EPF Plus NPS: How Salaried Professionals Can Build a Second Retirement Corpus

A private-sector salary often already has one retirement habit built in: provident fund saving. The question is whether that is enough for a retirement that may last 25 to 30 years after regular income stops.

NPS can help salaried professionals build a second retirement corpus because it is portable across jobs, market-linked, regulated by PFRDA, and designed specifically for retirement planning rather than short-term withdrawal.

Start With The Retirement Stack, Not A Product Race

EPF and NPS do not need to compete for the same role.

- EPF can remain the salary-linked retirement base for eligible employees.

- NPS can become the second, voluntary retirement layer where the subscriber chooses a pension fund and asset allocation within PFRDA rules.

- Emergency money, health cover, and short-term goals should still stay outside NPS because NPS Tier I is meant for retirement and has withdrawal conditions.

This separation matters. Retirement planning becomes easier when each rupee has a job: near-term liquidity, medium-term goals, and long-term pension security.

What Makes NPS Useful For Salaried Professionals

PFRDA describes NPS as a regulated, low-cost, flexible, portable, market-linked retirement system. For salaried professionals, four features are especially practical:

- Portability across jobs: PFRDA states that NPS accounts are portable across employment types and locations. A job change does not require starting retirement planning from zero.

- Employee and employer contribution routes: Under the Corporate Sector Model, contributions can be made by the employer, employee, or both, depending on the employer's compensation policy.

- Tax provisions to evaluate: PFRDA lists employee deduction provisions under Section 80CCD(1), the additional Rs 50,000 deduction under Section 80CCD(1B), and employer contribution deduction under Section 80CCD(2), with old-regime and new-regime limits differing for employees.

- Choice of investment approach: Subscribers can select pension funds and choose between Active Choice and Auto Choice. Active Choice allows allocation across equity, corporate bonds, and government securities within limits; Auto Choice reduces equity exposure with age.

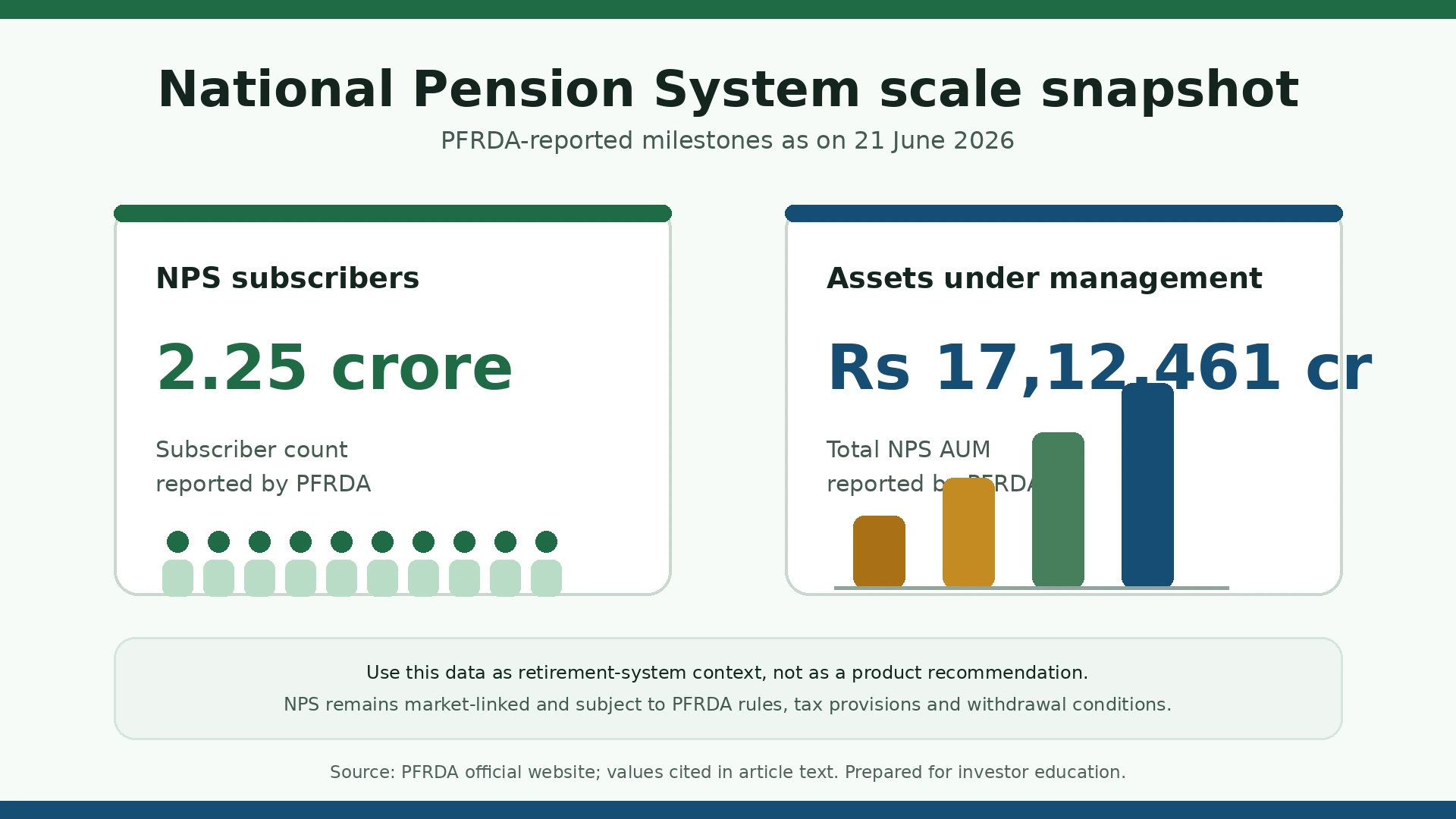

The Scale Behind The System

PFRDA's official website reported these NPS milestones as on 21 June 2026: 2.25 crore NPS subscribers and total NPS assets under management of Rs 17,12,461 crore.

The chart highlights a simple point in selectable text: NPS is no longer a niche retirement account. It is a regulated pension system with large participation and assets, but it remains market-linked. Scale is not a guarantee of return, and subscribers still need suitable asset allocation, contribution discipline, and exit planning.

How To Use NPS Without Overstretching Cash Flow

For a salaried investor, the practical question is not "How much can I put in NPS?" It is "What monthly amount can I continue without disturbing liquidity?"

A sensible sequence can be:

- Keep emergency money outside retirement products.

- Review existing EPF, employer retirement benefits, insurance, loans, and family responsibilities.

- Choose an NPS monthly contribution that can continue through salary changes.

- Review asset allocation once a year instead of reacting to short-term market returns.

- Recheck tax treatment every year because personal tax regime, employer contribution structure, and law can change.

Employees whose companies offer Corporate NPS should ask payroll or HR how employer contribution is structured. Employees without Corporate NPS can still evaluate individual NPS through a Point of Presence or online route, subject to eligibility and KYC.

What To Be Careful About

NPS is useful because it is retirement-focused. That is also why it should not be treated like a regular savings account.

- Tier I is the primary retirement account and has withdrawal and exit rules under PFRDA regulations.

- Tier II is optional, available only with an active Tier I account, and PFRDA states it does not carry the same tax benefits as Tier I.

- Market-linked returns can move up or down.

- Tax benefit suitability depends on salary structure, employer policy, tax regime, and individual tax profile.

- Annuity, lump sum, systematic lump sum withdrawal, and other exit options should be understood before retirement, not at the last minute.

When A Second Corpus Makes Sense

NPS may be worth evaluating if:

- your retirement planning currently depends only on EPF and expected future salary growth;

- you want a dedicated pension account that stays with you across jobs;

- your employer provides Corporate NPS or is open to adding it as a retirement benefit;

- you can invest with a long horizon and accept market-linked risk;

- you want to separate retirement saving from short-term goal investing.

It may not be the right first step if you do not have emergency funds, have high-cost debt, need high liquidity, or are not comfortable with retirement-linked withdrawal rules.

Abhipra NPS Support

You can read more about Abhipra's NPS services on the Abhipra NPS & Pension page. Eligible investors can also open an NPS account online or set up an NPS SIP contribution. For help, write to the Abhipra NPS Desk at nps@abhipra.com.

Source Links And Disclaimer

Sources checked on 1 July 2026:

- PFRDA official website for NPS milestones

- PFRDA NPS Corporate Sector Model

- PFRDA NPS All Citizen Model

This article is for educational and informational purposes only. It should not be treated as investment, tax, legal, or retirement planning advice. NPS is a market-linked retirement product and is subject to applicable PFRDA rules, investment risks, tax provisions, and withdrawal conditions. Investors should carefully evaluate their financial goals, risk appetite, investment horizon, liquidity needs, and tax situation before making any decision.