Physical Share Certificates vs Dematerialised Securities: A Corporate Compliance Comparison

Reviewed on: 3 July 2026. Reviewed by Abhipra RTA / Compliance Team.

Physical certificates and dematerialised securities both represent ownership, but they create very different compliance work for a company. Physical records depend heavily on certificate custody, folio matching and paper evidence. Demat records shift the workflow toward RTA, depository, DP and beneficial-owner coordination.

For companies preparing for growth, funding, dematerialisation, PAS-6 reconciliation or corporate actions, the difference is not cosmetic. It changes how records are verified, how transfers are controlled and how exceptions are closed.

What Changes When Securities Move From Paper to Demat

Physical share certificates are paper evidence issued against a folio. The company and its RTA must keep the register, certificate record, transfer history, loss or duplicate certificate evidence and shareholder identity trail aligned.

Dematerialised securities are held electronically through the depository system. The investor holds through a demat account with a Depository Participant, while the issuer and RTA coordinate with the depository for admitted securities, corporate actions, reconciliation and investor-service data.

| Area | Physical certificate workflow | Demat workflow |

|---|---|---|

| Ownership record | Company register, folio and certificate history are central. | Beneficial-owner records and depository data become central alongside issuer/RTA records. |

| Transfer control | Paper instruments, certificate custody and signature evidence matter heavily. | Transfer and credit flow through demat account and depository mechanisms, subject to applicable law and restrictions. |

| Loss and duplicate risk | Lost, damaged or duplicate certificates can create reissue and evidence issues. | Paper-certificate loss risk reduces after successful dematerialisation, but account and identity controls still matter. |

| Corporate actions | Dispatch, endorsement, certificate updates and folio records can add manual work. | Corporate action files, record date data and demat credit reconciliation become the control focus. |

| Audit trail | The trail depends on registers, certificates, transfer deeds, correspondence and board records. | The trail includes issuer records, RTA records, depository reports, demat request evidence and exception logs. |

Applicability Depends on Company and Security Type

Rule 9A created a dematerialisation framework for specified unlisted public companies. Rule 9B later extended a framework to specified private companies, with exemptions, exclusions and timelines that must be checked against the company's facts. The 30 June 2025 extension for many non-small private companies is now a past date.

For listed-company physical securities, SEBI's investor-service and physical-security circular framework may apply differently from unlisted-company shareholding. The SEBI special window dated 30 January 2026 is an important current source for eligible listed-company physical-security cases, but it should not be mechanically applied to every private or unlisted company situation.

Where the issuer type, security class, small-company status, producer-company timeline, listed status or exemption position is unclear, mark the matter as REQUIRES HUMAN LEGAL REVIEW before giving operational instructions.

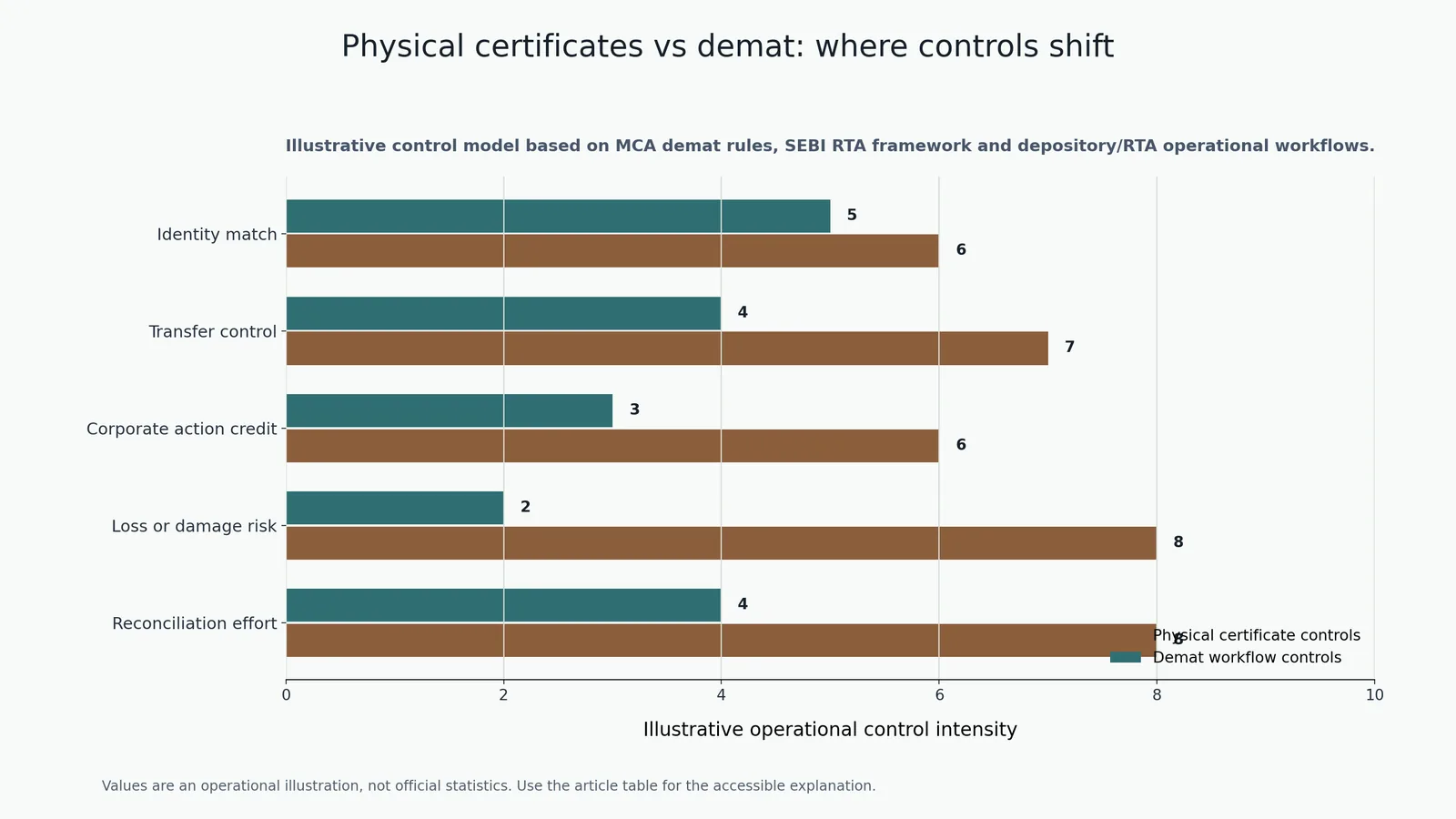

Where Controls Shift

The chart is an operational illustration, not official statistics. It shows that demat reduces some paper-custody risks, while increasing the need for clean digital identity, depository coordination and reconciliation discipline.

| Control area | Physical certificate intensity | Demat workflow intensity | Meaning for management |

|---|---|---|---|

| Identity match | 6 | 5 | Name, holding order and KYC still need careful matching. |

| Transfer control | 7 | 4 | Paper transfer evidence reduces, but restrictions and approvals still need control. |

| Corporate action credit | 6 | 3 | Demat credit can streamline processing if master data and record date files are clean. |

| Loss or damage risk | 8 | 2 | Physical custody risk reduces after successful demat. |

| Reconciliation effort | 8 | 4 | Demat helps only when company, RTA and depository records are reconciled regularly. |

Common Errors During Physical-to-Demat Transition

Common problems include:

- physical certificates not matching the latest register;

- joint holder order not matching the demat account;

- name, address or signature differences not resolved before the demat request;

- certificate loss or duplicate issue records not documented cleanly;

- transfers or transmissions attempted without checking the correct legal route;

- separate security classes treated as one pool;

- corporate action planning started before ISIN and master data are clean; and

- listed-company physical-security processes confused with unlisted-company demat requirements.

The practical sequence is to clean the company register, classify securities, identify the applicable rule or process, resolve certificate and shareholder mismatches, coordinate with the RTA and depository, then close exceptions before relying on demat records for a transaction.

Management Checklist

Before deciding whether paper records are ready for dematerialisation or a corporate action, confirm:

- the company type and applicable demat rule;

- listed or unlisted status;

- security class and ISIN requirement;

- latest register, certificate and transfer history;

- shareholder name, PAN/KYC, address and holding order;

- lost, duplicate, split or consolidated certificate history;

- board approvals and transaction restrictions;

- RTA, DP and depository dependencies;

- reconciliation owner and target date; and

- secure document-submission channel.

How Abhipra Can Assist

Abhipra can support companies, professionals and shareholders with physical-to-demat readiness review, RTA coordination, ISIN activation support, investor master cleanup, demat request tracking, corporate-action data preparation and exception closure.

For preliminary support, review Abhipra RTA Services or connect through Abhipra Contact. Do not send passwords, OTPs, unmasked PAN, bank details, signatures or sensitive KYC documents by email; wait for a secure submission route.

Source Links

- MCA Companies Act and rules e-book area

- MCA Companies (Prospectus and Allotment of Securities) Third Amendment Rules, 2018

- e-Gazette G.S.R. 802(E), dated 27 October 2023

- SEBI Registrars to an Issue and Share Transfer Agents Regulations, 2025

- SEBI Master Circular for RTAs, dated 6 February 2026

- SEBI special window for transfer and dematerialisation of physical securities, dated 30 January 2026

- NSDL official website

- CDSL official website

Disclaimer

This article is for educational and informational purposes only. It is not legal advice, securities-law advice, tax advice, FEMA advice or a compliance certification. Applicability of MCA, SEBI, depository and FEMA requirements depends on the company's facts, security type, shareholder category, listed status and current law. Please consult qualified professionals before taking corporate, legal, secretarial, tax, FEMA or investment action.