Index Funds vs Active Funds: Choose the Process You Can Stay With

Many investors compare index funds and active funds as if one must be permanently superior. The more useful question is different: which investment process fits your goal, cost sensitivity, review discipline and comfort with underperformance?

An index fund generally tries to track a chosen market index. An active fund gives a fund manager discretion to select securities within the scheme mandate and attempt to do better than the relevant benchmark. Both are mutual funds, both carry market risk, and neither removes the need to read scheme documents.

The Core Difference Is Control

An index fund outsources the security-selection decision to the index methodology. The fund's job is to stay close to the chosen index, subject to expenses, tracking difference, cash flows and portfolio execution.

An active fund outsources security selection to the fund manager and investment process. The investor accepts that the fund may outperform, match or underperform its benchmark over different periods.

| Decision factor | Index fund | Active fund |

|---|---|---|

| Portfolio design | Seeks to follow a stated index. | Uses fund-manager selection within the scheme mandate. |

| Main expectation | Broad market participation close to the selected benchmark, after costs and tracking effects. | Potential to differ from the benchmark, positively or negatively. |

| Review focus | Index suitability, tracking difference, expenses, liquidity and fund operations. | Mandate, portfolio, manager process, benchmark comparison, risk, costs and consistency. |

| Behaviour challenge | Staying invested when the chosen index itself performs poorly. | Staying disciplined when the fund trails the benchmark or peers for a period. |

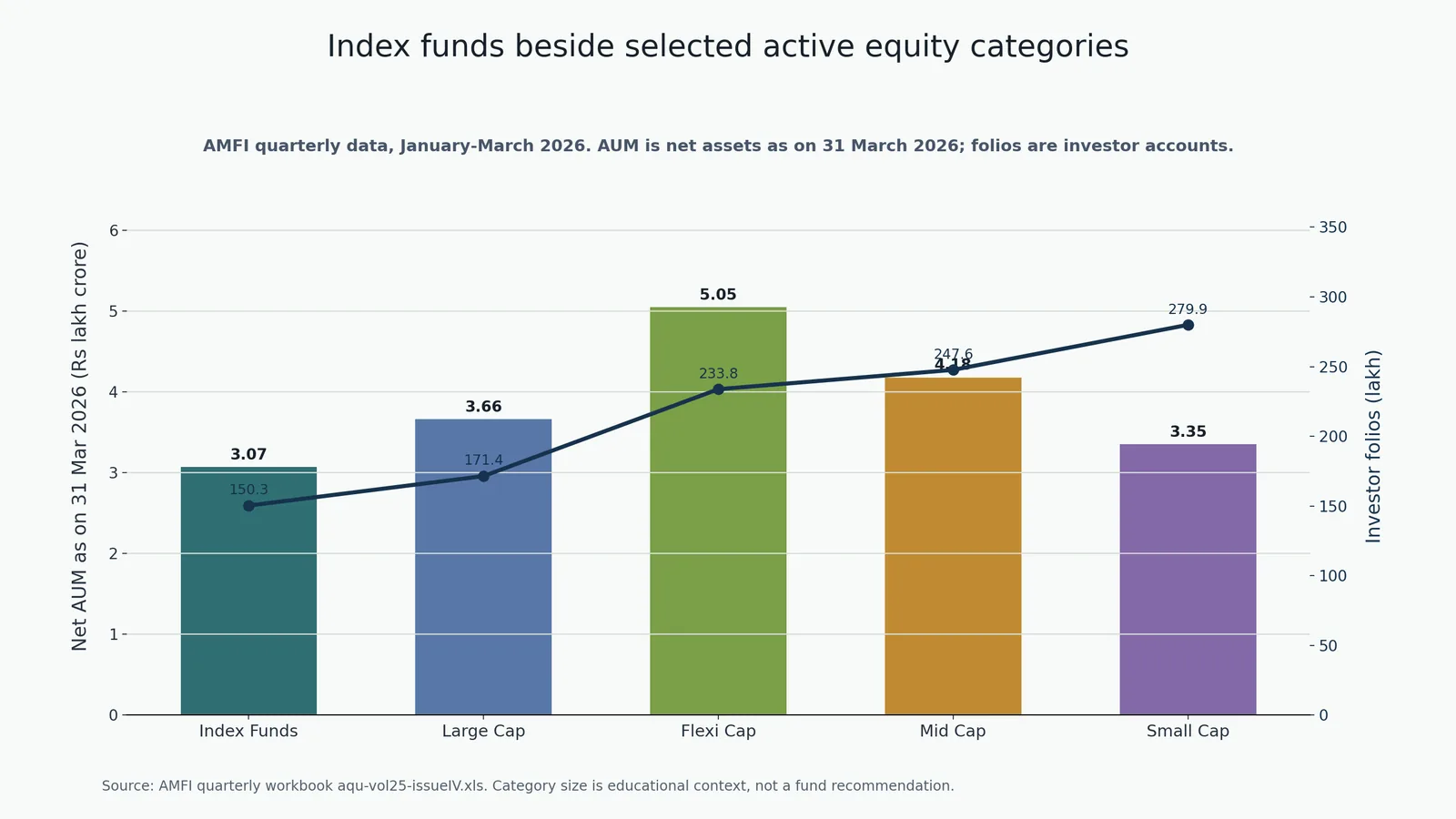

AMFI Data Shows Passive Categories Are No Longer Niche

AMFI's January-March 2026 quarterly data reported open-ended Index Funds with 360 schemes, 1.50 crore folios, net assets of Rs 3,07,315.46 crore as on 31 March 2026 and quarterly net inflow of Rs 11,429.49 crore.

The chart places index funds beside selected active equity categories. Category size is useful context, but it does not decide suitability for a specific investor.

| Category | Schemes | Folios | Net AUM as on 31 Mar 2026 | Quarter net flow |

|---|---|---|---|---|

| Index Funds | 360 | 1,50,30,991 | Rs 3,07,315.46 crore | Rs 11,429.49 crore |

| Large Cap Fund | 34 | 1,71,44,363 | Rs 3,66,045.49 crore | Rs 7,114.49 crore |

| Flexi Cap Fund | 45 | 2,33,79,152 | Rs 5,05,265.45 crore | Rs 24,651.13 crore |

| Mid Cap Fund | 33 | 2,47,63,770 | Rs 4,18,329.20 crore | Rs 13,252.00 crore |

| Small Cap Fund | 36 | 2,79,95,339 | Rs 3,34,662.34 crore | Rs 13,086.73 crore |

When an Index Fund May Be Considered

An index fund may suit an investor who wants a transparent benchmark-linked exposure, does not want to evaluate fund-manager calls deeply, wants cost discipline and is comfortable accepting the return path of the selected index after fund costs and tracking effects.

But the chosen index matters. A broad large-cap index, sector index, factor index and international index can behave very differently. The word "index" does not make every product simple or low risk.

When an Active Fund May Be Considered

An active fund may suit an investor who is willing to review the fund's process, risk, portfolio, mandate, costs and benchmark comparison. The investor should be prepared for periods when the fund does not beat the benchmark or peer group.

Active does not automatically mean better. It means the outcome depends more heavily on the fund's mandate, execution, risk controls and manager decisions.

The decision flow is practical: first choose the asset class and goal, then decide whether benchmark-linked exposure or manager-led selection fits the role. After that, review cost, risk, liquidity, tax impact and documentation.

Common Mistakes

- Choosing an index fund only because it is called passive, without checking the index.

- Choosing an active fund only from recent one-year performance.

- Comparing a low-risk index with a higher-risk active category and calling the result fair.

- Ignoring tracking difference, expense ratio, exit load and taxation.

- Holding too many funds that duplicate the same market exposure.

- Switching repeatedly between active and index funds after every short performance cycle.

- Treating either route as a guarantee against market falls.

Investor Checklist

Before choosing between index and active funds, write down:

- the goal and expected holding period;

- the asset class and category needed for that goal;

- whether the fund's benchmark is suitable;

- expense ratio, exit load and tax treatment;

- Risk-o-meter and scheme documents;

- tracking difference for index funds where relevant;

- active-fund portfolio, mandate and process consistency;

- overlap with existing holdings; and

- a review date that is not driven only by short-term performance.

For account-opening and investment-service information, review Abhipra Services or visit Abhipra eKYC. For a suitability discussion, connect with the Abhipra team before choosing a fund only from online rankings.

Reviewed by Abhipra Research / Compliance Team.

Source Links

- SEBI mutual fund categorisation circular

- SEBI Investor website

- AMFI Research and Information data section

- AMFI Investor Corner

- AMFI Risk-o-meter information

Disclaimer

This article is for educational and informational purposes only. It is not investment advice, tax advice, trading advice or a recommendation to invest in any mutual fund scheme or category. Mutual fund investments are subject to market risks. Read all scheme-related documents carefully before investing. Past performance is not indicative of future returns. Consult a qualified financial adviser and tax adviser before making a financial decision.