Expense Ratio and NAV Explained: Two Numbers Every Mutual Fund Investor Should Read

A mutual fund fact sheet can look simple until two terms start confusing the decision: NAV and expense ratio. One tells you the per-unit value of the scheme. The other tells you the annual cost charged to run the scheme. Neither number should be read in isolation.

For Indian investors comparing mutual funds, understanding these two terms can prevent two common mistakes: assuming a lower NAV is automatically cheaper, and ignoring the cost that quietly affects long-term outcomes.

NAV Is Not The Price Tag Of A Cheap Fund

NAV, or Net Asset Value, is the per-unit value of a mutual fund scheme. In simple terms, it reflects the value of the scheme's assets after liabilities, divided by the number of outstanding units.

A fund with an NAV of Rs 20 is not automatically cheaper than a fund with an NAV of Rs 200. The NAV depends on when the scheme started, how its portfolio has moved, distributions, splits and unit history. What matters more is what the scheme owns, whether it matches your goal, and whether the risk is suitable for you.

Expense Ratio Is The Ongoing Cost Of The Scheme

The expense ratio, often called Total Expense Ratio or TER, is the annual cost charged to the scheme for fund management, administration, operations and permitted expenses. It is not usually paid separately by the investor; it is adjusted in the scheme's NAV.

That means a scheme's reported NAV and return experience already reflect expenses. A lower cost may help over long periods, but cost alone should not become the only reason to select a fund. Investors should also check category, risk level, investment style, portfolio quality, consistency, fund mandate and suitability.

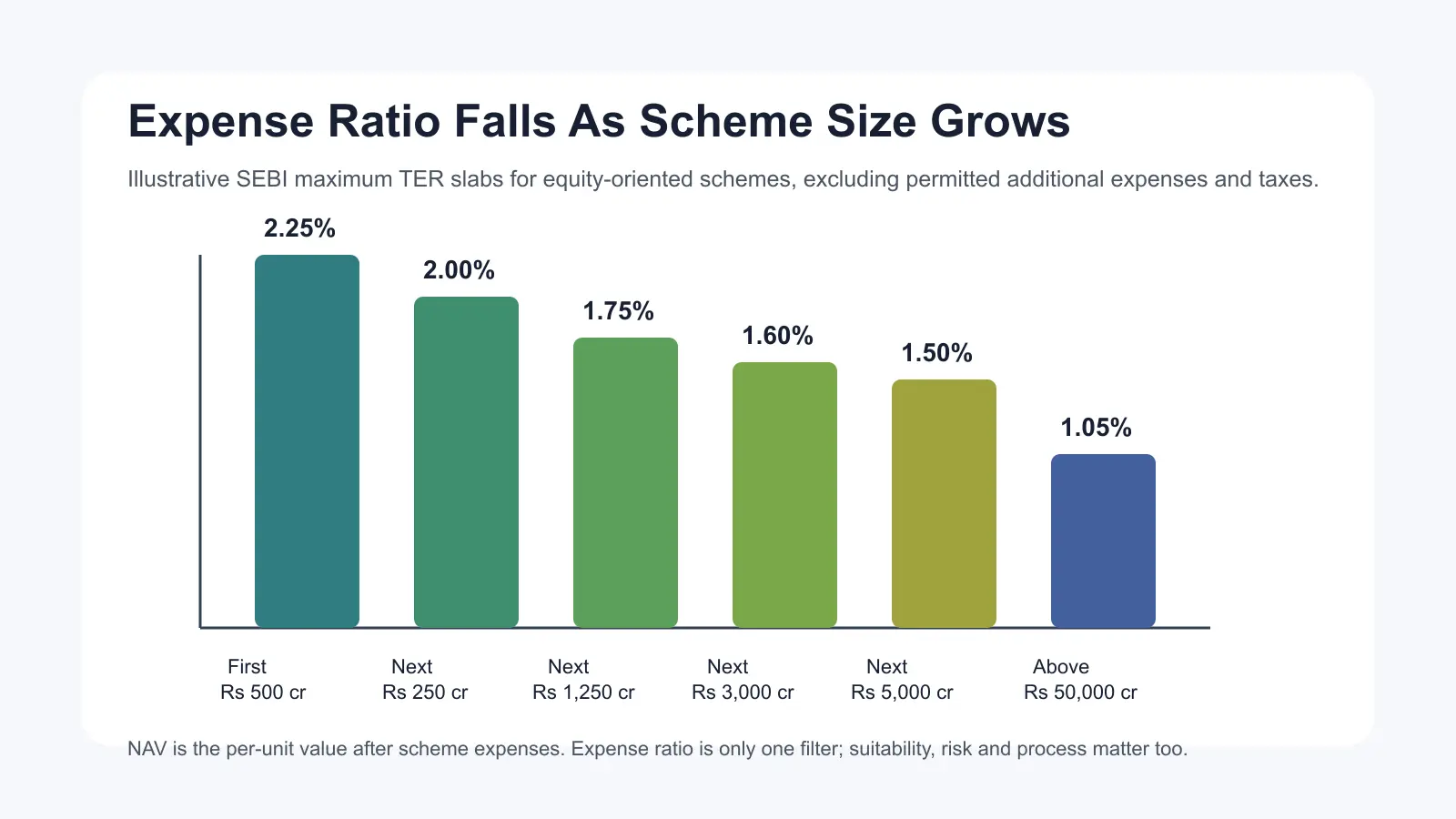

SEBI's TER Slab Framework

SEBI prescribes maximum TER limits through a slab framework. For equity-oriented schemes, the broad maximum TER decreases as scheme assets increase. This prevents larger schemes from charging the same maximum percentage as much smaller schemes, subject to applicable regulations, additional permitted expenses and taxes.

| Assets slab | Maximum TER for equity-oriented schemes | Investor takeaway |

|---|---|---|

| First Rs 500 crore | 2.25% | Smaller schemes may have higher permitted cost limits. |

| Next Rs 250 crore | 2.00% | Cost limit starts reducing as scheme size grows. |

| Next Rs 1,250 crore | 1.75% | Scale can lower the maximum permitted expense percentage. |

| Next Rs 3,000 crore | 1.60% | Compare actual TER in the scheme factsheet, not only the maximum. |

| Next Rs 5,000 crore | 1.50% | A large fund can still be unsuitable if the category or risk is wrong for your goal. |

| Above Rs 50,000 crore | 1.05% | Cost matters, but it is only one part of fund selection. |

How To Read Both Numbers Together

Use NAV and expense ratio as filters, not as shortcuts.

- If two funds follow a similar mandate, compare their TER, risk, portfolio and consistency.

- If a fund has a low NAV, check whether it is genuinely suitable or simply newer.

- If a fund has a low expense ratio, still check category risk, concentration and investment process.

- If a fund has high recent returns, check whether the return came with higher volatility or sector concentration.

The desk review represents the practical sequence: read the scheme category first, then check riskometer, portfolio, expense ratio, NAV history and whether the investment fits the goal. The data table above provides the numerical context; the investment decision still needs suitability review.

Common Mistakes

Do not buy a mutual fund only because its NAV is low. A low NAV does not mean the fund is undervalued like a stock.

Do not choose a fund only because the expense ratio is low. Low cost can help, but the wrong category or excessive risk can still damage the plan.

Do not compare expense ratios across unrelated categories. An overnight fund, index fund, hybrid fund and small-cap fund can have very different mandates, risks and cost structures.

Investor Checklist

- Read the scheme category and investment objective.

- Check the actual TER in the latest factsheet.

- Understand whether you are looking at a direct plan or regular plan.

- Treat NAV as a unit value, not a cheap-or-expensive signal.

- Compare funds within the same category and similar mandate.

- Review risk, liquidity, tax impact and investment horizon before investing.

For mutual fund selection, SIP planning or portfolio review support, connect with Abhipra's Wealth Planning Desk through Abhipra's contact page.

Source Links

- SEBI: Master Circular for Mutual Funds

- SEBI: Mutual Fund Regulations

- AMFI: Mutual fund investor and NAV information

Reviewed by Abhipra Research / Compliance Team.

Disclaimer

This article is for educational and informational purposes only. It is not investment advice, tax advice, a mutual fund recommendation or a promise of returns. Mutual fund investments are subject to market risks. Investors should read all scheme-related documents carefully and evaluate suitability, risk appetite, investment horizon, liquidity needs and tax position before making investment decisions.