What Happens to Your NPS Corpus at Retirement?

Retirement planning does not end when the National Pension System (NPS) account has grown into a corpus. The real decision starts at exit: how much can be withdrawn as a lump sum, how much has to be used for annuity, and how the money can support regular retirement income.

For many investors, this is the point where NPS becomes different from a normal long-term investment account. NPS is designed to convert part of the accumulated corpus into pension income, not only to provide a one-time payout.

The Two Parts of the NPS Corpus

At normal exit around retirement age, the NPS corpus is broadly divided into:

- A lump-sum component that can be withdrawn, subject to applicable rules.

- An annuity component that is used to buy pension income from an annuity service provider.

This design is important because retirement money has two jobs. One part may help meet immediate needs such as contingency planning, debt closure, medical provisioning or family support. The other part should create income discipline for the years after salary or business income reduces.

Updated Exit Split: Withdrawal Flexibility Has Improved

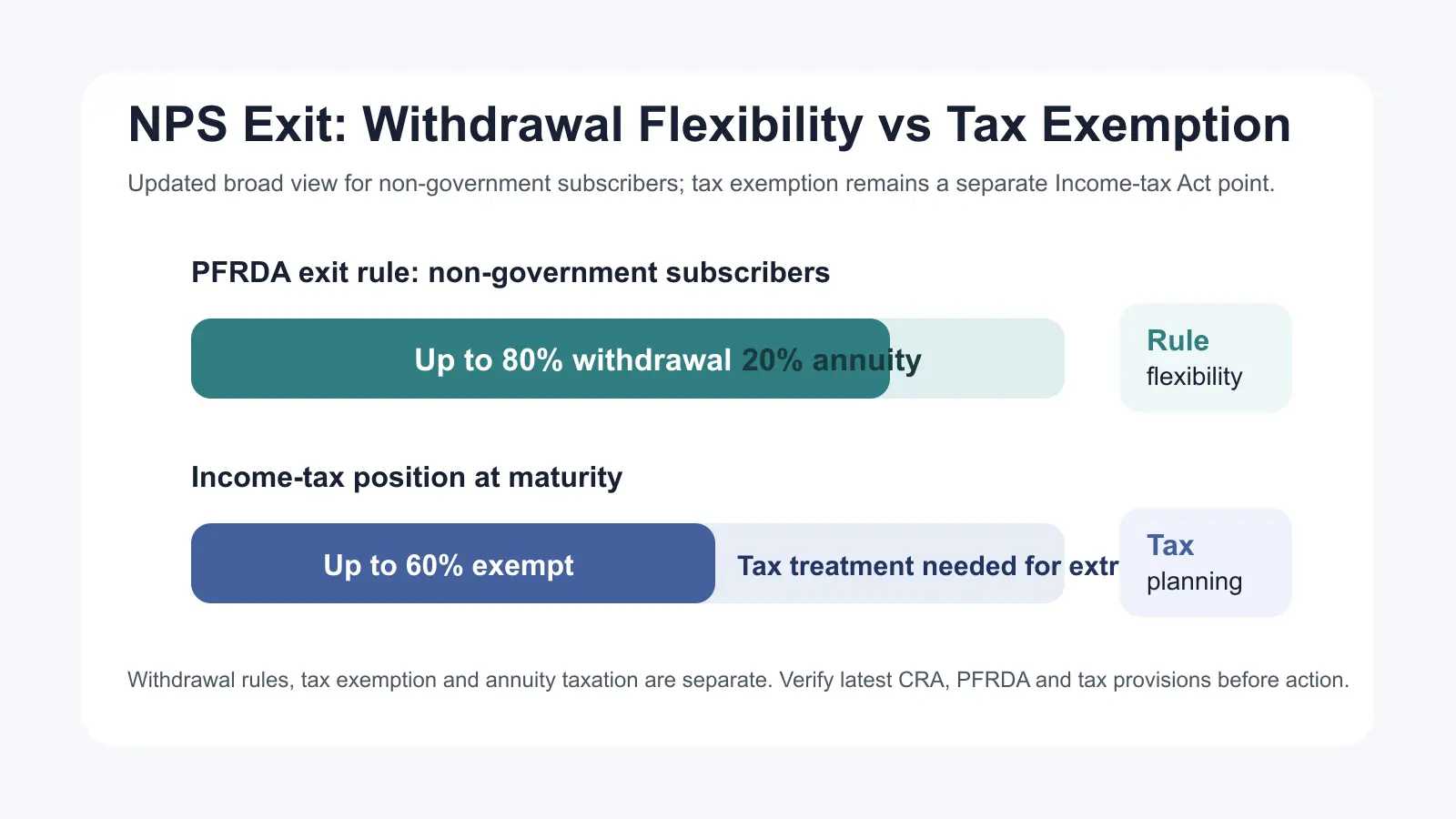

PFRDA's amended exit framework has changed the planning conversation for non-government NPS subscribers. At eligible exit after the required minimum period, the regulation now provides that at least 20% of accumulated pension wealth should be used to buy annuity, and the balance can be taken as lump sum or through a phased/periodic withdrawal arrangement permitted by PFRDA. In practical terms, the withdrawal flexibility can go up to 80%, subject to the latest rules, subscriber category, corpus thresholds and CRA process.

This does not mean every investor should automatically withdraw 80%. It means the exit decision now needs two separate checks: what PFRDA permits as withdrawal, and how the Income-tax Act treats the maturity proceeds.

| Point to check | Current broad position | Investor implication |

|---|---|---|

| Eligible exit for non-government subscribers | At least 20% of accumulated pension wealth is generally used for annuity; the balance may be available for lump-sum or permitted periodic withdrawal. | Withdrawal flexibility can go up to 80%, but the best choice depends on income needs, tax treatment and family protection. |

| Small corpus treatment | The amended regulation provides threshold-based full-withdrawal treatment in specified cases. | Check the current CRA/PFRDA process before filing the exit request. |

| Income-tax exemption at maturity | Section 10(12A) provides exemption for payment from NPS Trust on closure or opt-out up to 60% of the total amount payable. | Do not assume the additional withdrawal flexibility automatically receives the same tax exemption. |

Tax Treatment: 80% Withdrawal Flexibility Is Not The Same As 80% Tax Exemption

The maturity-tax point needs special attention. Under Section 10(12A) of the Income-tax Act, the exemption for payment from the NPS Trust on closure or opting out is linked to 60% of the total amount payable. Therefore, even where PFRDA rules permit higher withdrawal flexibility, investors should separately evaluate the tax treatment of any amount beyond the exempt portion before deciding how much to withdraw.

The annuity portion also needs tax planning. The purchase of annuity is part of the NPS exit design, but pension/annuity income received later is generally considered taxable in the year of receipt according to the investor's applicable tax slab and facts. This is why retirement cash-flow planning should not stop at the withdrawal percentage.

Why the Annuity Decision Matters

The annuity part is not a minor formality. It decides the pension stream that may support monthly expenses after retirement. Investors should compare annuity service providers, annuity options, payout frequency, return-of-purchase-price features and family protection needs before choosing.

An annuity with a higher pension amount may not always be the best fit if it provides weaker family protection. Similarly, a return-of-purchase-price option may appeal to families that want capital protection for nominees, but the regular payout can differ. The right choice depends on household expenses, health cover, spouse dependency and other retirement assets such as EPF, PPF, deposits, mutual funds or rental income.

What Investors Should Do Before Exit

Start exit planning before the retirement date. Do not wait until the last few weeks to understand annuity choices, bank details, nominee records, KYC status and document requirements.

Use this checklist:

- Review your NPS statement and estimate the likely corpus split.

- Decide how much lump-sum liquidity is genuinely required.

- Compare annuity options from empaneled annuity service providers.

- Check whether nominee details, bank details and KYC records are updated.

- Map expected pension income against household monthly expenses.

- Keep tax, medical and emergency liquidity needs separate from routine spending.

Common Mistakes to Avoid

The first mistake is seeing the lump-sum amount as free spending money. Retirement can last 20 to 30 years, so even the withdrawable component needs a plan.

The second mistake is selecting annuity purely on the highest first-year payout. Pension income must be assessed with spouse security, nominee benefit, inflation, other assets and liquidity needs.

The third mistake is exiting prematurely without understanding the annuity-heavy structure. NPS is built for retirement, and premature exit may reduce flexibility.

How Abhipra Can Help

Investors who want to understand NPS registration, contribution discipline, SIP setup, exit preparation or annuity planning can connect with Abhipra's NPS Desk.

- Learn more about Abhipra NPS & Pension services.

- Open an NPS account through Abhipra's online NPS account-opening link.

- Set up recurring contributions through Abhipra's online NPS SIP setup link.

- For NPS queries, write to the Abhipra NPS Desk.

Sources

- PFRDA: National Pension System overview

- PFRDA: Regulatory framework and exit regulations

- PFRDA: Exit and Withdrawal Regulations, 2015, last amended on 16 December 2025

- PFRDA: Empaneled annuity service providers

- Income Tax Department: Income-tax Act, 1961 - Section 10(12A) covers NPS maturity/closure exemption up to 60% of the total amount payable.

Disclaimer

This article is for educational and informational purposes only. It should not be treated as investment, tax, legal or retirement planning advice. NPS is a market-linked retirement product and is subject to applicable PFRDA rules, investment risks, tax provisions and withdrawal conditions. Investors should carefully evaluate their financial goals, risk appetite, investment horizon and tax situation before making any decision.