The Silent Tax on Idle Money: How Inflation Shrinks Your Savings

Idle money feels safe because the number in the bank account does not move down every morning.

But a household does not spend numbers. It spends purchasing power. If groceries, rent, school fees, medical bills and fuel keep moving up, the same Rs 1 lakh quietly buys less each year.

That is why inflation can be called a silent tax on money that is kept idle for too long. It does not send a notice. It simply reduces what your money can do.

The Small Leak Nobody Notices

Imagine a family that keeps Rs 1 lakh untouched for a future goal. At first, it feels disciplined. The money is visible, stable and available.

The problem appears later.

If prices rise by 6% a year, that Rs 1 lakh will still look like Rs 1 lakh after 10 years if it earns nothing. But in purchasing-power terms, it will buy only about Rs 55,839 worth of today's goods and services.

The account balance stayed the same. The usefulness of the balance did not.

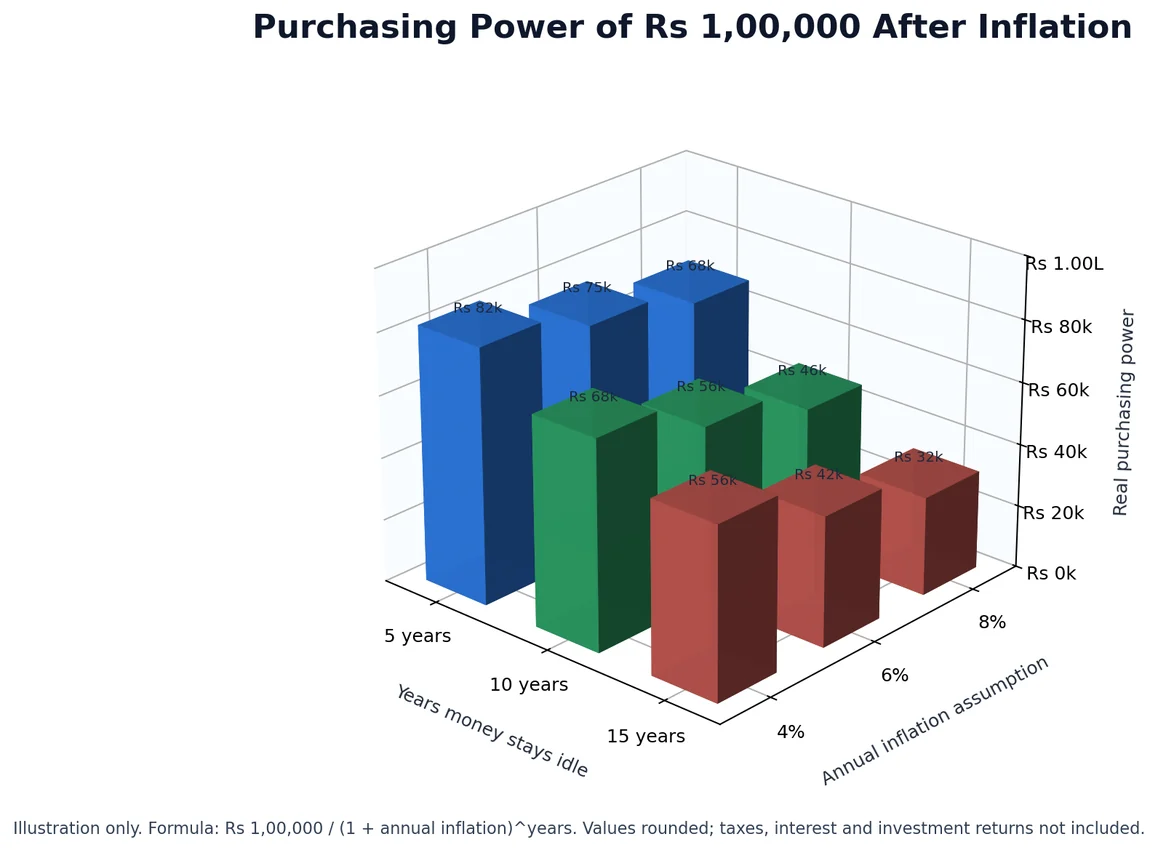

The Chart: What Inflation Does To Rs 1 Lakh

The chart uses a simple purchasing-power formula:

Future purchasing power = Rs 1,00,000 / (1 + annual inflation rate) ^ number of years

It is an illustration, not a forecast or product recommendation. No interest, tax, return, fee or reinvestment has been assumed.

If Rs 1 lakh stays idle:

- At 4% annual inflation, purchasing power falls to about Rs 82,193 after 5 years, Rs 67,556 after 10 years and Rs 55,527 after 15 years.

- At 6% annual inflation, purchasing power falls to about Rs 74,726 after 5 years, Rs 55,839 after 10 years and Rs 41,727 after 15 years.

- At 8% annual inflation, purchasing power falls to about Rs 68,058 after 5 years, Rs 46,319 after 10 years and about Rs 31,520 after 15 years.

This is why inflation matters even when markets are not being discussed. The question is not only "Did my money grow?" It is also "Did my money grow faster than my cost of living?"

Nominal Return Is Not The Same As Real Return

Nominal return is the visible return. Real return is what remains after inflation.

For example, if money earns 5% and inflation is 6%, the investor may feel that the balance increased. But the purchasing power still went backward by about 1% before considering tax and costs.

This is the mistake many households make with long-term idle cash. They look at safety only as protection from market fluctuation. They do not look at safety as protection from purchasing-power loss.

Both risks matter.

Idle Cash Is Useful. Too Much Idle Cash Is Costly.

This does not mean every rupee should be invested aggressively.

Cash and savings balances have a proper role:

- emergency fund;

- near-term expenses;

- business cash flow;

- medical reserves;

- school fees due soon;

- planned purchases within a short horizon; and

- money waiting for a clearly documented allocation decision.

The problem begins when long-term money is kept idle only because the decision feels uncomfortable. In that case, inflation does not wait politely. It keeps working in the background.

A Practical Way To Separate Money

A simple household framework can help:

- Keep short-term money liquid and accessible.

- Protect important medium-term goals with suitable, lower-volatility options.

- Grow long-term money through diversified investments matched to risk appetite, goal date and tax situation.

- Review the plan at fixed intervals, not every time a headline becomes noisy.

This framing is more useful than asking whether cash is good or bad. Cash is a tool. The wrong use of a good tool can still damage the outcome.

How To Think Before Moving Idle Money

Before investing money that has been idle, ask:

- What is this money for?

- When will it be needed?

- How much fall in value can the household tolerate?

- Is the emergency fund already separate?

- Are KYC, nomination and account access details complete?

- What costs, taxes, lock-ins or exit conditions apply?

- Is the decision based on a plan or on recent performance?

The RBI Financial Education initiative highlights awareness of financial products, good financial practices, digital use and consumer protection. The SEBI Investor website provides investor education and support resources. The AMFI Investor Corner explains mutual fund concepts, risks, KYC and investor resources, while noting that mutual funds are not deposits and returns cannot be guaranteed.

For inflation and macroeconomic context, investors can refer to the official Ministry of Statistics and Programme Implementation website, which publishes India's official statistics and data releases including consumer-price information.

The Real Enemy Is Delay Without A Plan

Inflation does not mean investors should rush into unsuitable products. It means long-term money needs a job description.

Some money must remain liquid. Some money must remain stable. Some money must be given a chance to grow.

The investor's work is to decide which rupee belongs in which bucket.

If that decision is delayed for years, inflation makes the decision anyway. It quietly converts a large-looking balance into a smaller lifestyle.

Where Abhipra Can Help

Investors who want help with account opening, demat, mutual fund access, investment services or investor support can review Abhipra Services or complete the Abhipra eKYC journey.

A useful first conversation is not "Which product should I use first?" It is "Which goal is this money for, how soon is it needed, and what risk can I actually stay with?"

Reviewed by Abhipra Research / Compliance Team.

Source Links

- RBI Financial Education

- Ministry of Statistics and Programme Implementation

- SEBI Investor website

- AMFI Investor Corner

- Abhipra Services

Disclaimer

This article is for educational and informational purposes only. It should not be considered investment advice, trading advice, tax advice or insurance advice. Investments in securities market are subject to market risks. Please read all related documents carefully before investing. Past performance is not indicative of future returns. The chart uses simplified inflation assumptions only and does not represent any product return, guarantee or recommendation. Please consult a qualified financial advisor, tax advisor or insurance advisor before making any financial decision.