How to Choose the Right Mutual Fund: Start With the Goal, Not the Ranking

A mutual fund is easy to buy, but not always easy to choose. The confusing part is not the online transaction; it is deciding whether a fund actually fits the job you want it to do.

Many investors begin with a ranking, a recent return number or a friend's SIP. A better starting point is simpler: define the goal, then shortlist only the categories that match the time horizon, risk capacity and liquidity need.

First Decide The Job Of The Money

Before looking at any scheme name, write one sentence: "This money is for..."

That sentence changes the selection. A fund meant for a three-year home down-payment reserve should not be judged like a fund meant for a child's higher education 12 years away. A fund for emergency liquidity should not be pushed into a high-volatility category just because recent returns look attractive.

The practical order is:

- Goal and amount.

- Time horizon.

- Capacity to tolerate temporary losses.

- Need for liquidity.

- Tax position and exit load.

- Category and scheme comparison.

Category Comes Before Scheme Name

SEBI's categorisation framework was designed to make mutual fund categories more comparable. That matters for investors because a large-cap fund, a mid-cap fund, a liquid fund, an aggressive hybrid fund and an index fund are not competing for the same job.

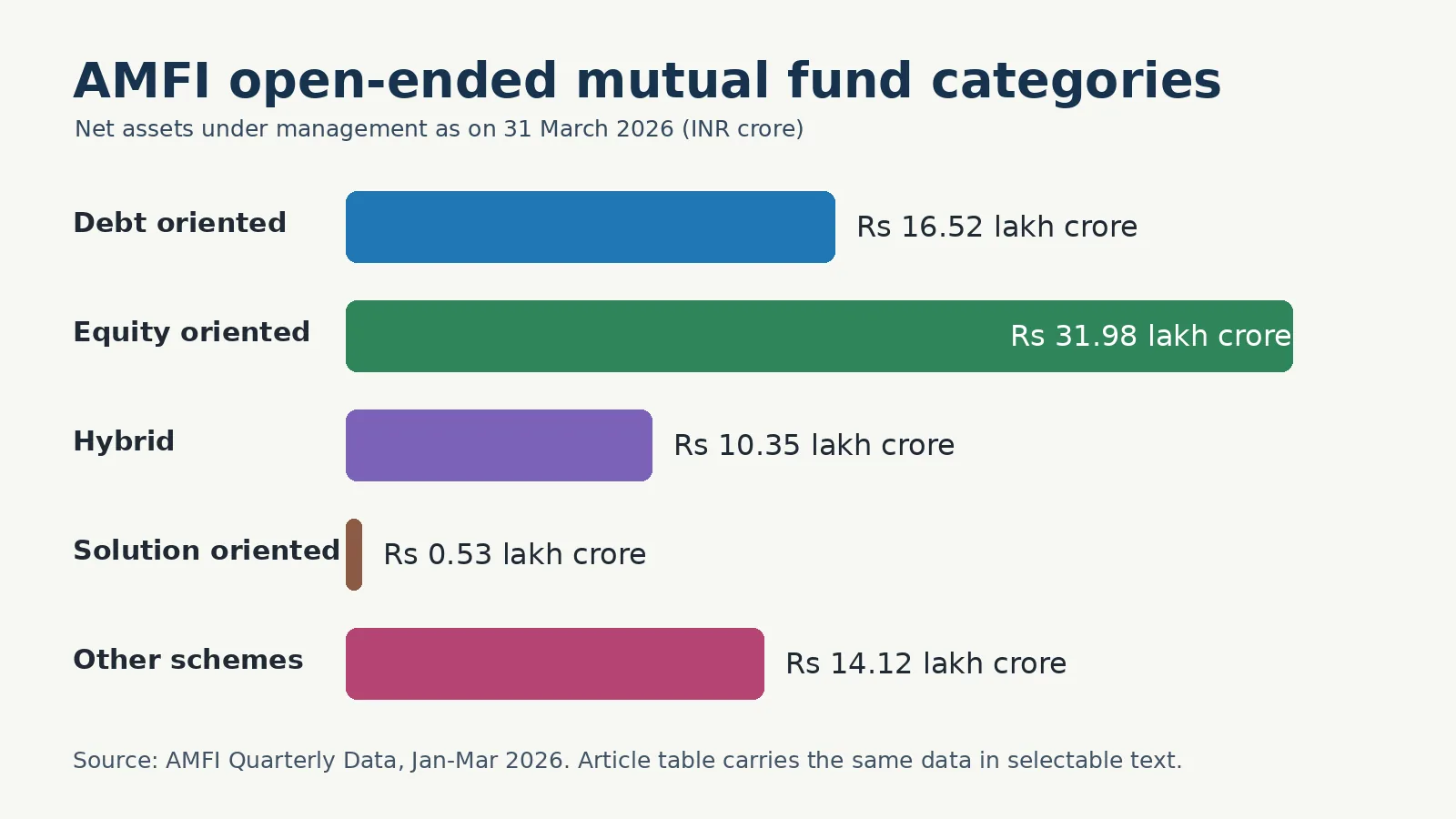

AMFI's official Jan-Mar 2026 quarterly data also shows how broad the open-ended mutual fund universe is. As on 31 March 2026, open-ended schemes had Rs 73.49 lakh crore of net assets under management across 1,865 schemes and 27.35 crore folios. Equity-oriented schemes formed the largest open-ended bucket in this AMFI table at about Rs 31.98 lakh crore.

| Open-ended category | No. of schemes | Folios | Net AUM | Selection takeaway |

|---|---|---|---|---|

| Debt oriented | 335 | 82.84 lakh | Rs 16.52 lakh crore | Start with duration, credit quality and liquidity need. |

| Equity oriented | 568 | 18.27 crore | Rs 31.98 lakh crore | Match market-cap exposure and volatility with the goal horizon. |

| Hybrid | 181 | 1.90 crore | Rs 10.35 lakh crore | Check equity-debt mix and whether the fund solves your asset-allocation problem. |

| Solution oriented | 41 | 63.03 lakh | Rs 0.53 lakh crore | Read lock-in, suitability and goal-specific constraints carefully. |

| Other schemes | 740 | 5.71 crore | Rs 14.12 lakh crore | Understand whether the fund is passive, ETF-linked, gold-linked or otherwise specialised. |

The table is not a recommendation for any category. It simply shows why a ranking-first question is the wrong first question. The fund category must match the job.

What To Check Before Comparing Returns

Once the category is right, compare schemes on the same playing field.

Look at the scheme information document, benchmark, portfolio, fund objective and AMFI/AMC disclosures. The Risk-o-meter is important because it gives a quick view of the scheme's risk label, but it should not be the only test.

Use this order:

- Scheme objective: does it match the goal?

- Risk-o-meter and portfolio risk: can you tolerate the volatility or credit risk?

- Benchmark: is the scheme being measured against the right yardstick?

- Costs: expense ratio, exit load and transaction costs matter more over long holding periods.

- Consistency: compare rolling behaviour and drawdowns, not just one-year return.

- Portfolio overlap: avoid buying five funds that quietly own very similar exposures.

- Tax treatment: understand how redemption timing and fund type may affect post-tax outcome.

A Simple Selection Workflow

The workflow is intentionally conservative. First filter by goal and time horizon. Then choose the category. Then remove schemes whose risk, liquidity, cost or portfolio fit does not suit the investor. Only after that should performance comparison enter the discussion.

For example, if the goal is seven to ten years away and the investor can tolerate market volatility, an equity-oriented category may be evaluated. If the money may be needed soon, the investor should not force the same money into a high-risk category merely because a return chart looks attractive.

Common Mistakes

- Choosing a fund because it topped a short-term return table.

- Comparing funds from different categories as if they have the same mandate.

- Ignoring exit load, taxation and liquidity.

- Treating SIP as protection against loss.

- Owning too many funds with overlapping portfolios.

- Not reviewing whether the original goal has changed.

Investor Checklist

Before investing, ask:

- What goal will this fund serve?

- What is the minimum time horizon for this money?

- What category fits that horizon and risk level?

- What does the scheme invest in today?

- What does the Risk-o-meter say?

- What are the expense ratio and exit load?

- Does this fund duplicate something already in my portfolio?

- How will I review it without reacting to every market move?

Investors who want help with account opening, mutual fund access, portfolio review or investment services can review Abhipra Services or complete the Abhipra eKYC journey.

Reviewed by Abhipra Research / Compliance Team.

Source Links

- AMFI Monthly / Quarterly Data

- AMFI Jan-Mar 2026 quarterly data workbook

- AMFI Risk Parameters

- SEBI: Categorization and Rationalization of Mutual Fund Schemes

- Abhipra Services

Disclaimer

This article is for educational and informational purposes only. It is not investment, trading, tax, legal or insurance advice. Mutual fund investments are subject to market risks. Read all scheme-related documents carefully and evaluate the scheme objective, risk, costs, liquidity, time horizon, taxation and suitability before investing. Past performance does not indicate future returns, and SIPs or mutual fund investments do not assure returns or protect against loss.