Hybrid Funds for First-Time Investors: Helpful Shortcut or Misunderstood Risk?

For a first-time mutual fund investor, the hardest question is often not "which fund has the highest return?" It is "how much equity risk can I handle without panicking, and how much stability do I need?" Hybrid mutual funds try to answer that by investing across more than one asset type, usually some mix of equity, debt, arbitrage or other permitted assets.

What A Hybrid Fund Actually Does

A hybrid fund is not a capital-protection product. It is still a mutual fund scheme. The difference is that the scheme mandate allows the fund manager to hold more than one asset type within the same scheme category.

SEBI's mutual fund categorisation framework lists hybrid scheme categories such as conservative hybrid, balanced or aggressive hybrid, dynamic asset allocation or balanced advantage, multi asset allocation, arbitrage and equity savings funds. Each category has its own investment mandate, so two "hybrid" funds may behave very differently.

For a new investor, this matters because the word hybrid only tells you that the fund blends assets. It does not tell you whether the fund is conservative, equity-heavy, tactical, arbitrage-focused or suitable for your time horizon.

Where Hybrid Funds May Help A New Investor

Hybrid funds can be useful when an investor wants a simpler starting point than managing separate equity and debt funds. A suitable hybrid category may reduce the need to manually rebalance between asset classes every few months.

They may also help investors who understand that some equity exposure is needed for long-term goals but are not comfortable starting with a pure equity fund. A conservative or balanced structure can feel easier to hold through normal market movement, provided the investor has read the scheme document and risk-o-meter.

The important word is "may". A hybrid fund is not automatically safe. If the portfolio has meaningful equity exposure, its value can fall. If it holds debt securities, interest-rate and credit risks still matter. If it uses arbitrage, returns depend on market spreads and costs.

The Category Choice Matters More Than The Label

For first-time investors, the right question is not "Are hybrid funds good?" The better question is "Which hybrid category matches my goal, holding period, risk tolerance and tax position?"

- Conservative hybrid funds generally suit investors who want lower equity exposure than equity-oriented hybrids.

- Aggressive hybrid or balanced hybrid funds may carry higher equity-linked volatility.

- Dynamic asset allocation or balanced advantage funds can change equity and debt exposure based on the scheme's model, but the model can still be wrong for your personal situation.

- Multi asset allocation funds spread exposure across at least three asset classes under the scheme mandate, but that does not remove market risk.

- Arbitrage and equity savings funds are often used for different purposes from long-term wealth creation, so investors should check whether the strategy matches the goal.

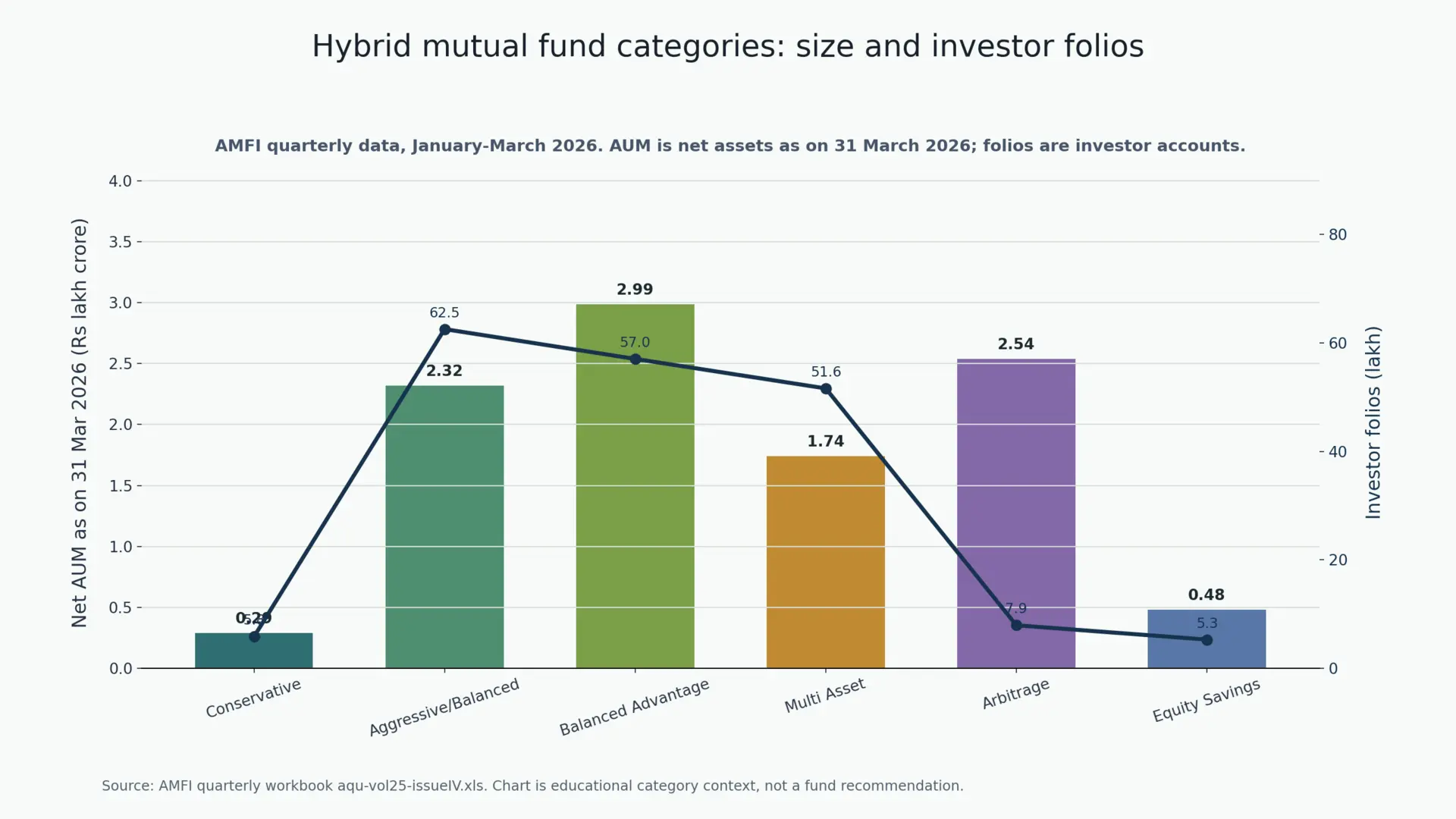

What AMFI Data Says About Investor Use

AMFI's January-March 2026 quarterly workbook shows that hybrid categories are not a small corner of the market. As on 31 March 2026, dynamic asset allocation or balanced advantage funds had Rs 2.99 lakh crore of net AUM, arbitrage funds had Rs 2.54 lakh crore, and aggressive or balanced hybrid funds had Rs 2.32 lakh crore. The folio count was also high in aggressive or balanced hybrid funds and balanced advantage funds.

The graph compares AMFI-reported net AUM and folios for major hybrid categories. The AUM bars show category size; the line shows investor folios. A larger category does not make a fund suitable by itself, but it helps investors see how different hybrid categories are used in the market.

| Hybrid category | Schemes | Folios | Net AUM as on 31 March 2026 | Net inflow during Jan-Mar 2026 |

|---|---|---|---|---|

| Conservative Hybrid Fund | 18 | 5.80 lakh | Rs 0.29 lakh crore | Rs -363.43 crore |

| Balanced Hybrid Fund / Aggressive Hybrid Fund | 31 | 62.55 lakh | Rs 2.32 lakh crore | Rs 4,091.90 crore |

| Dynamic Asset Allocation / Balanced Advantage Fund | 36 | 57.05 lakh | Rs 2.99 lakh crore | Rs 3,078.47 crore |

| Multi Asset Allocation Fund | 34 | 51.61 lakh | Rs 1.74 lakh crore | Rs 24,174.37 crore |

| Arbitrage Fund | 38 | 7.90 lakh | Rs 2.54 lakh crore | Rs -17,228.55 crore |

| Equity Savings Fund | 24 | 5.26 lakh | Rs 0.48 lakh crore | Rs -951.85 crore |

A Simple First-Time Investor Filter

Before choosing any hybrid fund, check five things:

- Goal: Is the money for a long-term goal, a short-term parking need or emergency liquidity?

- Time horizon: Can you stay invested through market movements without needing the money suddenly?

- Asset mix: How much equity, debt, arbitrage or other exposure can the scheme hold?

- Costs and taxation: What are the expense ratio, exit load and tax treatment for your holding period?

- Behaviour: Will you continue the plan when the equity part falls or when another category temporarily performs better?

Portfolio Balance Reminder

This visual reinforces a practical selection rule: first-time investors should look beyond recent returns, define their need for growth, stability and liquidity, and then compare the scheme category and documents with that personal requirement.

Common Mistakes

- Treating every hybrid fund as low risk.

- Choosing a balanced advantage fund without understanding how its model changes allocation.

- Using a long-term equity-oriented hybrid fund for money needed in a few months.

- Ignoring exit load, tax treatment, debt quality and scheme concentration.

- Switching categories after every short-term performance cycle.

Bottom Line

Hybrid funds can be a practical first step for investors who want a professionally managed asset mix, but they are not a universal answer. A first-time investor should start with the goal, emergency fund, time horizon and risk capacity, then choose the category only if the scheme mandate fits.

Reviewed by Abhipra Research / Compliance Team.

Source Links

- SEBI circular on categorisation and rationalisation of mutual fund schemes

- AMFI data page

- AMFI January-March 2026 quarterly workbook

- AMFI investor resources

- SEBI investor website

Disclaimer

This article is for investor education only and is not investment advice, tax advice, legal advice, research recommendation or a solicitation to buy or sell any mutual fund scheme or security. Mutual fund investments are subject to market risks. Investors should read all scheme-related documents carefully and consult a qualified adviser for suitability.