Why Starting Pension Planning at Childhood Changes the Entire Equation

Most parents save for school, college or a first home. Retirement usually enters the conversation much later, after the child starts earning. NPS Vatsalya changes that question: what if the pension habit starts while the child is still a minor, with the parent or guardian building the discipline first?

The Biggest Advantage Is Time, Not A Magic Return

NPS Vatsalya is not a guaranteed-return product. It is a market-linked retirement account under the NPS framework, and its value will depend on contributions, asset allocation, charges, market returns and future rules. Its real planning advantage is simpler: the investment clock can start many years before the child earns a salary.

That longer runway can change family behaviour in three ways:

- Retirement is treated as a separate goal, not an afterthought.

- The child grows up seeing retirement contributions as a normal habit.

- Smaller periodic contributions get more time to work, though returns are never guaranteed.

What Parents Should Verify First

As per the PFRDA NPS Vatsalya page, the account is meant for minor subscribers and is operated through a guardian until the child reaches adulthood. The official page should be checked before account opening because contribution, withdrawal and transition rules can change.

Key checks for parents:

- The child, guardian and KYC details must match the latest CRA/PFRDA requirements.

- Contributions should be made only from money that can remain locked for a long retirement purpose.

- The account is not a substitute for emergency funds or education savings.

- At adulthood, the child should understand the account and complete the required transition formalities.

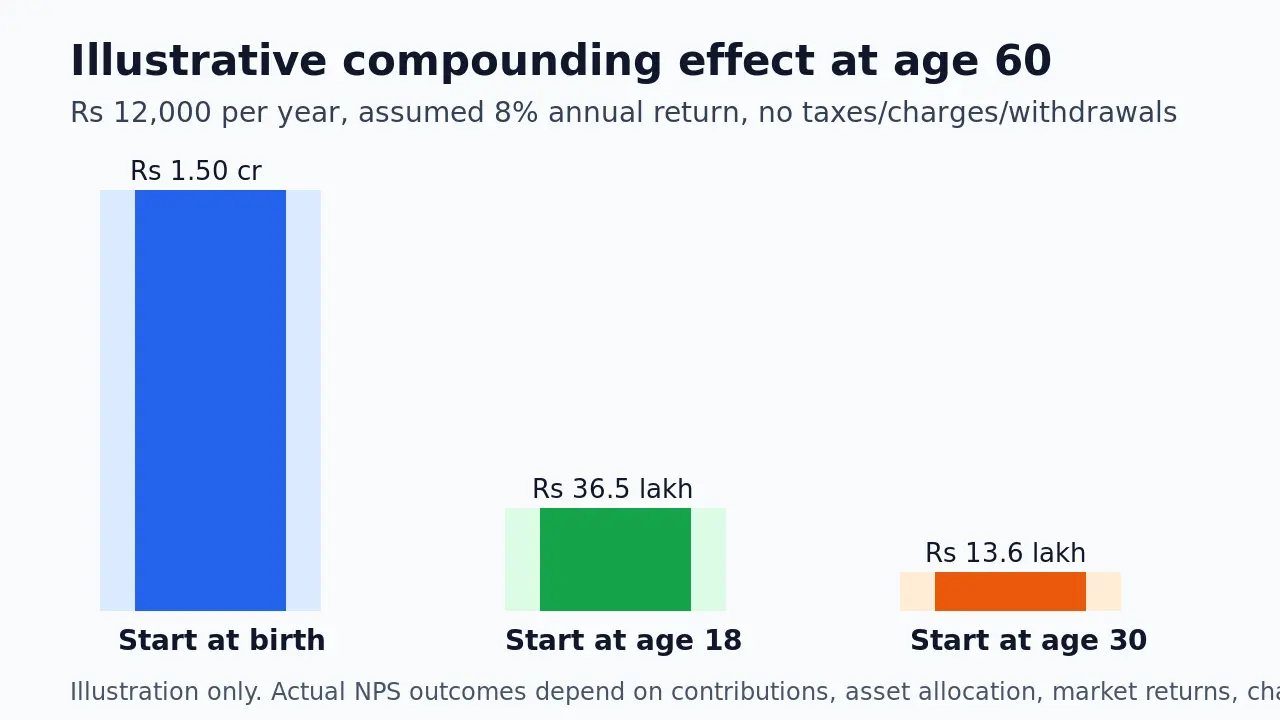

A Simple Illustration: Starting Earlier Changes The Scale

The chart below uses a deliberately simple example: Rs 12,000 contributed at the end of every year until age 60, with an assumed 8% annual return. It is only an illustration to explain compounding. It is not an NPS return forecast, guarantee or recommendation.

The chart shows the same annual contribution under three starting ages:

- Starting at birth for 60 years: approximately Rs 1.50 crore at age 60.

- Starting at age 18 for 42 years: approximately Rs 36.5 lakh at age 60.

- Starting at age 30 for 30 years: approximately Rs 13.6 lakh at age 60.

The point is not that the assumed return will happen. The point is that the earlier start gets more compounding periods. If actual returns are lower, higher or volatile, outcomes will change.

Where NPS Vatsalya Fits In A Family Plan

NPS Vatsalya can sit beside other child-focused goals, but it should not be confused with them. College funding, health protection, term insurance for parents and an emergency fund may need more flexibility than a retirement account provides.

A practical approach is:

- Use liquid savings and suitable goal-based investments for near-term education expenses.

- Use insurance for protection risks.

- Use NPS Vatsalya only for the portion parents are comfortable earmarking for the child's long-term retirement security.

What The Child Should Learn At 18

The account becomes most meaningful when the child understands it. At 18, the discussion should move from "parents saved for me" to "I am responsible for my retirement account."

Good questions to discuss:

- What asset allocation is suitable for my age and risk appetite?

- How much can I contribute after I start earning?

- How do NPS withdrawal and annuity rules affect long-term liquidity?

- How does this account work alongside EPF, PPF, mutual funds or other savings?

Practical Next Steps

Parents who want to understand the NPS framework can read Abhipra's NPS & Pension service page. For account-opening, use the latest official onboarding flow and verify the current rules before proceeding. You may also contact the Abhipra NPS Desk at nps@abhipra.com for assistance.

FAQs

Is NPS Vatsalya suitable for every child?

Not automatically. It may suit families that can set aside money for a very long retirement purpose. It may not suit families that need flexible access for education, medical needs or short-term goals.

Does the chart guarantee the child's retirement corpus?

No. The chart uses an assumed return only to explain the effect of starting age. Actual NPS outcomes depend on contributions, asset allocation, market returns, charges, withdrawal choices and applicable rules.

Should parents stop education savings if they open NPS Vatsalya?

No. Education planning and retirement planning are different goals. NPS Vatsalya should complement, not replace, goal-based education savings.

Source Links And Disclaimer

- PFRDA NPS Vatsalya page

- NPS Trust

- PIB release on PFRDA pension outreach for MSMEs

- Abhipra NPS & Pension services

This article is for educational and informational purposes only. It should not be treated as investment, tax, legal or retirement planning advice. NPS is a market-linked retirement product and is subject to applicable PFRDA rules, investment risks, tax provisions and withdrawal conditions. Investors should evaluate their financial goals, risk appetite, investment horizon and tax situation before making any decision.