Equity, Debt, Gold and Cash: How to Build Your First Portfolio Without Guesswork

When Aditi received her first annual bonus, she had four different voices in her head.

One said, “Put it in shares.” Another said, “Keep it safe.” A third said, “Buy gold.” The fourth whispered, “What if you need the money next month?”

That confusion is normal. A first portfolio is not built by finding one perfect product. It is built by giving every rupee a job.

Start With the Job, Not the Asset

Equity, debt, gold and cash do different jobs:

- Cash handles near-term needs and emergencies.

- Debt can add relative stability and planned-income behaviour, but still carries interest-rate, credit and liquidity risks depending on the product.

- Equity is used for long-term growth participation, with higher volatility and the possibility of loss.

- Gold may act as a diversifier during some stress periods, but it does not produce guaranteed income and can also be volatile.

The mistake is asking, “Which one is best?” A better first question is:

When will I need this money, and what risk can this specific goal tolerate?

The First Bucket Is Cash

Cash is not glamorous, and it is not meant to win a long-term return contest. Its job is to stop a surprise expense from forcing you to sell investments at the wrong time.

For a beginner, this bucket usually comes before market-linked investing. It may include bank balance, sweep deposits or other highly accessible money. A liquid mutual fund or money-market fund may help with short-term parking for some investors, but it should not be treated as identical to emergency bank cash.

The key test is simple: if a medical bill, job gap or urgent family expense appears, can you access money without disturbing long-term investments?

Debt Is the Stability Bucket, Not a No-Risk Bucket

Debt investments can include deposits, bonds, debt mutual funds or other fixed-income products. They often look calmer than equity, but “debt” is not a single risk level.

Debt mutual funds can face interest-rate movement, credit events, liquidity stress, expense impact and taxation rules. Before choosing any scheme, investors should read the scheme objective, portfolio quality, duration, costs and Risk-o-meter. AMFI provides scheme risk information and Risk-o-meter information.

Debt works best when it is matched to a goal's time horizon and the investor understands what can go wrong.

Equity Is the Growth Bucket That Tests Behaviour

Equity can help a long-term portfolio participate in business growth. It also tests patience.

A first-time investor should not confuse long-term growth potential with short-term certainty. Equity can fall sharply and remain uncomfortable for longer than expected. That is why equity money should usually be money with time, purpose and emotional tolerance.

For beginners, diversified routes such as mutual funds may be easier to manage than selecting individual shares immediately. Direct equity requires research, position sizing and continuous monitoring.

Gold Is a Diversifier, Not a Retirement Plan by Itself

Gold is often emotionally familiar in Indian households. It may provide diversification because it can behave differently from equity or debt in some periods.

But gold has limits. It does not produce business earnings, interest or rent. Its price can also move sharply. A first portfolio should not use gold as a substitute for an emergency fund, insurance, retirement planning or goal-based investing.

Gold's role, if any, should be written clearly: why it is held, how much is enough for that household, and when it will be reviewed.

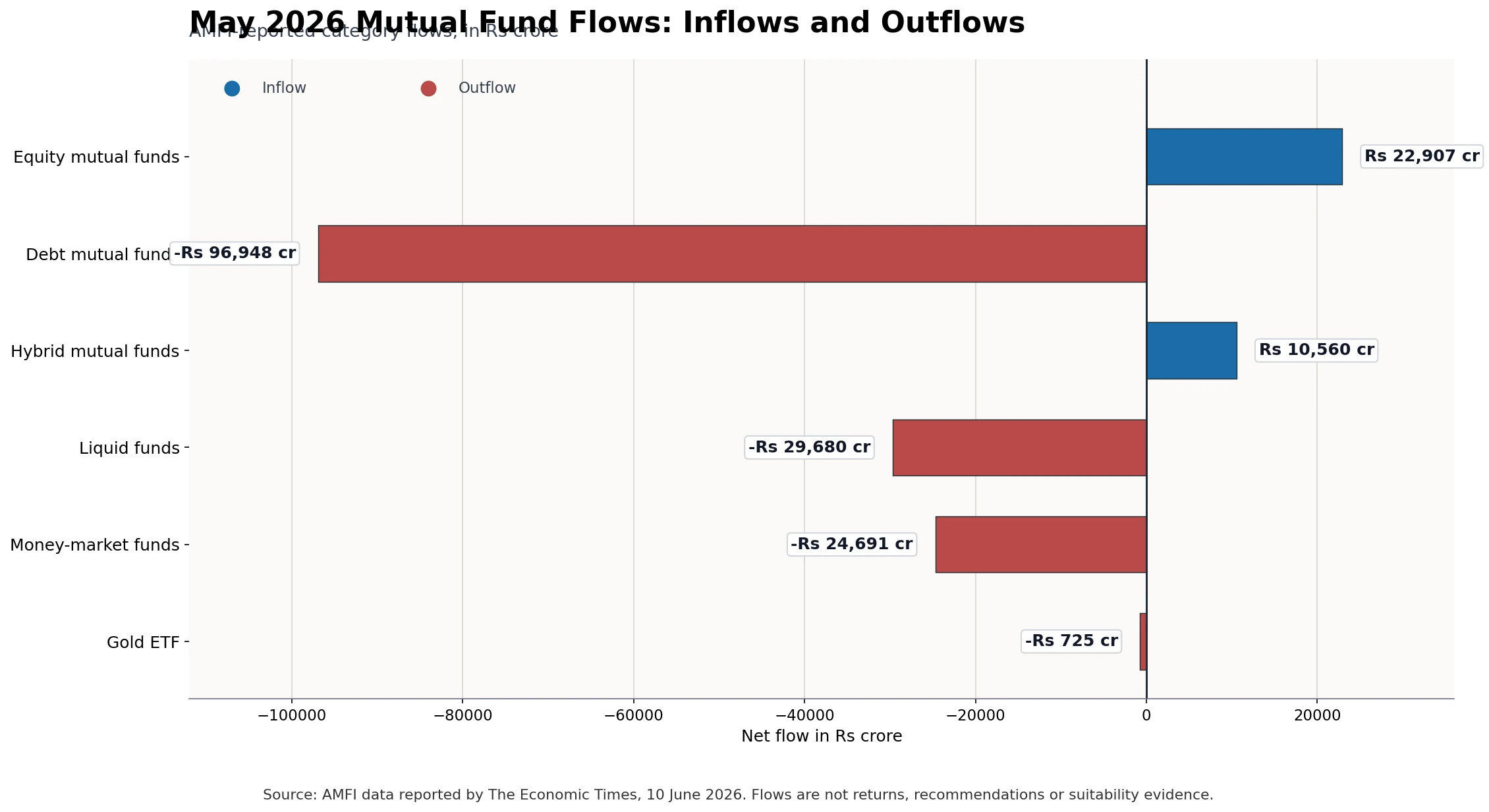

Current Fund-Flow Data Shows Why Buckets Behave Differently

AMFI data reported by The Economic Times on June 10, 2026 showed very different mutual fund flows in May 2026:

| Bucket shown in chart | May 2026 net flow | How a beginner should read it |

|---|---|---|

| Equity mutual funds | ₹22,907 crore inflow | Equity continued to attract money, but inflows do not guarantee future returns. |

| Debt mutual funds | ₹96,948 crore outflow | Debt categories can see large institutional and treasury movements. |

| Hybrid mutual funds | ₹10,560 crore inflow | Mixed-asset products can appeal to investors, but scheme allocation and risk still matter. |

| Liquid funds | ₹29,680 crore outflow | Cash-management categories can move with short-term liquidity needs. |

| Money-market funds | ₹24,691 crore outflow | Short-duration categories are not the same as household emergency cash. |

| Gold ETFs | ₹725 crore outflow | Gold flows can change, so gold should not be held only because it is currently popular. |

This chart is useful because it shows that asset buckets behave differently. It is not a signal to chase whichever bucket received money in one month.

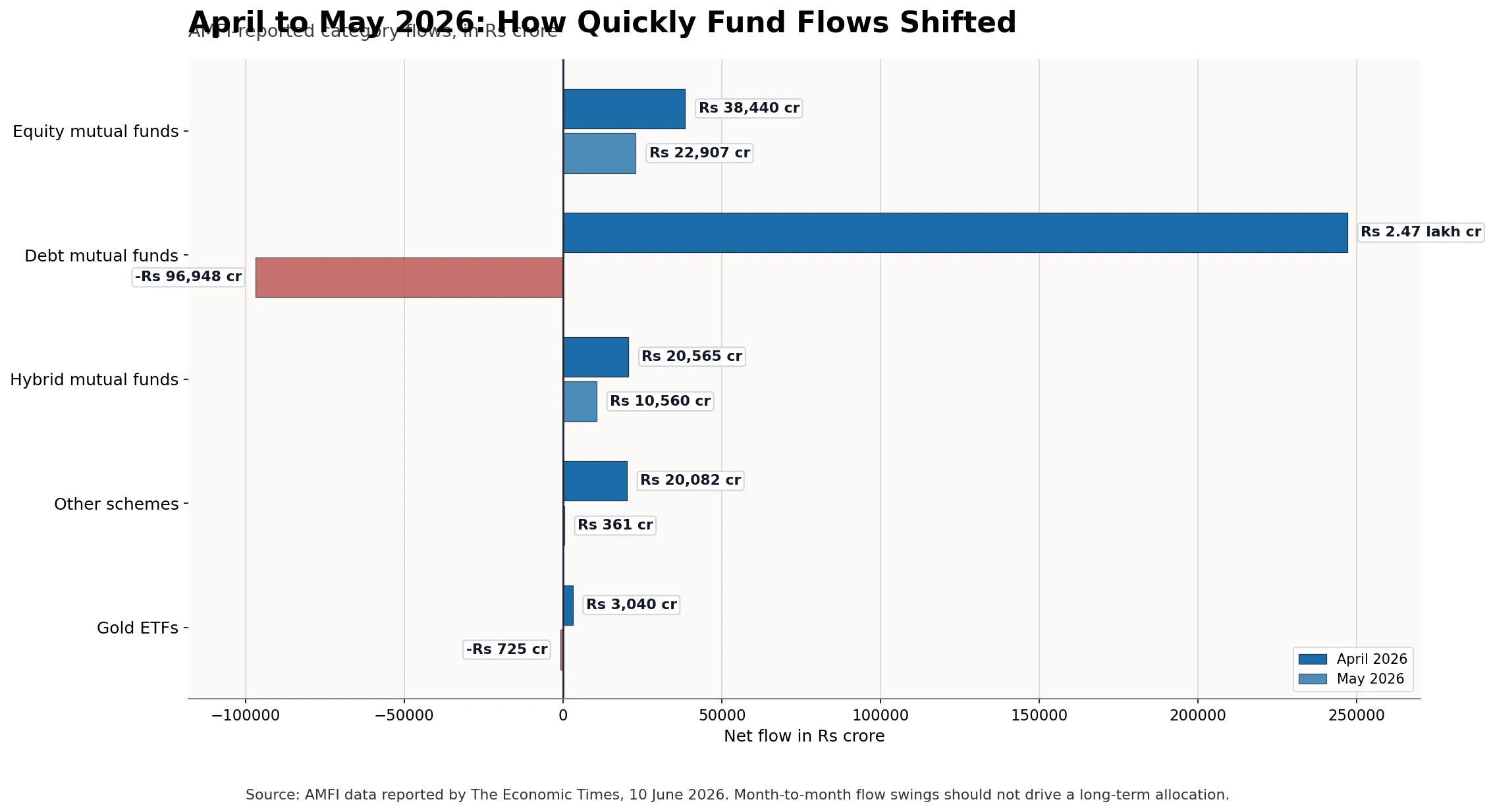

One Month Can Look Very Different From the Previous Month

The same AMFI-reported data showed how quickly category flows can shift from April to May 2026:

| Category | April 2026 | May 2026 |

|---|---|---|

| Equity mutual funds | ₹38,440 crore inflow | ₹22,907 crore inflow |

| Debt mutual funds | ₹2.47 lakh crore inflow | ₹96,948 crore outflow |

| Hybrid mutual funds | ₹20,565 crore inflow | ₹10,560 crore inflow |

| Other schemes including passive funds | ₹20,082 crore inflow | ₹361 crore inflow |

| Gold ETFs | ₹3,040 crore inflow | ₹725 crore outflow |

The lesson for a first portfolio is practical: allocation should come from goals, time horizon and risk capacity, not from one month's flow chart.

A Simple Order for a First Portfolio

Aditi did not need a complicated model. She needed an order of operations:

- keep near-term expenses and emergency money accessible;

- identify goals due within the next few years;

- use stability-oriented products only after understanding their risks and liquidity;

- use equity only for money that can tolerate volatility and time;

- add gold only if it has a defined diversification role; and

- review the buckets periodically instead of reacting to every headline.

The image shows the same idea: the portfolio is not one large pile. It is a set of jobs, each with its own time horizon and risk.

Common Mistakes

- Starting with equity before building accessible emergency money.

- Calling debt “risk-free” without checking credit, duration and liquidity.

- Buying gold because of fear without writing its role in the portfolio.

- Treating liquid funds as identical to bank cash.

- Copying someone else's asset allocation.

- Chasing one-month inflows or recent returns.

- Owning too many products without knowing which goal they serve.

- Ignoring taxation, exit load, documentation and nomination.

- Forgetting that diversification reduces some risks but does not remove market risk.

Investor Checklist

Before making the first portfolio, write down:

- how much money must remain accessible;

- which goals are within three years;

- which goals are genuinely long term;

- how much temporary loss would cause panic;

- which products fit each bucket;

- expected costs, tax treatment and liquidity conditions;

- whether scheme Risk-o-meter and documents have been reviewed; and

- when the portfolio will be reviewed.

For investment-service information, review Abhipra Services, or visit Abhipra eKYC for account-opening support.

Reviewed by Abhipra Research / Compliance Team.

Source Links

- AMFI Investor Corner

- AMFI scheme risk information

- AMFI Risk-o-meter information

- SEBI Investor website

- AMFI May 2026 mutual fund flow data reported by The Economic Times

Disclaimer

This article is for educational and informational purposes only. It should not be considered investment advice, trading advice, tax advice or insurance advice. Investments in securities market and mutual funds are subject to market risks. Asset allocation depends on goals, risk profile, liquidity needs, time horizon and tax situation. Past performance and fund-flow data are not indicators of future returns. Please read all related documents carefully and consult a qualified adviser before making any financial decision.