Emergency Fund: The First Step Before Investing

Before a new investor thinks about stocks, mutual funds or long-term wealth creation, one question should come first: if income stops or a medical, job or family emergency appears, will the household be forced to sell investments at the wrong time?

An emergency fund is the cash buffer that protects your investment journey from avoidable disruption. It is not meant to chase returns. Its job is to keep essential expenses funded when life becomes unpredictable.

Start With Stability Before Market Risk

The SEBI Investor Charter says investors should understand risks before investing and read documents carefully. That advice becomes more practical when your basic cash cushion is already in place. Without a reserve, even a good long-term investment can become a forced sale during a short-term problem.

Think of the emergency fund as the first layer of your financial plan. It should sit before SIPs, direct equity, F&O, insurance reviews and long-term portfolio allocation. Once the household has breathing room, market-linked investments can be handled with more patience and less panic.

What Should This Money Be Ready To Pay For?

Start by listing essential commitments, not lifestyle spending. A useful emergency-fund worksheet should include:

- house rent or home-loan EMI;

- groceries, utilities, school fees and basic transport;

- insurance premiums that must not lapse;

- medicines, medical deductibles and family-care needs;

- existing loan EMIs and minimum unavoidable obligations.

The right buffer is not identical for every investor. A salaried person with stable income, low debt and two earning members may need a different reserve from a self-employed professional, single-income family or business owner with uneven cash flows.

Where Should The Emergency Fund Sit?

The first priority is access and safety, not maximum return. Many households keep the core reserve in bank savings accounts, sweep facilities or short-term deposits, depending on liquidity needs and bank terms.

For bank deposits, investors should understand the protection framework. DICGC states that eligible deposits such as savings, fixed, current and recurring deposits are insured up to Rs 5 lakh per depositor per bank, covering principal and interest within that limit. This is useful information, but it is not a reason to ignore diversification, bank selection or account documentation.

Market-linked products can have a role in a broader plan, but emergency money should not depend on a volatile asset price being favourable on the exact day cash is needed.

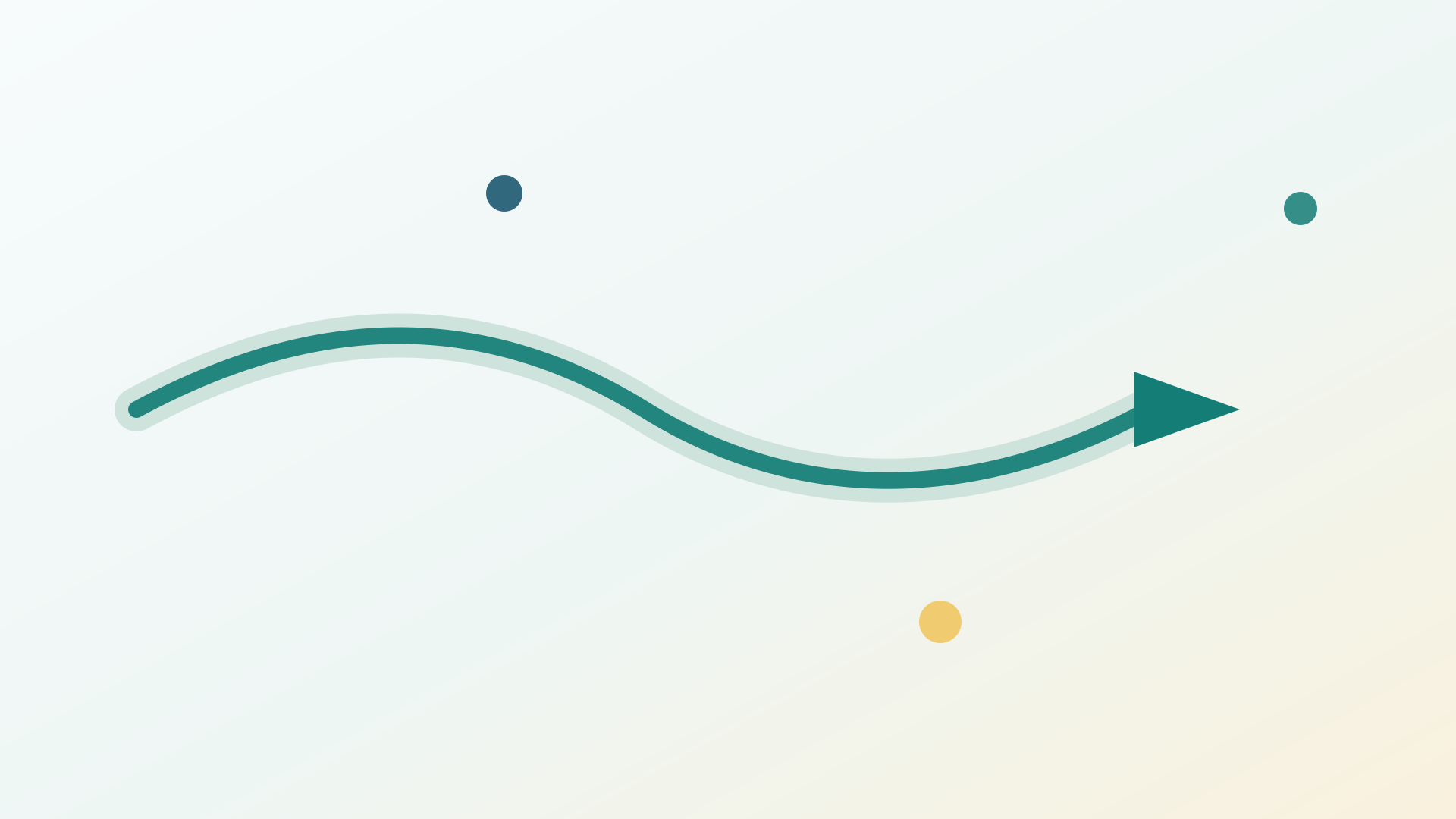

From Cash Buffer To Investing Habit

The visual follows one simple story: essential expenses come first, a protected reserve comes next, and investment growth begins only after the household has short-term resilience. This order helps investors separate emergency liquidity from long-term wealth creation instead of using one account for every purpose.

Common Mistakes

- Investing every surplus rupee while keeping no cash buffer.

- Treating credit cards or personal loans as the emergency plan.

- Keeping emergency money in risky or locked-in products.

- Forgetting annual insurance premiums, school fees or tax payments while estimating essential expenses.

- Using the emergency fund for planned lifestyle purchases and then not refilling it.

Investor Checklist

- Write down unavoidable monthly commitments.

- Separate emergency money from spending money.

- Keep access simple for genuine emergencies.

- Review bank coverage, nominee details and account access for family members.

- Start investing gradually only after the emergency buffer plan is clear.

- Rebuild the fund after every withdrawal.

When you are ready to begin investing after setting up your reserve, you can explore Abhipra online account opening at ekyc.abhipra.com or learn about Abhipra Depository Services.

Reviewed by Abhipra Research / Compliance Team.

Source Links

- SEBI Investor Charter

- DICGC: A Guide to Deposit Insurance

- NSE India: Getting Started for First-Time Investors

Disclaimer

This article is for educational and informational purposes only. It should not be considered investment advice, trading advice, tax advice or insurance advice. Investments in securities market are subject to market risks. Please read all related documents carefully before investing. Past performance is not indicative of future returns. Please consult a qualified financial advisor, tax advisor or insurance advisor before making any financial decision.