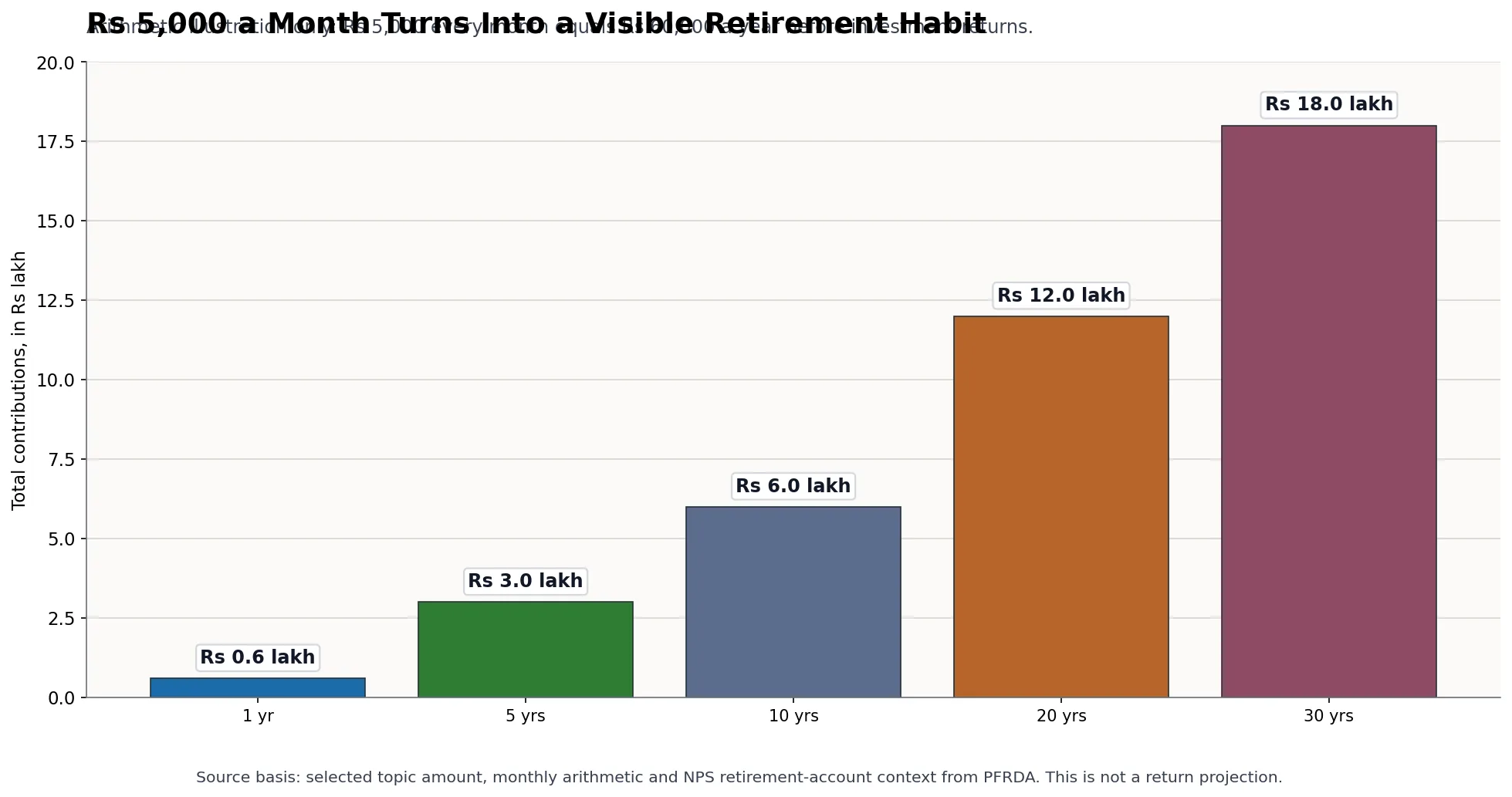

Rs 5,000 per month is Rs 60,000 a year. Without assuming any investment return, that habit alone means Rs 3 lakh contributed over five years, Rs 6 lakh over ten years, Rs 12 lakh over twenty years and Rs 18 lakh over thirty years.

| Contribution period | Amount contributed | How to read it |

|---|---|---|

| 1 year | Rs 60,000 | A monthly habit becomes an annual retirement line item. |

| 5 years | Rs 3 lakh | The contribution habit becomes visible even before returns. |

| 10 years | Rs 6 lakh | Long-term discipline starts reducing dependence on last-minute tax saving. |

| 20 years | Rs 12 lakh | Regularity matters because retirement money needs time and separation. |

| 30 years | Rs 18 lakh | A small monthly decision can become a serious long-term allocation. |

What Compounding Could Mean In A 30-Year Illustration

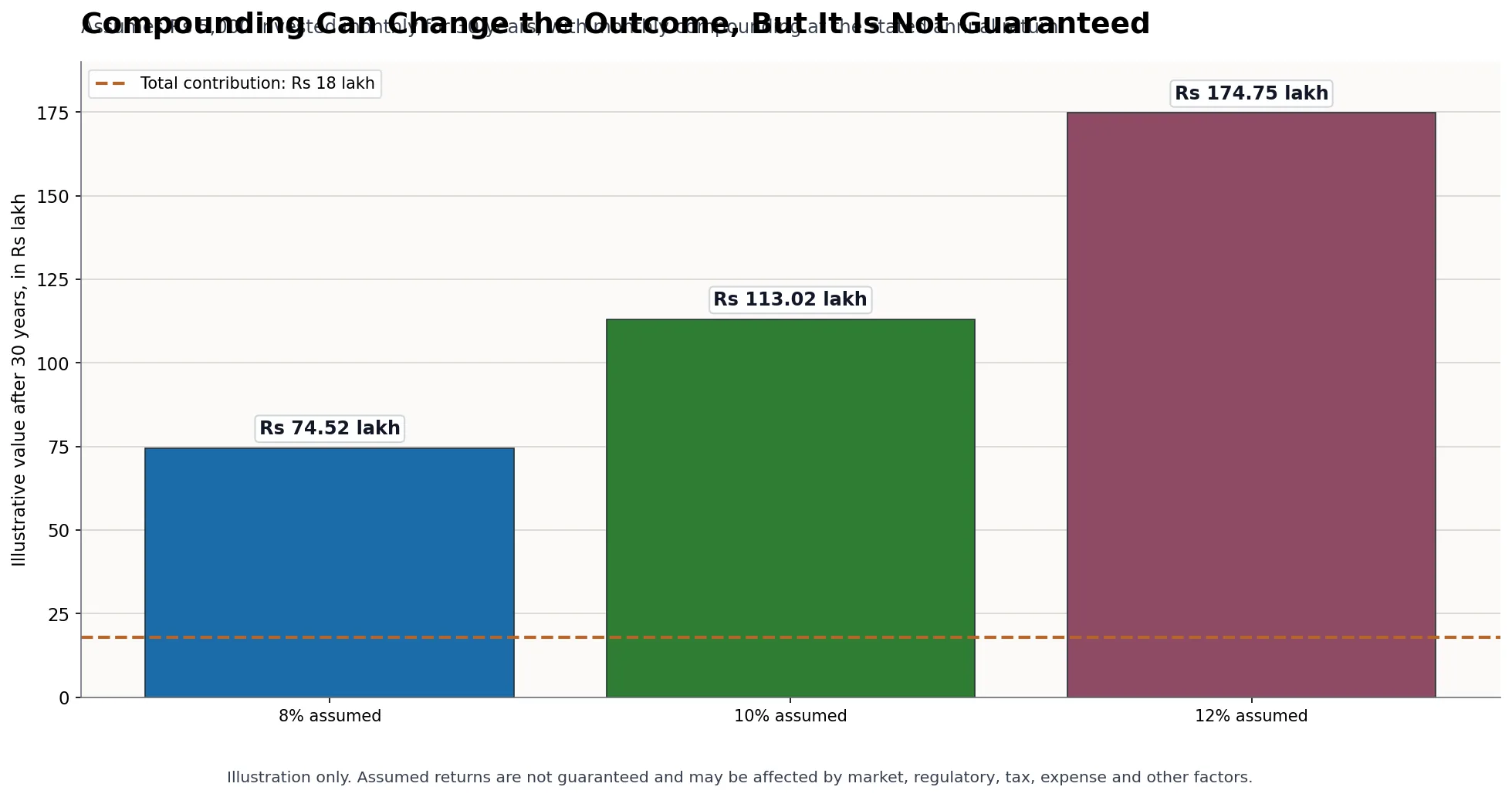

If the same Rs 5,000 monthly contribution is assumed to earn 8%, 10% or 12% per year, compounded monthly, the 30-year illustration changes materially. The total contribution is still Rs 18 lakh, but the assumed corpus becomes about Rs 74.52 lakh at 8%, Rs 1.13 crore at 10% and Rs 1.75 crore at 12%.

| Assumed annual return | Total contribution over 30 years | Illustrative value after 30 years | Illustrative gain over contribution |

|---|---|---|---|

| 8% per year | Rs 18 lakh | Rs 74.52 lakh | Rs 56.52 lakh |

| 10% per year | Rs 18 lakh | Rs 1.13 crore | Rs 95.02 lakh |

| 12% per year | Rs 18 lakh | Rs 1.75 crore | Rs 1.57 crore |

These return figures are purely assumed for investor education. They are not guaranteed, not a prediction of NPS performance and not a promise of any future corpus. Actual returns can be affected by market cycles, asset allocation, pension fund performance, expenses, contribution timing, tax rules, regulatory changes, inflation, interest-rate movements and other unforeseen factors from time to time.

The earlier table deliberately avoids return projections. Actual NPS outcomes depend on asset allocation, pension fund performance, charges, contribution gaps, market conditions and applicable PFRDA rules.

Why NPS Can Help Build The Habit

PFRDA describes Tier I as the default NPS pension account and a retirement savings account. That structure matters because retirement money should not sit in the same mental bucket as weekend spending, annual gadgets or short-term goals.

PFRDA also explains that Tier II is available only to subscribers with an active Tier I account, has no withdrawal restriction and is not eligible for tax benefits. For a retirement-discipline conversation, this distinction is useful: Tier I is the retirement account; Tier II is a more flexible investment account.

The System Is Large, But The Suitability Is Personal

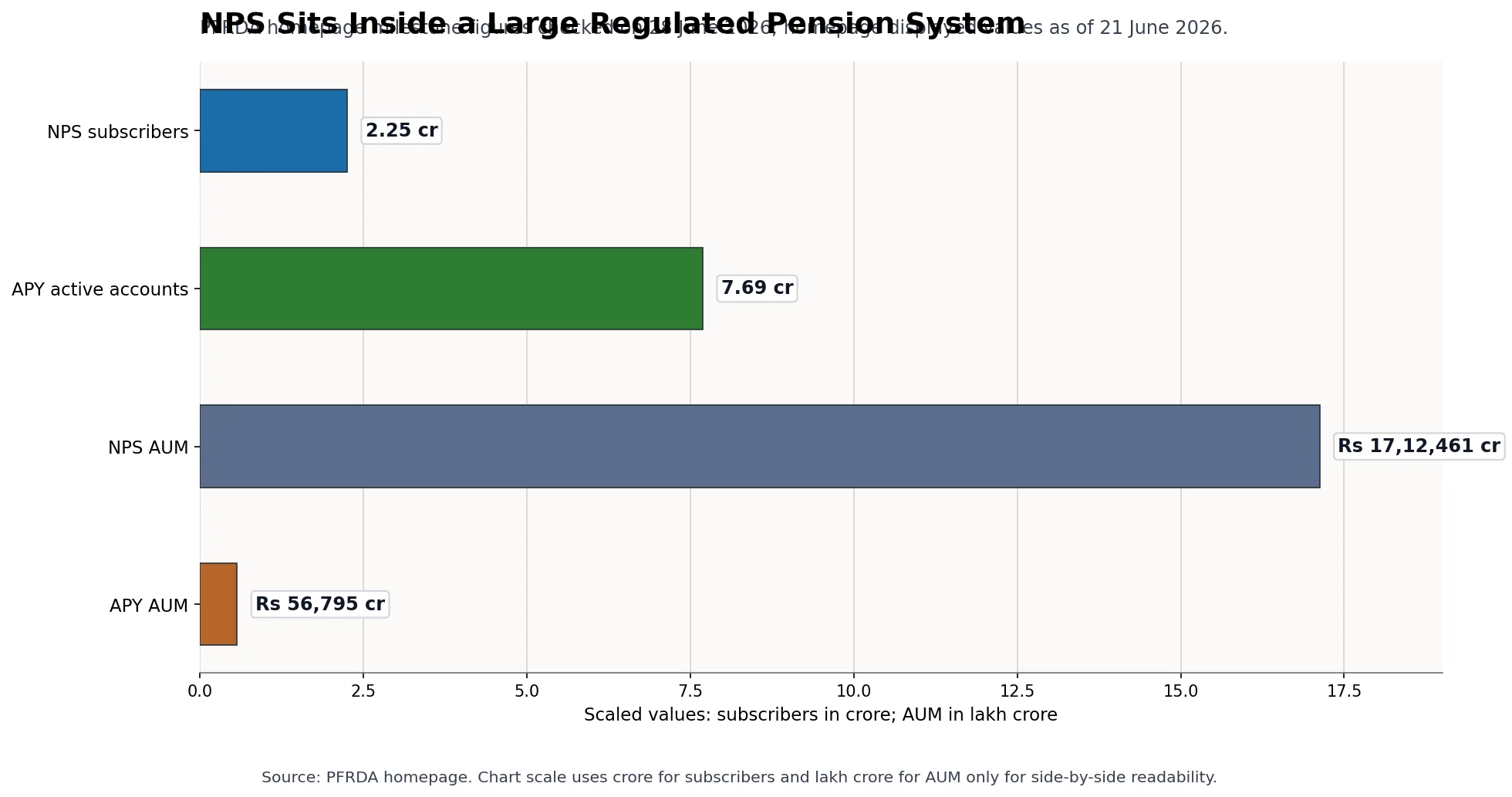

PFRDA's homepage showed NPS total subscribers at 2.25 crore and NPS assets under management at Rs 17,12,461 crore when checked on 28 June 2026. It also showed APY active accounts at 7.69 crore and APY AUM at Rs 56,795 crore.

| Scheme | Subscribers | AUM | Reader takeaway |

|---|---|---|---|

| NPS | 2.25 crore | Rs 17,12,461 crore | Scale shows adoption, not individual suitability. |

| APY | 7.69 crore active accounts | Rs 56,795 crore | Pension awareness is broad, but product choice still depends on the investor's situation. |

The scale is context, not a recommendation. An investor still has to check liquidity needs, emergency reserves, tax regime, risk appetite and retirement horizon.

What To Check Before Starting Rs 5,000 A Month

PFRDA's All Citizen Model page says eligible individuals can voluntarily subscribe to NPS if they are Indian citizens, resident or non-resident, or OCI subscribers, subject to conditions; the page states the age range as 18 to 85 years and requires KYC compliance.

Before starting a monthly NPS contribution, ask five practical questions:

- Can this amount continue even in a difficult month?

- Is emergency money already separate from retirement money?

- Do I understand that NPS is market-linked?

- Do Tier I exit and withdrawal rules fit my retirement objective?

- Am I choosing asset allocation because it suits my risk capacity, not because of one-year performance?

PFRDA's current exit table says normal exit after 60 years or 15 years can allow up to 80% lump sum and at least 20% annuity, while premature exit can allow up to 20% lump sum and at least 80% annuity, subject to corpus-specific and approved payout options. That is why NPS should be evaluated as a retirement account, not as a casual short-term savings product.

For service information, read Abhipra NPS & Pension. To start the process online, visit the NPS account opening link. To set up recurring contributions, use the NPS SIP setup link.

FAQs

Does Rs 5,000 per month guarantee a retirement corpus?

No. The Rs 5,000 example shows contribution discipline only. NPS is market-linked, and the final corpus will depend on investment performance, charges, asset allocation, contribution continuity and rules applicable at exit.

Should I use NPS only for tax saving?

Tax benefits may apply depending on the Income Tax Act and the tax regime applicable to you, but NPS should first be understood as a retirement product. Tax saving alone should not override liquidity and risk considerations.

Can I stop or change the amount later?

NPS allows flexible contributions, but investors should check the current CRA/PFRDA process, minimum contribution rules, tax impact and continuity requirements before changing a contribution routine.

Conclusion

Rs 5,000 a month is not a magic number. It is a practical starting point for investors who want retirement planning to become monthly behavior rather than an annual scramble.

The key is to keep the promise realistic: regular contributions can build discipline, but NPS remains market-linked and rule-bound. Review the amount, asset choice and tax position periodically, and keep emergency money outside the retirement account.

Reviewed by Abhipra Research / Compliance Team.

Source Links

Disclaimer

This article is for educational and informational purposes only. It should not be treated as investment, tax, legal, or retirement planning advice. NPS is a market-linked retirement product and is subject to applicable PFRDA rules, investment risks, tax provisions, and withdrawal conditions. Investors should carefully evaluate their financial goals, risk appetite, investment horizon, liquidity needs and tax situation before making any decision.