Why Share-Capital Records Become Harder to Manage as a Company Grows

Reviewed on: 2 July 2026. Reviewed by Abhipra RTA / Compliance Team.

A small company can often track shareholders through a familiar register and a few certificate files. As the company grows, that approach becomes fragile. More shareholders, more security classes, dematerialisation requirements, transfers, allotments, pledges and corporate actions all have to match across statutory, RTA and depository records.

The risk is not only clerical. A weak share-capital record can delay ISIN activation, dematerialisation, PAS-6 reconciliation, funding rounds, rights issues, buybacks, due diligence and investor servicing.

The Record Stops Being One Register

In the early stage, management may think of shareholding as a single register. Over time, the record becomes a connected control system.

Typical record layers include:

- statutory register of members and security holders;

- share certificate issue and cancellation records;

- board and shareholder approvals for allotments, transfers and corporate actions;

- instrument-wise and class-wise capital records;

- RTA master records and transaction logs;

- depository records after ISIN activation and dematerialisation;

- beneficial-owner reports and demat credit files;

- PAS-6 or share-capital reconciliation working papers where applicable; and

- evidence retained for auditors, investors, lenders or professionals.

If these layers do not agree, the company may not know whether the issue is a missing board approval, an unrecorded transfer, a certificate mismatch, a depository credit issue or a data migration error.

Growth Events That Add Complexity

| Growth event | What becomes harder | Control expected from management |

|---|---|---|

| More shareholders | Names, addresses, joint-holding order, PAN/KYC status, contact details and transmission history become harder to keep current. | Maintain a clean investor master and preserve evidence for every change. |

| More security classes | Equity shares, preference shares, debentures, CCDs or CCPS may need class-wise records and, where dematerialised, separate ISIN planning. | Reconcile authorised, issued, subscribed and paid-up capital by class before operational changes. |

| Mandatory dematerialisation | The company must coordinate issuer admission, RTA records, depository records, shareholder demat accounts and corporate actions. | Treat demat as a project with owner, timeline, record freeze points and exception tracking. |

| New funding or corporate action | Rights, bonus, private placement, buyback, pledge, transfer or conversion records must match approvals, registers and depository files. | Run pre-action checks before board approval and post-action reconciliation after completion. |

| Professional due diligence | Investors, lenders, auditors and company secretaries ask for a traceable history, not only a latest cap table. | Preserve source documents, approval trails, correspondence, reconciliations and unresolved exception notes. |

Demat Rules Make Record Quality More Visible

Rule 9A introduced dematerialisation requirements for specified unlisted public companies. Rule 9B extended a dematerialisation framework to specified private companies, with important exclusions and timelines. The 30 June 2025 extension for many non-small private companies is now a past date, so companies should avoid treating it as an upcoming compliance window.

For affected companies, the issue is not simply obtaining an ISIN. Records must support:

- which securities are covered;

- whether the company falls within or outside the applicable rule scope;

- whether promoters, directors and key managerial personnel hold securities in demat where required before relevant actions;

- whether shareholders can transfer or subscribe in the manner required by the rules;

- whether class-wise capital records agree with depository records; and

- whether reconciliation evidence is ready for professional review.

Where the company status, exemption position, producer-company timeline or later change in small-company status is unclear, it should be marked for human legal review before operational instructions are issued.

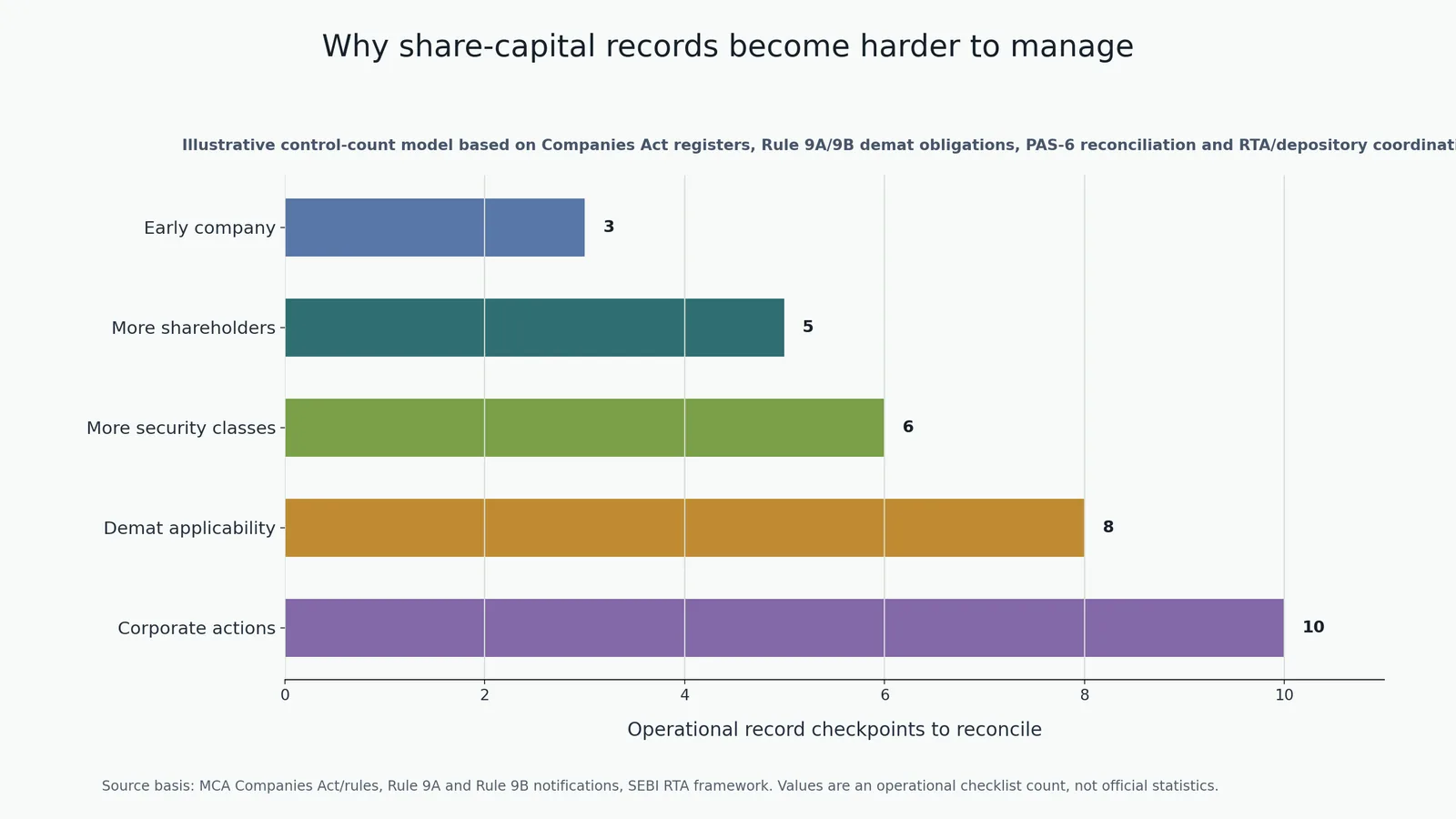

An Operational View of Complexity

The chart uses an operational checklist count, not official statistics. It shows why management attention rises as more record layers must be reconciled.

| Stage | Illustrative checkpoints | Examples included in the count |

|---|---|---|

| Early company | 3 | Register, certificate record and approval trail. |

| More shareholders | 5 | Investor master, KYC/contact changes, joint holding and transfer/transmission history. |

| More security classes | 6 | Class-wise capital, instrument terms, conversion/redemption events and ISIN planning. |

| Demat applicability | 8 | RTA master, depository admission, demat requests, beneficial-owner records and reconciliation. |

| Corporate actions | 10 | Pre-action eligibility, record date, credit files, post-action reconciliation and exception closure. |

Common Errors That Delay RTA Work

Frequent issues include:

- latest cap table not matching statutory registers;

- physical certificate details missing, duplicated or not cancelled after demat;

- old addresses, signatures or joint-holding order not aligned with demat account details;

- board approvals and allotment records not matching the capital summary;

- separate security classes treated as one operational pool;

- transfers recorded commercially but not supported by complete documents;

- foreign shareholder records missing PAN, beneficial ownership or certification checks;

- PAS-6 or reconciliation work started after the half-year close instead of during the period; and

- exceptions discussed informally but not recorded with owner, date and closure status.

The practical fix is a controlled record-cleanup sequence: freeze the latest capital snapshot, map every security class, identify missing documents, reconcile certificates and demat data, then close exceptions before new transactions are processed.

Management Checklist Before the Company Grows Further

Before a funding round, rights issue, ESOP exercise, buyback, merger, foreign investment transaction or ISIN activation, the board and company secretary should confirm:

- The latest capital summary agrees with the statutory register.

- Every security class is separately identified.

- Share certificates issued, cancelled, split, consolidated or lost are traceable.

- Transfers, transmissions and allotments have approval and evidence trails.

- Promoter, director and KMP holdings are reviewed where demat rules affect future actions.

- Shareholder names and holding order can match demat account records.

- RTA, depository and company-secretarial teams are using the same cut-off data.

- PAS-6 or reconciliation obligations are planned before the reporting period closes.

- Open exceptions have an owner, target date and review status.

- Sensitive investor documents are collected only through secure channels.

How Abhipra Can Assist

Abhipra can support companies, professionals and management teams with preliminary share-capital record review, RTA coordination, dematerialisation readiness, ISIN activation support, investor master cleanup, corporate-action data preparation and secure exception tracking.

For a preliminary RTA or dematerialisation discussion, review Abhipra RTA Services or connect through Abhipra Contact. Do not send passwords, OTPs, unmasked PAN, bank details, signatures or sensitive KYC documents by email; wait for a secure submission route.

Source Links

- MCA Companies Act and rules e-book area

- MCA Companies (Prospectus and Allotment of Securities) Third Amendment Rules, 2018

- e-Gazette G.S.R. 802(E), dated 27 October 2023

- SEBI Registrars to an Issue and Share Transfer Agents Regulations, 2025

- SEBI Master Circular for RTAs, dated 6 February 2026

- SEBI special window for transfer and dematerialisation of physical securities, dated 30 January 2026

- NSDL official website

- CDSL official website

Disclaimer

This article is for educational and informational purposes only. It is not legal advice, securities-law advice, tax advice, FEMA advice or a compliance certification. Applicability of MCA, SEBI, depository and FEMA requirements depends on the company's facts, security type, shareholder category and current law. Please consult qualified professionals before taking corporate, legal, secretarial, tax, FEMA or investment action.