Understanding Annuity in NPS: Why Part of Your Corpus Buys Pension

Most investors notice the NPS corpus first. The pension decision often comes later, when retirement is close and the exit form asks a serious question: how much should remain available as a lump sum, and how much should be used to buy annuity income?

That question matters because NPS is not designed only to create a retirement number on a statement. It is designed to convert part of long-term saving into retirement income.

Annuity Converts A Corpus Into Pension Income

An annuity is a retirement-income arrangement. At NPS exit, the subscriber uses the required annuity portion of the corpus to buy a pension option from an Annuity Service Provider. The exact income depends on the provider, product option, age, annuity rates, spouse or nominee benefit, return-of-purchase-price feature and terms selected at the time of purchase.

This is why annuity should not be treated as a formality. It decides how a part of the accumulated NPS corpus will support regular post-retirement income.

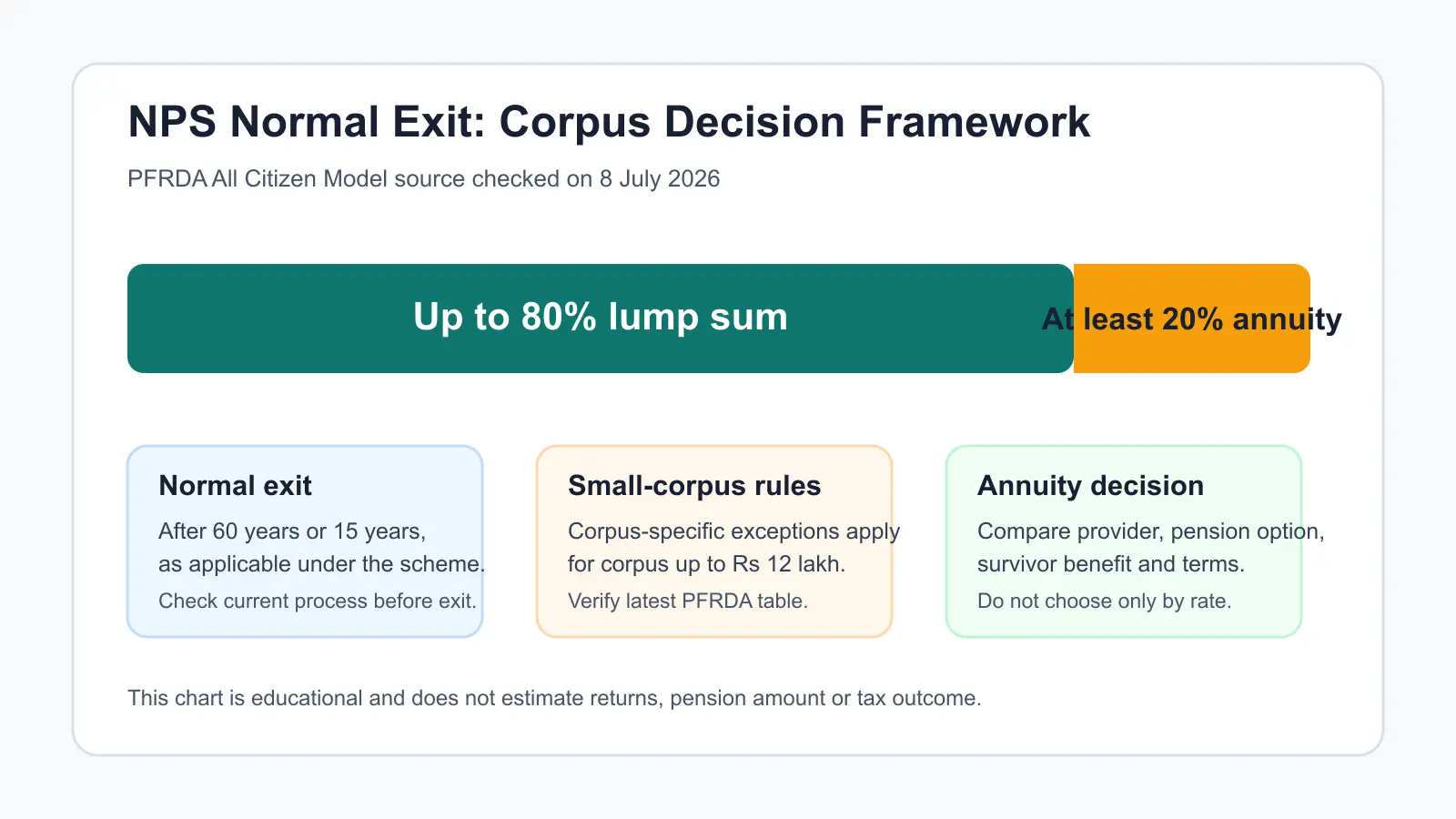

The Latest Normal-Exit Split Is Not The Old 60-40 Rule

PFRDA's All Citizen Model page, checked on July 8, 2026, states that normal exit after 60 years or 15 years, as applicable, allows up to 80% lump sum and requires at least 20% annuity. The same PFRDA table also lists corpus-specific treatment for corpus up to Rs 12 lakh.

In practical terms:

- The lump-sum portion can support liquidity, reinvestment, family needs or planned withdrawals.

- The annuity portion is meant to create pension income.

- Corpus-specific exceptions and permitted payout options should be checked before making an exit decision.

- Premature exit has a different structure and should not be confused with normal retirement exit.

| Decision point | What it means | Action before exit |

|---|---|---|

| Lump sum | Under normal exit, PFRDA states that up to 80% may be available as lump sum, subject to applicable rules. | Plan how much liquidity is needed for medical reserve, household cash flow, debt closure and family goals. |

| Annuity | At least 20% is used to buy annuity under normal exit, unless a specific exception applies. | Compare annuity options, survivor benefit, return-of-purchase-price choice and provider terms. |

| Corpus-specific exception | PFRDA lists special treatment for corpus up to Rs 12 lakh under the current All Citizen Model table. | Check the latest rule table and CRA process before assuming a standard split. |

| Premature exit | Premature exit rules differ from normal exit and may require a larger annuity portion. | Do not use normal-retirement rules for early-exit decisions. |

Why NPS Uses Annuity

Retirement planning has two separate risks. The first is not saving enough. The second is spending the corpus too quickly after retirement.

Annuity addresses the second risk. It turns part of the corpus into periodic income, so the retirement account does not depend only on one-time withdrawals. This is useful for subscribers who want a pension-like cash flow after salary or business income reduces.

The trade-off is liquidity. Once annuity is purchased, the terms of the selected annuity product apply. That is why the choice should be made after comparing options, not at the last minute.

The desk review shows the practical decision process: confirm exit eligibility, estimate household retirement expenses, decide lump-sum liquidity needs, compare annuity service providers, evaluate spouse or nominee protection, and keep tax and documentation records ready.

Questions To Ask Before Choosing An Annuity Option

Do not choose an annuity only because the first-year payout looks higher. Ask these questions:

- Is the pension payable only for the subscriber's life or also to the spouse after the subscriber's death?

- Does the option return purchase price to the nominee or legal heir?

- Is the pension fixed, increasing or structured differently?

- What are the current annuity rates and terms from different providers?

- How will the selected option fit monthly expenses, medical reserve and other retirement income?

- What documents, bank details and nominee records must be updated before exit?

PFRDA's Annuity Service Provider page also points subscribers to compare annuity rates and terms. That comparison is important because the best option is not always the highest immediate pension. Family protection and liquidity planning matter.

How Abhipra Can Help

Subscribers approaching retirement should review NPS exit rules, annuity options, documents, nomination, bank details and tax implications before submitting an exit request.

Read more about Abhipra's NPS and pension services.

Eligible investors can open an NPS account through Abhipra's online NPS PoP link.

Investors who want contribution discipline can use Abhipra's NPS SIP PoP link.

For NPS queries, write to Abhipra's NPS Desk.

Reviewed by Abhipra NPS / Compliance Team.

Sources And Disclaimer

Sources checked on July 8, 2026: PFRDA All Citizen Model, PFRDA Annuity Service Provider page, Protean myNPS account-opening information, and Abhipra NPS and pension services.

This article is for educational and informational purposes only. It is not investment, tax, legal or retirement-planning advice. NPS is market-linked and subject to applicable PFRDA rules, investment risks, charges, tax provisions, annuity terms, exit rules and operational procedures. Subscribers should verify current rules and consult qualified advisers before making retirement or tax decisions.