The Quiet Force of Compounding: Why Time Can Matter More Than Amount

Most investors notice the amount they invest. Fewer notice the calendar.

That is why compounding often feels boring in the beginning. The first few years may look slow. The later years can look surprisingly powerful because earlier gains also get time to participate.

The real lesson is not “invest big immediately”. It is simpler: give good financial habits enough years to work, and do not interrupt them casually.

Compounding Is Not Magic. It Is Reinvestment Plus Time

Compounding means returns start earning returns. If money earns a return and that return stays invested, the next period starts on a larger base.

That is very different from simple interest thinking, where the original principal feels like the only worker. In compounding, time gradually adds more workers.

For investors, this matters because many real-life decisions are not about one perfect product. They are about habits:

- starting earlier rather than waiting for a “perfect” income level;

- increasing contributions when income rises;

- avoiding unnecessary withdrawals from long-term money;

- staying diversified instead of chasing one hot idea; and

- reviewing risk without restarting from zero every few years.

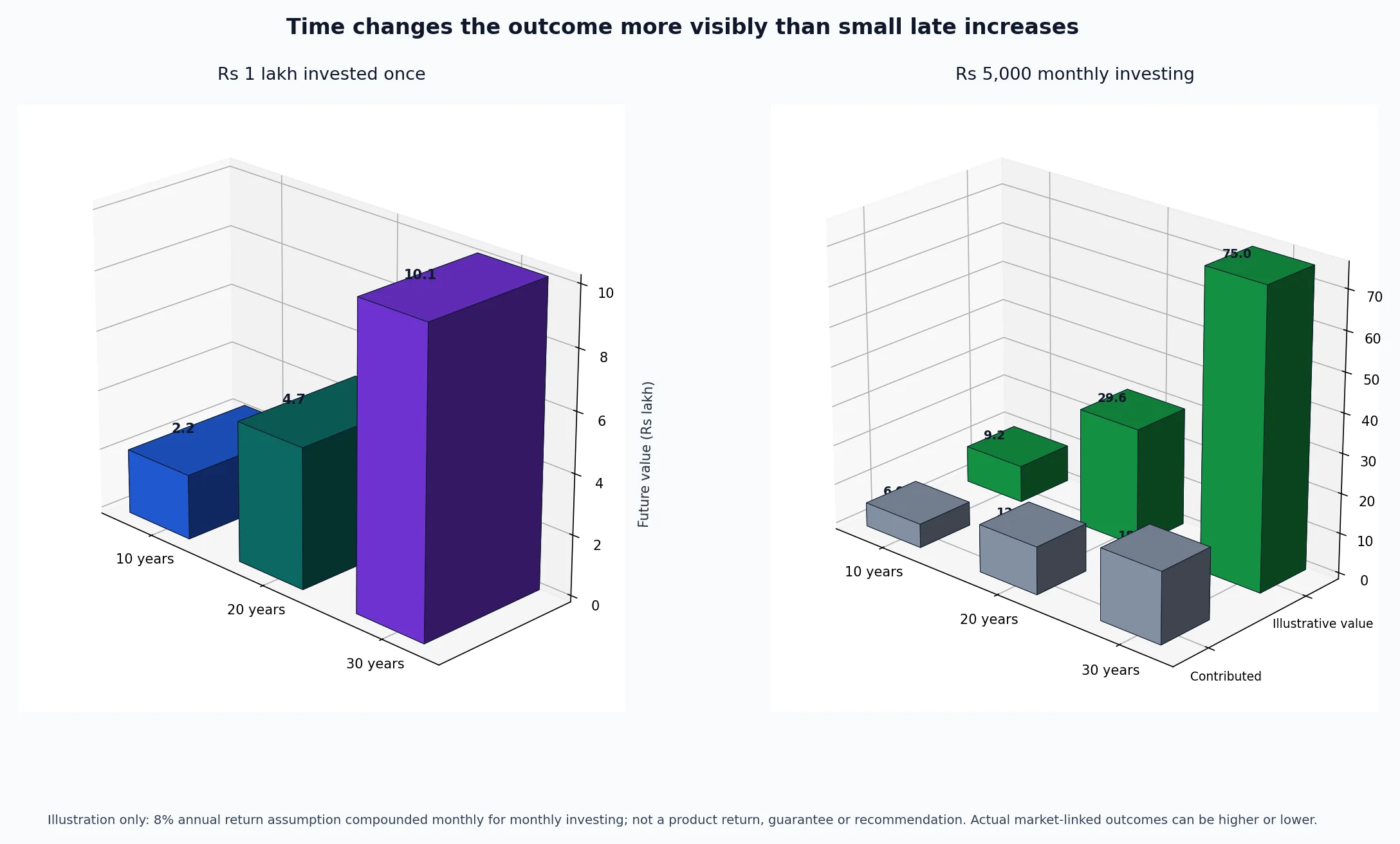

The Chart: Same Rate, Different Time

The chart uses one transparent assumption: 8% annual return, compounded annually for the lump-sum example and monthly for the monthly-investment example. It is not a forecast, product return, guarantee or recommendation.

The first panel shows what happens to Rs 1 lakh invested once:

- 10 years: about Rs 2.16 lakh

- 20 years: about Rs 4.66 lakh

- 30 years: about Rs 10.06 lakh

The second panel shows Rs 5,000 invested monthly under the same annual assumption:

- 10 years: Rs 6 lakh contributed, about Rs 9.21 lakh illustrative value

- 20 years: Rs 12 lakh contributed, about Rs 29.65 lakh illustrative value

- 30 years: Rs 18 lakh contributed, about Rs 75.01 lakh illustrative value

The point is not that investors should expect 8%. Actual outcomes depend on asset class, product cost, tax, timing, market volatility and investor behaviour. The point is that longer periods can give compounding more room to show up.

Why Late Starts Feel Expensive

A late start does not make wealth creation impossible. It changes the burden.

When time is short, the investor may need one or more of these:

- a higher monthly contribution;

- a lower target corpus;

- a later goal date;

- a higher-risk portfolio, if suitable; or

- additional income sources.

That is why delaying investment decisions can quietly reduce flexibility. A person who starts early can often build the habit with smaller steps. A person who starts late may have to run harder, accept more trade-offs, or both.

Time Helps Only When The Money Is Suitable For The Time Horizon

Compounding is not a reason to put every rupee into risky assets.

Short-term money needs stability and access. Emergency funds, near-term school fees, a house down payment due soon, or business cash flow should not be forced into volatile products merely because compounding sounds attractive.

Long-term money can usually tolerate more fluctuation, but even there the investor should ask:

- What is the goal?

- When will the money be needed?

- Can the goal date move?

- What loss can the household tolerate without panic?

- Are emergency reserves already separate?

- What costs, exit loads and taxes apply?

Compounding rewards time, but suitability decides where that time should be used.

The Behaviour Trap: Interrupting Too Often

Many investors understand compounding on paper but interrupt it in practice.

Common interruptions include:

- stopping SIPs during normal market falls;

- withdrawing long-term investments for avoidable spending;

- switching products every year based on recent performance;

- expecting linear returns from market-linked assets;

- using debt meant for emergency needs to buy risky products; and

- treating social-media return claims as planning assumptions.

The AMFI Research and Information data section and AMFI Investor resources can help investors review mutual-fund industry data and basic investor education. The SEBI Investor website also provides investor education and grievance resources. These sources are useful reminders that investing should be documented, diversified and understood before money is committed.

A Practical Compounding Checklist

Before relying on compounding for any goal, write down:

- the goal amount and target date;

- the monthly or lump-sum amount you can sustain;

- the asset mix suitable for that goal;

- the review date, preferably not every week;

- what would make you stop or reduce contributions;

- the tax treatment and costs; and

- nomination, KYC and account-access details.

For long-term goals, the most useful question may be: What can I continue without drama?

Small, boring, repeatable actions often beat large, emotional decisions that do not survive volatility.

Where Abhipra Can Help

Investors who want to start with account-opening, demat, mutual-fund or investment-service support can review Abhipra Services or complete the Abhipra eKYC journey.

A useful first conversation is not “Which product should I buy first?” It is “Which goal am I funding, how long do I have, and what risk can I actually stay with?”

Reviewed by Abhipra Research / Compliance Team.

Source Links

- AMFI Research and Information data section

- AMFI Investor resources

- SEBI Investor website

- RBI Financial Education

- Abhipra Services

Disclaimer

This article is for educational and informational purposes only. It should not be considered investment advice, trading advice, tax advice or insurance advice. Investments in securities market are subject to market risks. Please read all related documents carefully before investing. Past performance is not indicative of future returns. The chart uses a simplified assumption only and does not represent any product return or guarantee. Please consult a qualified financial advisor, tax advisor or insurance advisor before making any financial decision.