NPS Vatsalya: What Happens When the Child Turns 18?

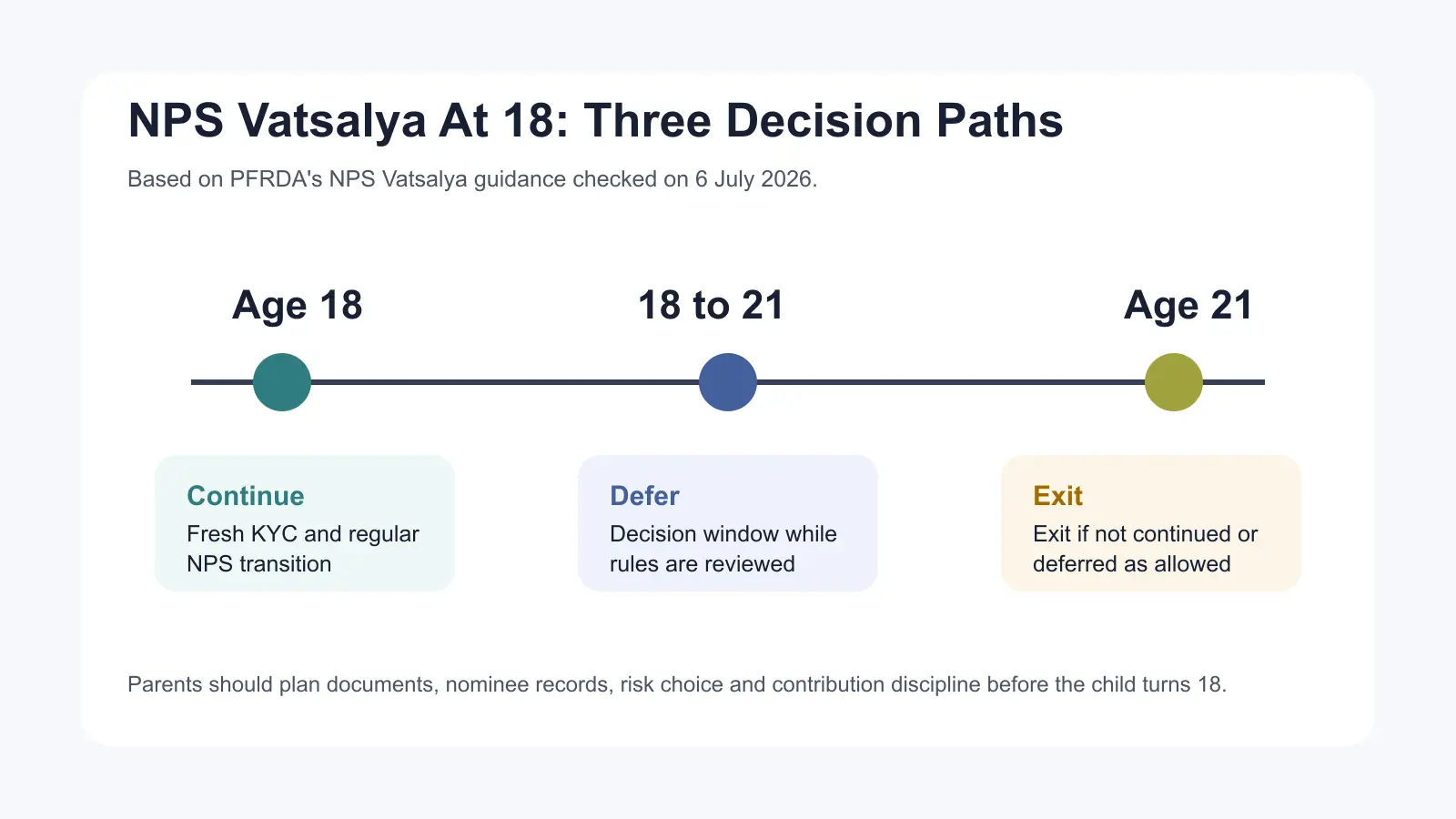

NPS Vatsalya is opened by a parent or guardian for a minor. But the real planning milestone arrives when the child becomes an adult. At 18, the account is no longer only a parent-led pension account. The child, now a major, has to make a decision about continuing, deferring or exiting as permitted by PFRDA rules.

This makes the 18th birthday an administrative and financial planning checkpoint, not just a family milestone.

The Account Does Not Automatically Become A Finished Goal

PFRDA's NPS Vatsalya guidance explains that when the minor subscriber attains 18 years of age, the subscriber can continue under NPS after completing fresh KYC. The transition is important because the child becomes responsible for future retirement-planning decisions.

Parents should therefore prepare before the 18th birthday. The family should know whether the child will continue contributions, defer the decision within the permitted window, or exit according to applicable rules.

The 18 To 21 Decision Window

The official PFRDA guidance provides a practical transition window. On attaining majority, the subscriber can continue the account by completing fresh KYC. The subscriber can also defer the continuation or exit decision up to 21 years of age. If the account is not continued or deferred, exit conditions apply as per the scheme rules.

| Stage | What the family should review | Practical action |

|---|---|---|

| At age 18 | Fresh KYC, contact details, bank details, nominee details and investment preference. | Decide whether to continue under regular NPS after completing required process. |

| Between 18 and 21 | Whether the young adult is ready to take contribution and retirement-planning decisions. | Use the permitted deferment window if the decision needs more time. |

| Exit choice | Exit rules, corpus size, annuity requirement, tax treatment and long-term retirement purpose. | Verify latest CRA and PFRDA process before submitting an exit request. |

Withdrawal Rules Still Need Care

NPS Vatsalya is designed for long-term retirement discipline, not short-term spending. PFRDA's page provides for partial withdrawal for specified reasons and also explains exit treatment depending on corpus size and annuity requirements.

This means parents should avoid presenting NPS Vatsalya as a general-purpose child fund. Education goals, emergency needs and retirement security are different financial goals. NPS Vatsalya can support retirement discipline, but the family should plan separately for near-term liquidity.

The desk review represents the practical checklist before the child turns 18: update KYC readiness, confirm bank and contact details, review nominee information, discuss contribution responsibility, and decide whether the account should continue, defer or exit under current rules.

What Parents Should Discuss With The Child

- Why the account was opened and what retirement planning means.

- How market-linked pension products can move up and down.

- Whether future contributions will come from the child, parent or family.

- What happens if the account is continued into regular NPS.

- Why withdrawal should be evaluated against long-term retirement security.

How Abhipra Can Help

Families planning NPS Vatsalya transition, NPS contribution setup or regular NPS continuation can connect with Abhipra's NPS Desk for process guidance. Use the relevant action link below based on the support required.

- Explore Abhipra NPS services for Vatsalya and regular NPS support

- Open an NPS account through Abhipra's registered PoP journey

- Set up an NPS SIP through Abhipra's PoP journey

- For NPS queries, write to nps@abhipra.com

Source Links

- PFRDA: NPS Vatsalya

- PFRDA: Official website

- NPS Trust: Official website

Disclaimer

This article is for educational and informational purposes only. It should not be treated as investment, tax, legal or retirement planning advice. NPS and NPS Vatsalya are subject to applicable PFRDA rules, investment risks, tax provisions, withdrawal conditions and operational processes. Investors and guardians should evaluate goals, risk appetite, investment horizon, liquidity needs and tax situation before making any decision.