How to Choose a Pension Fund Manager in NPS Without Chasing Last Year's Winner

Choosing a pension fund manager in NPS should feel like selecting a long-term retirement partner, not picking the top name from last year's return table.

NPS gives useful flexibility. PFRDA says subscribers can choose the Pension Fund and asset allocation recorded with the Central Recordkeeping Agency. NPS Trust also publishes pension fund performance and scheme-level information. The practical challenge is using this information calmly.

Start With The Role Of The Pension Fund

A pension fund manager invests NPS contributions according to the selected scheme, asset class and regulatory investment guidelines. Under the common NPS structure, the main choices are not just "which fund", but also:

- The pension fund.

- The asset class mix.

- Active Choice or Auto Choice.

- Tier I or Tier II usage.

- Whether the choice still fits the investor's age, risk comfort and retirement horizon.

PFRDA's All Citizen Model page says subscribers can select any one PFRDA-registered pension fund, and NPS Trust states that ten pension funds are registered with PFRDA. NPS Trust also says subscribers can select more than one pension fund for different asset classes under eligible models.

The Two Changes Investors Often Confuse

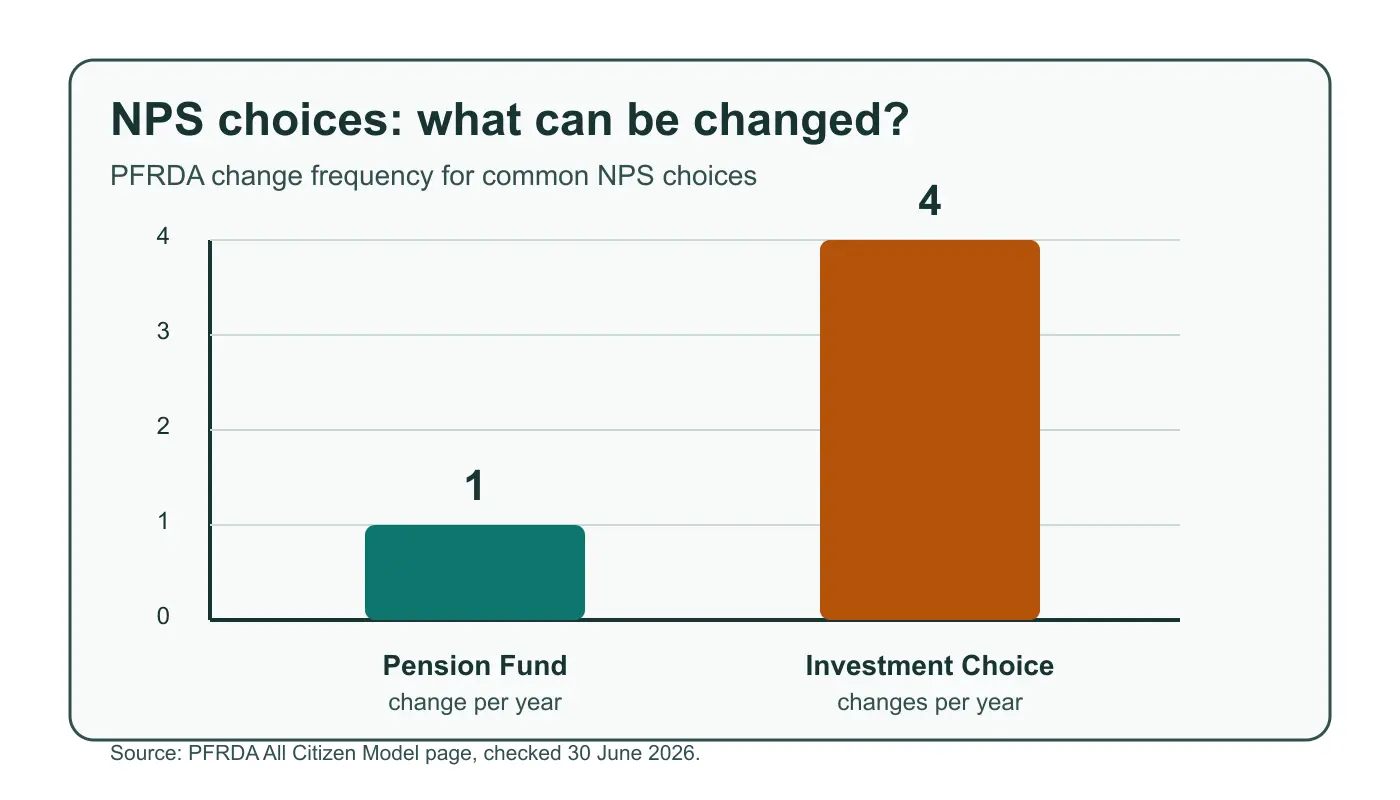

Pension fund change and asset-allocation change are separate decisions. PFRDA states that a subscriber can change the pension fund once in a year, while the asset allocation or investment choice can be changed four times in a year.

The chart means:

- Pension Fund change: once in a year.

- Investment choice or asset allocation change: four times in a year.

- These choices should not be used for frequent return chasing.

This matters because poor asset allocation can hurt a good pension fund choice. For example, PFRDA states that under Active Choice, Equity may go up to 75%, while Corporate Bonds and Government Securities may each go up to 100%, subject to the applicable model and rules. Under Auto Choice, the equity allocation follows a lifecycle design.

| Choice area | Official rule or disclosure | Practical reading |

|---|---|---|

| Pension Fund | PFRDA says subscribers can select any one PFRDA-registered pension fund; NPS Trust lists ten registered pension funds. | Use a shortlist, not a one-year winner list. |

| Performance review | NPS Trust publishes 1-year, 3-year, 5-year, 10-year, since-inception and custom return views. | Check consistency across periods and asset classes. |

| Market risk | NPS Trust states NPS does not offer fixed returns and returns are market-linked. | Do not treat historical returns as a promise. |

| Switching | Pension fund can be changed once in a year; asset allocation or investment choice can be changed four times in a year. | Review periodically, but avoid tactical over-switching. |

A Better Selection Checklist

Use the NPS Trust returns page as a starting point, then ask better questions:

- Has the pension fund shown reasonable consistency across 3-year, 5-year and 10-year views, where available?

- Is performance acceptable across the relevant asset class, not only in one category?

- Does the fund's result look strong because of the market cycle, or because it handled different periods steadily?

- Is the investor's own allocation too aggressive or too conservative for retirement?

- Will a change create a habit of chasing recent winners?

NPS Trust's return page carried returns as on 29 June 2026 when checked. It also states that past performance of schemes or pension funds is not indicative of future performance, and that NPS Trust does not guarantee or assure returns.

The checklist visual can be read as a simple sequence:

- Confirm the investor's retirement horizon.

- Check asset allocation first.

- Compare pension fund performance across longer periods.

- Read the risk and no-guarantee disclaimer.

- Change only when the reason is stronger than short-term ranking.

Charges Matter, But They Are Not The Whole Decision

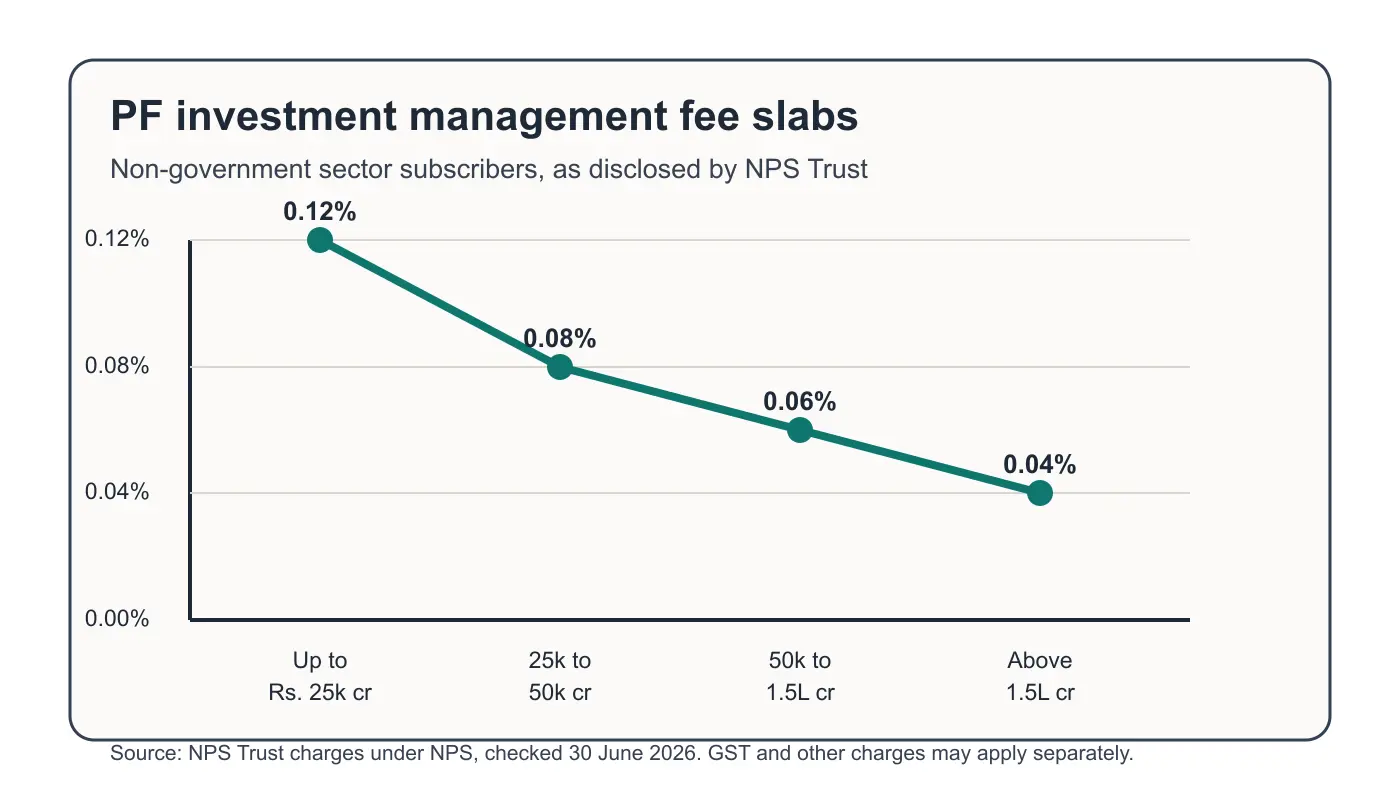

NPS is designed as a low-cost retirement system. NPS Trust's charges page lists pension fund investment management fee slabs. For non-government sector subscribers, the disclosed slabs are 0.12%, 0.08%, 0.06% and 0.04% as the relevant AUM slab rises. Government sector slabs are different.

The non-government sector pension fund investment management fee slabs shown in the chart are:

- Up to Rs. 25,000 crore AUM: 0.12%.

- Above Rs. 25,000 crore to Rs. 50,000 crore: 0.08%.

- Above Rs. 50,000 crore to Rs. 1,50,000 crore: 0.06%.

- Above Rs. 1,50,000 crore: 0.04%.

GST, intermediary charges and transaction-related charges may apply separately. Cost should be understood, but a pension fund should not be selected only because a single displayed number looks attractive.

Common Mistakes To Avoid

- Picking the top one-year return without checking longer periods.

- Comparing an equity-heavy choice with a conservative allocation and calling one "better".

- Forgetting that NPS returns are market-linked.

- Switching because of short-term market noise.

- Ignoring age, income stability, retirement horizon and liquidity needs.

FAQs

How many pension funds are registered under NPS?

NPS Trust states that ten pension funds are registered with PFRDA.

Can I change my NPS pension fund manager?

Yes. PFRDA states that a subscriber can change the pension fund once in a year.

Should I choose the pension fund with the highest one-year return?

Not by itself. One-year return can be influenced by market conditions. Review longer periods, asset class performance, consistency, risk and your own allocation.

Does NPS give a fixed return?

No. NPS Trust states that NPS does not offer fixed returns and returns are market-linked.

Conclusion

The sensible way to choose an NPS pension fund manager is to start with your retirement goal, then check asset allocation, long-period performance, risk, costs and switching rules.

For Abhipra service information, read Abhipra NPS & Pension. To start online, use the NPS account opening link. To set recurring contributions, use the NPS SIP setup link.

Reviewed by Abhipra Research / Compliance Team.

Source Links

- PFRDA All Citizen Model

- NPS Trust: PFs under NPS

- NPS Trust: Returns under NPS

- NPS Trust: Charges under NPS

- Abhipra NPS & Pension

Disclaimer

This article is for educational and informational purposes only. It is not investment, tax, legal or retirement planning advice. NPS is market-linked and subject to PFRDA rules, investment risk, tax provisions, exit conditions and regulatory changes. Investors should evaluate suitability, liquidity needs, tax position, risk appetite and investment horizon before making any decision.