ELSS Mutual Funds for Tax Saving: Check the Regime Before You Invest

Many salaried investors first hear about ELSS in the last quarter of the financial year, when proof submission and tax planning become urgent. That timing often creates the wrong question: "Which ELSS should I buy quickly?"

A better first question is: does an ELSS investment actually fit your tax regime, lock-in comfort and equity-risk capacity?

ELSS stands for Equity Linked Savings Scheme. It is an equity-oriented mutual fund category used by many investors for old-regime tax planning under Section 80C. It is still a market-linked investment, not a tax-saving deposit. The tax deduction, lock-in and equity exposure must all make sense together.

First Check: Old Regime or New Regime

The Income Tax Department's AY 2026-27 guidance says the new tax regime under Section 115BAC is the default regime for eligible individual taxpayers, while eligible taxpayers may opt for the old tax regime. The same page separates deductions available under the new regime from deductions available under the old regime.

For old-regime taxpayers, the Income Tax Department lists Section 80C, 80CCC and 80CCD(1) with a combined deduction limit of Rs 1,50,000. The listed 80C items include life insurance premium, provident fund, subscription to certain equity shares, tuition fees, National Savings Certificate, housing-loan principal and other eligible items.

That means ELSS should not be bought only because it carries a tax-saving label. First check whether you are using the old regime, whether you still have unused 80C space and whether other eligible payments have already filled the limit.

| Question | Why it matters | Action before investing |

|---|---|---|

| Are you staying in the old tax regime? | Section 80C is an old-regime planning item. The new regime has fewer deductions. | Compare old and new regime using current income, deductions and surcharge/cess impact. |

| How much 80C space is still unused? | The combined 80C/80CCC/80CCD(1) deduction limit is Rs 1,50,000. | Reduce EPF, insurance premium, eligible tuition fees, housing-loan principal and other eligible items from the limit. |

| Can the money stay locked in? | ELSS is not emergency money. Redemption cannot be treated like a normal liquid reserve. | Keep emergency funds and near-date commitments separate before making a tax-saving investment. |

| Can you accept equity volatility? | ELSS is an equity mutual fund category, so value can move materially with markets. | Read the scheme objective, portfolio, costs, Risk-o-meter and scheme documents. |

ELSS Is Tax Planning Plus Equity Risk

An ELSS investment can be useful for an old-regime taxpayer who wants equity exposure and still has 80C capacity. But tax benefit should not hide the investment risk.

Key points to remember:

- ELSS is a mutual fund investment, not a guaranteed-return tax product.

- The portfolio is market-linked and can decline in value.

- Past returns, star ratings and recent rankings should not be treated as a prediction.

- Lock-in does not remove market risk; it only restricts liquidity.

- Tax treatment can change, and the investor's own regime choice can change the usefulness of the deduction.

The practical sequence is simple: decide the tax regime, calculate unused 80C room, confirm liquidity, then evaluate whether equity exposure fits the goal.

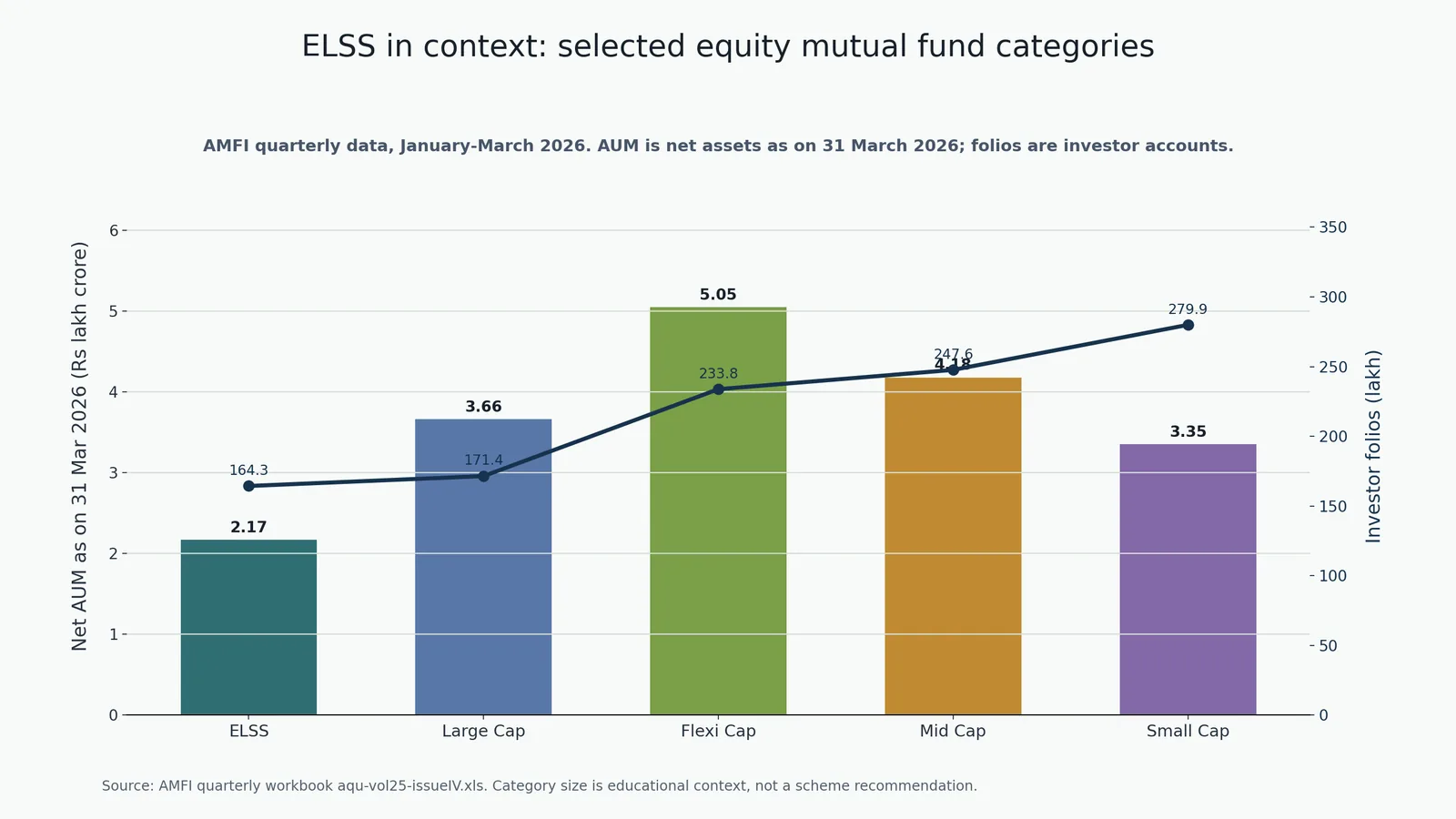

AMFI Data: ELSS Is a Meaningful Equity Category

AMFI's quarterly data for January-March 2026 reported open-ended ELSS category net assets of Rs 2,17,309.84 crore as on 31 March 2026, with 1.64 crore investor folios. It also reported a net outflow of Rs 1,681.05 crore for the quarter.

The chart places ELSS beside selected equity categories. Category size is useful context, but it is not a recommendation to buy any scheme or category.

| Category | Schemes | Folios | Net AUM as on 31 Mar 2026 | Quarter net flow |

|---|---|---|---|---|

| ELSS | 41 | 1,64,33,567 | Rs 2,17,309.84 crore | -Rs 1,681.05 crore |

| Large Cap Fund | 34 | 1,71,44,363 | Rs 3,66,045.49 crore | Rs 7,114.49 crore |

| Flexi Cap Fund | 45 | 2,33,79,152 | Rs 5,05,265.45 crore | Rs 24,651.13 crore |

| Mid Cap Fund | 33 | 2,47,63,770 | Rs 4,18,329.20 crore | Rs 13,252.00 crore |

| Small Cap Fund | 36 | 2,79,95,339 | Rs 3,34,662.34 crore | Rs 13,086.73 crore |

A Sensible ELSS Decision Flow

Use this sequence before selecting a scheme:

- Estimate tax under both regimes using current salary, deductions and other income.

- If the old regime is still suitable, calculate unused 80C room.

- Confirm that emergency money, rent, EMI, school fees and near-date obligations are already protected.

- Decide whether equity exposure is appropriate for the investment horizon.

- Compare scheme documents, expense ratio, portfolio, Risk-o-meter, fund manager process and consistency.

- Avoid selecting a scheme only from one-year return, social-media lists or last-minute proof-submission pressure.

- Keep nomination, PAN, bank account, FATCA and KYC details updated.

Where ELSS Can Fit

ELSS may fit an investor who:

- is consciously using the old regime;

- has 80C capacity left after other eligible items;

- wants equity exposure for a suitable time horizon;

- does not need the money for emergency liquidity; and

- can stay disciplined through market falls.

It may not fit an investor who is using the new regime, has already exhausted the 80C limit, needs money soon, wants assured maturity value or cannot tolerate equity volatility.

Common Mistakes

- Buying ELSS after the 80C limit is already exhausted.

- Choosing ELSS only because a colleague submitted it as tax proof.

- Treating the lock-in period as a return guarantee.

- Comparing ELSS with provident fund, insurance premium or home-loan principal without considering risk and liquidity differences.

- Investing a lump sum in March without checking asset allocation.

- Redeeming as soon as lock-in ends even when the goal still needs equity exposure.

- Ignoring exit strategy, capital gains tax, nomination and documentation.

Action Checklist

Before making an ELSS investment, write down:

- chosen tax regime for the year;

- unused 80C amount;

- amount already covered by EPF, tuition fees, insurance premium and loan principal;

- reason for choosing equity exposure;

- minimum holding expectation beyond the lock-in;

- risk level shown in scheme documents;

- cost and portfolio concentration;

- nomination and KYC status; and

- review date after the tax season.

For account-opening and investment-service support, review Abhipra Services or visit Abhipra eKYC. For an ELSS suitability discussion, connect with the Abhipra team before making a rushed tax-saving purchase.

Reviewed by Abhipra Research / Compliance Team.

Source Links

- Income Tax Department: Salaried Individuals for AY 2026-27

- SEBI mutual fund categorisation circular

- AMFI Research and Information data section

- AMFI Investor Corner

- AMFI Risk-o-meter information

- SEBI Investor website

Disclaimer

This article is for educational and informational purposes only. It is not investment advice, tax advice, trading advice, legal advice or a recommendation to invest in any scheme. Mutual fund investments are subject to market risks. Read all scheme-related documents carefully before investing. Tax benefits depend on the applicable law, tax regime, eligibility and individual facts. Past performance is not indicative of future returns. Consult a qualified financial adviser and tax adviser before making a financial decision.